Macroprudential Policy in a Monetary Union SUERF conference „Monetary and economic policies on both sides of the Atlantic“

Check against delivery.

Corresponding author: Claudia M. Buch, Deutsche Bundesbank, Postfach 10 06 02, 60006 Frankfurt, Germany. This text is based on joint work with Manuel Buchholz and Katharina Knoll, both Deutsche Bundesbank. An earlier version of this text has been prepared for the conference “High Public Debt: Theoretical and Historical Perspectives” held at Goethe University Frankfurt on May 17, 2019. We are grateful to Puriya Abbassi, Fabian Bichlmeier, Magnus Brechtken, Robert Düll, Albrecht Ritschl, and Edgar Vogel for most helpful inputs as well as to Janina Berner for excellent editorial assistance. The paper reflects the views of the authors and not necessarily those of the Deutsche Bundesbank. All errors and inconsistencies are our own.

1 Motivation

Central banks rely on and play a key role in ensuring the stability of the financial system. Yet, the definition of “financial stability” as an explicit policy objective and the assignment of a role for central banks has been a relatively recent development. Financial stability is defined as a situation in which the financial system neither contributes to a pronounced amplification of an economic downturn nor is a source of instability itself.

The specific tasks assigned to central banks have been evolving over time. According to the Bundesbank Law of 1957, the Bundesbank’s mandate was rather broadly defined as to “safeguarding the currency”.[1] Forty years later, in the wake of the evolving European economic and monetary union, the Bundesbank’s mandate became focused on “maintaining price stability”. After the financial crisis, the Financial Stability Act of 2013 prominently provided for the Bundesbank to contribute to safeguarding financial stability.

While central banks play an important role in ensuring financial stability through macroprudential policies, they do not act independently. The Bundesbank and the Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht, Bafin) are members of the Financial Stability Committee (Ausschuss für Finanzstabilität), the main policy body responsible for macroprudential surveillance. The committee is chaired by the Ministry of Finance.[2] The Committee evaluates the stability of the German financial system, submits an annual report to the German Bundestag, and it can issue warnings and recommendations. The Bundesbank provides analytical inputs for the discussions.

Macroprudential policy is particularly important in a monetary union where joint responsibility for monetary policy coincides with national responsibility for key policy areas affecting financial stability. Hence, mechanisms are needed which prevent the build-up of excessive levels of private or public debt.

Recognizing the importance of sound fiscal positions for a monetary union, the Stability and Growth Pact focuses on mechanisms to contain the build-up of excessive levels of public debt at the level of individual member states. The European sovereign debt crisis has been a painful reminder of how important incentives to maintain sound public finances are. But it has also shown that looking at the current levels of public debt might be insufficient. In the wake of banking crises, and without credible mechanisms to restructure excessive private debt, governments might be forced to intervene. Private debt may then turn into public debt.

Financial stability has thus been established as a new policy field in order to address the build-up of excessive levels of private debt. Macroprudential policy aims at increasing the resilience of the financial system, making systemic financial crisis that may, ultimately, result from excessive surges in debt less likely and severe. In addition, credible resolution regimes for banks are needed to reduce implicit government guarantees and to prevent risks from being shifted from the private to the public sector in times of crisis.

Against this background, this paper makes three key points:

First, monitoring the build-up of unsustainable debt levels requires taking the real economy into account. Weaker economic growth impairs the ability to repay debt, and negative shocks can lead to a self-enforcing downward spiral as has happened during the European debt crisis (German Council of Economic Experts 2011; Shambaugh 2012). Sound financial systems contribute to economic growth, and financial instabilities have negative implications for the real economy (Levine 1997, Pagano 1993, Rajan and Zingales 1998). Debt per se is not the issue, but debt levels which are excessive relative to the underlying strength of the real economy. Understanding the channels through which the build-up of financial stability risks affect the real economy and may cause resource misallocation is important. Expectations are key in this regard: Expectations that are overly optimistic with regard to future fundamentals and the evolution of the real economy can put the repayment of debt at risk.

Second, the dividing line between private and public debt is not always clear-cut. Through the conversion of implicit into explicit subsidies for the financial sector, unsustainable levels of private debt can spill over into governments’ balance sheets. A highly leveraged financial system may breed systemic risks and threaten the functioning of the financial system. If buffers against risks in the private sector are insufficient, the government might be forced to intervene in times of crisis. Implicit public guarantees for financial institutions can contribute to excessive risk taking and high leverage. Such implicit subsidies not only reflect that some institutions can become too large or too complex to fail. Instead, common exposure to aggregate or macroeconomic risks can lead to “collective moral hazard

” if too many institutions are exposed to the same type of shock (Farhi and Tirole 2012).

Third, macroprudential policy is the first line of defence against such spill overs of risk from the private to the public sector. Macroprudential policy aims at enhancing the resilience of the financial system with regard to adverse shocks and addressing the build-up of unsustainable financing choices. Macroprudential policy plays a particularly important role in the European monetary union which lacks a single sovereign and where many policies that can affect the stability of financial markets are under the domestic responsibility for policy (Buch and Weigert 2019).

2 Public and Private Debt in the Long-Run

a) Leveraging Up

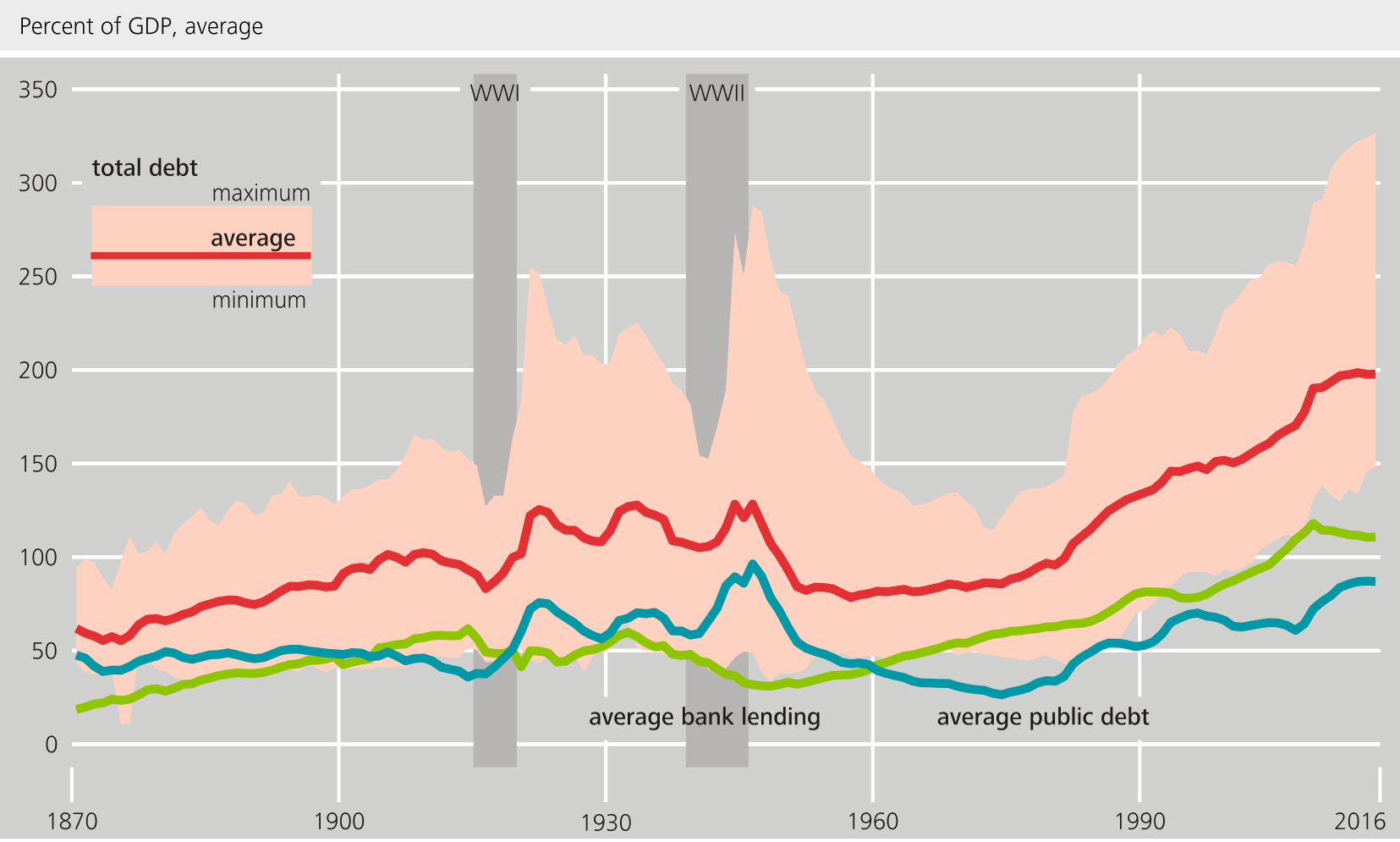

The 20th century has seen a substantial increase in overall debt levels. Figure 1 (Panel a) plots the aggregate private and public debt over time for 17 advanced economies since the late 19th century. Relative to GDP, total debt has more than doubled. Around the year 1900, the total debt of households, non-financial businesses, and governments amounted to a little less than 100% of GDP. In 2016, total debt was just about to cross the 200% mark. Advanced economies have levered up considerably during the past century, and a large share of the increase in total debt happened in the decades after 1970. Figure 1 (Panel b) also shows that there is considerable heterogeneity across advanced economies, reflecting different institutional structures, financial sector regulation, social security systems, and preferences.

Figure 1 (Panel a) shows that the public debt ratio has been broadly stable at around 50% between 1870 and World War I. But two world wars and the Great Depression created substantial demand for public spending and drove up public debt levels significantly in advanced economies. In the middle of the 20th century, public debt amounted to nearly 100 percent of national income on average. After a consolidation period of about three decades, the increase came to a halt around 1990. In the aftermath of the Global Financial Crisis, fiscal imbalances once more increased considerably. By the year 2016, the mean public debt-to-GDP ratio had nearly reached its mid-20th-century peak (Eichengreen, El-Ganainy, Esteves and Mitchener 2019; Jordà, Schularick and Taylor 2016b).

The trajectory of private debt to GDP looks somewhat different. Relative to national income, borrowing of households and non-financial businesses rose more than threefold prior to World War I. While public debt surged, bank lending declined during the World Wars and the Depression-era of the 1930s. Around 1950, private credit amounted to less than a third of annual GDP on average. By the early 1970s, it had doubled and reached its pre-World War I level. Since then, the private debt ratio has nearly doubled again, arriving at more than 110% of annual GDP in 2016 (Jordà, Schularick and Taylor 2016b; Schularick and Taylor 2012). The spectacular rise in total debt relative to GDP since the 1970s depicted in Figure 1 (Panel a) has thus mainly been the result of an unprecedented growth of private sector debt.

Which factors can account for the leveraging up of public and private balance sheets? The determinants of trends and fluctuations in public debt ratios are rather well-documented. Historically, spikes in public borrowing often followed armed conflicts, recessions, and financial crises. On a more general level, the role of the state for the macro-economy has changed. Particularly in the second half of the 20th century popular demands on governments, for health care, or pensions became an important driver of public debt ratios across the Western world (Eichengreen, El-Ganainy, Esteves and Mitchener 2019).

This increase in private leverage has been driven by several factors. First, financial development and financial integration have proceeded rapidly over the past century. Financial innovations have allowed financial institutions to better manage risks, to increase their tolerance to risk, and to take on higher leverage. In the post-war period, banking markets were largely protected by capital controls and restrictions on the activities of domestic financial institutions. Banking crises were rare (Kaminsky and Reinhart 1999), and banking was considered to be “boring” (Krugman 2009). Yet, deregulation of banking markets started in the 1980s, both in the US and Europe, leading to a significant expansion of financial intermediation, including expansion of cross-border finance. Second, the widespread introduction of deposit insurance and of lender of last resort functions has, arguably, changed risk tolerance and the extent of moral hazard (Taylor 2014). Third, policies targeted at specific credit market segments have increased the demand for credit. For example, policies aimed at increasing homeownership may have contributed to an increase in mortgage credit given that the vast majority of households borrow to buy a house (Rajan 2011). This aspect is particularly important since mortgage debt is the main financial liability of the household sector, and mortgage loans are the main asset of the financial system (Jordà, Schularick and Taylor 2016a).

b) Financial Crises and Deleveraging

High leverage may be problematic as it increases the vulnerabilities of debtors (and thus creditors) to macroeconomic volatility and heightened uncertainty. This is the reason why, historically, financial crises have often been private credit booms gone bust. High levels of debt can signal a debt overhang. A debt overhang exists if the current debt burden is deemed “unacceptably” high by market participants and misaligned with fundamentals. The level that is perceived to be “acceptable” varies with economic conditions – it may be higher when times are good and lower in economic downturns. In fact, financial crises are often associated with a downward revision of acceptable debt levels resulting from a sudden awareness that assets have become overvalued and that collateral requirements have been too lax.

In response to adjustments of expectations, debtors will deleverage to clean up their balance sheets. And this deleveraging may lead to a self-enforcing debt deflationary spiral that reinforces the initial shock (Fisher 1933). Once debt is perceived as being excessive, credit markets tighten. Debtors are forced to liquidate assets in order to reduce the stock of debt. Asset prices fall and increase the value of debt in real terms, leading to a vicious cycle of distress selling and a debt-deflationary spiral. The existing evidence suggests that such deleveraging spells can be both severe and long-lasting (IMF 2016, Lang and Welz 2018, Mbaye, Badia and Chae 2018). Average deleveraging episode in advanced economies since the mid-20th century took roughly four years, and private debt was reduced by about 15-19% of GDP.[3] The shock triggering an adjustment of expectations may be a demand or a supply shock – i.e. households or firms may deleverage. Recent research based on historical evidence points to the importance of demand shocks (Benguria and Taylor 2019).

Deleveraging of households and deleveraging of firms may act as a drag on economic growth. High and persistent levels of household debt were a main factor holding back economic recovery after the Global Financial Crisis,[4] just as it played an important role in explaining the consumption collapse during the 1930s.[5] In both cases, a shock to household balance sheets resulted in a reduction in consumption with significant macroeconomic effects. As indebted households tend to have a relatively higher propensity to consume out of wealth compared to creditors, their effort to deleverage can translate into a decline in aggregate demand (Tobin 1980). Indeed, evidence suggests that an increase in the household debt-to-GDP ratio predicts lower GDP growth and higher unemployment in the medium run (Mian, Sufi, and Verner 2017).[6] Debt overhang in the non-financial firm sector can trigger similar adjustment patterns (Ceccheti, Mohanty, and Zampolli 2011). Facing the need to “repair” their balance sheet following an adverse shock, firms reduce investment with negative effects for economic growth.

In both cases, the financial sector may act as an amplifier. In light of a debt overhang of firms and households, banks’ may face a surge in nonperforming loans. In a benign scenario, this may cause a reduction in credit availability, additionally dragging on the macroeconomy. In the most extreme case, a surge in nonperforming loans may even threaten the solvency of banks. Banks foregoing profitable lending activities may aggravate the initial shock (Philippon and Schnabl 2013). Such feedback loops are more likely if many sectors of an economy are affected at the same time. For example, declining household demand will force firms to reduce wage costs or to lay off workers, which further depresses demand (Bornhorst and Ruiz-Arranz 2013).

3 Links between Private and Public Debt

a) Crisis-Related Support to Financial Institutions

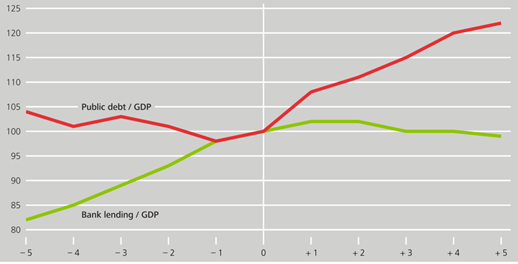

While households and firms lever up their balance sheets when times are good and when optimism is high, governments tend to reduce their debt burden relative to GDP. Private borrowing thus tends to be strongly procyclical. Public borrowing displays at least some countercyclical elements as it tends to grow faster in recessions than in expansions. These different cyclical trajectories tend to be most pronounced in the run-up to and the aftermath of financial crises (Jordà, Schularick and Taylor 2016b). Based on data for the group of advanced economies discussed above, Figure 2 confirms that private and public debt are likely to move in opposite directions around these episodes. Bank lending typically strongly increases in the years before a financial crisis. By contrast, governments tend to be able to reduce their debt burden relative to GDP. Once the crisis is in full swing, trajectories reverse. Public debt increases significantly, by about 20 percentage points within the 5-year window on average. Bank lending to the private sector stagnates or even declines during this period.

This pattern is not very surprising. After all, once vulnerabilities in private balance sheets are exposed, interventions of the public sector are often the only option in the short-term to prevent a further fall in output and deflationary pressure. Romer and Romer (2019, p. 39) review the narrative evidence of post-crisis fiscal expansions and conclude that there appears to be “[…] remarkable agreement across policymakers from different countries that financial rescue is valuable and appropriate in times of high financial distress

.” Clearly, the response to a financial crisis depends on the fiscal space governments had ex ante: The larger the fiscal space, the more aggressive governments’ response to financial crises, and the less severe the post-crisis output losses (Romer and Romer 2019; Jordà, Schularick, and Taylor 2016b).

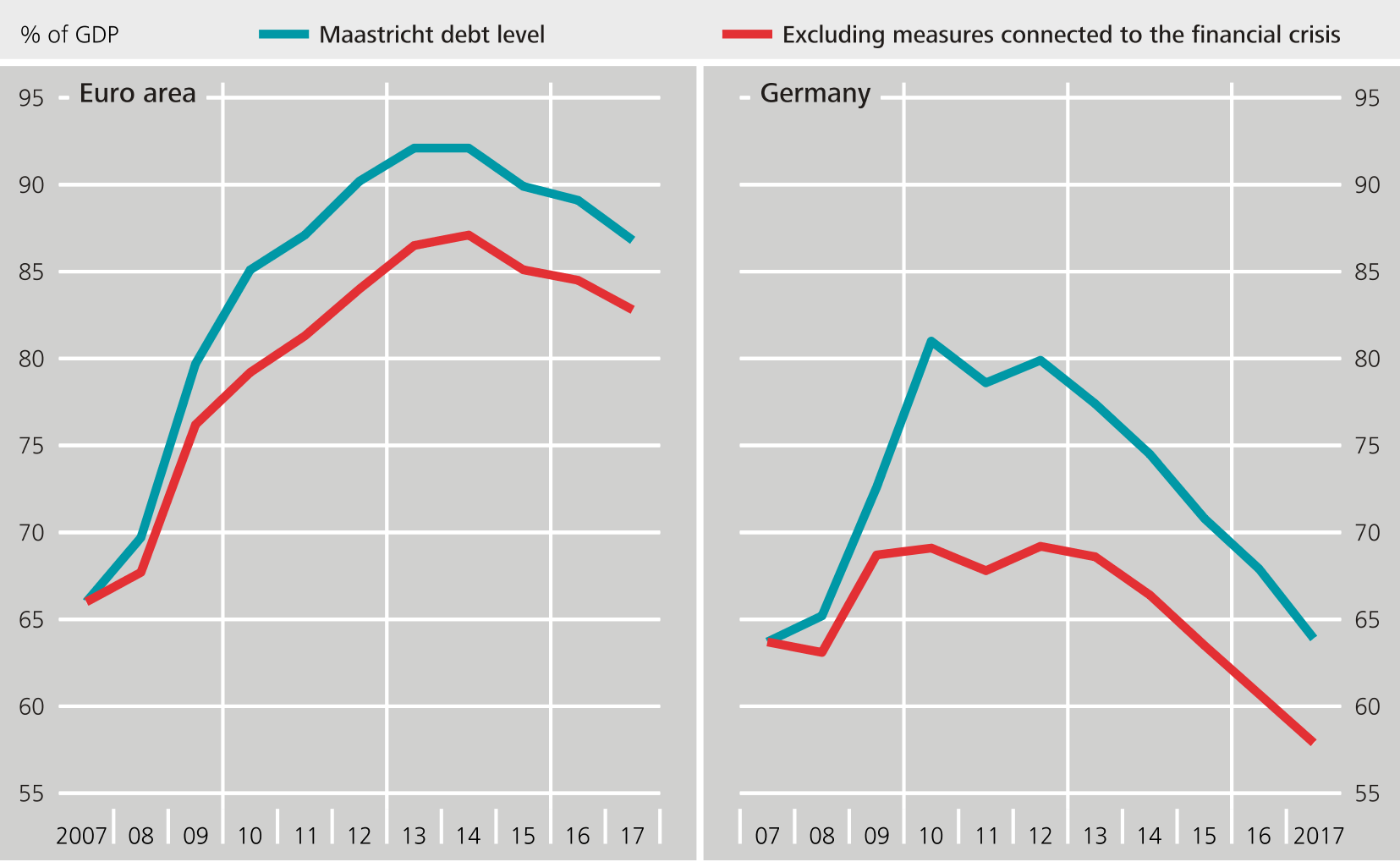

As an example, the right panel of Figure 3 sheds light on the effect on public finances measures based on the recent German experience. When the financial crisis hit, Germany had a comparably balanced budget. In 2008 and 2009, the government introduced measures aimed at stimulating economic growth in the form of three main stimulus packages.[7] Between 2007 and 2010, the German public debt ratio had increased by nearly 20 percentage points. As the European national debt crisis began to unfold, the German government took a U-turn and passed the so-called Future Package aimed at reducing public spending and increasing taxes.

Public support after crises often targets troubled debtors or creditors directly. The rationale is to help overcoming coordination problems, market failures, or the inability of distressed banks to absorb losses (Laeven and Laryea 2009; Laryea 2010). Providing relief for debtors, e.g. by providing subsidies to creditors for lengthening maturities, providing credit guarantees, creating asset management companies, or even engaging in direct lending to companies that are unable to access financial markets. Measures may also focus on creditors, e.g. in the form of financial sector rescues.

In the wake of the Global Financial Crisis, governments also supported banks within their jurisdictions through capital injections or explicit guarantees. The extent of this risk transfer from the private to the public sector is reflected in public debt ratios. Figure 3 compares the evolution of public debt levels with and without assistance of the public sector for financial institutions. In the counterfactual case without any crisis-related support to the financial sector, general government debt relative to GDP would have been more than 4 percentage points lower in 2017 in the euro area (left panel). In Germany, this gap amounted to nearly 12 percentage points in 2010 (right panel). Almost ten years after the crisis, in 2017, the gap still stood at 6 percentage points.

Rescue measures such as capital injections or explicit government guarantees can have a pronounced and persistent effect on government finances. The long-term net effect depends on the specific form of intervention and the recovery of markets. If, for instance, governments have acquired equity stakes in banks and the market recovers, net cost of interventions decline over time and may even turn into net benefits. If, however, the public sector issues guarantees only and does not participate in the upsides of this investment, costs for the taxpayer might be substantial.[8]

b) The Bank-Sovereign Nexus

If risk is transferred from the private to the public sector through some form of bail out, this leaves its trace on balance sheets of governments. Indeed, sovereign spreads tend to increase after bailout announcements. As a result, governments themselves might come under financial pressure after a bailout. A self-reinforcing feedback loop harbouring risks to financial stability and macroeconomic growth may ensue: Doubts about government solvency induce a decline in sovereign bond prices and may lead to a deterioration in the credit quality of banks; bank distress may become more widespread and trigger additional government support measures, calling into question the sustainability of public finances even more (Deutsche Bundesbank 2015a). This bank- sovereign nexus, which has been exposed not least during the European sovereign debt crisis, has been extensively described in recent literature (Acharya, Drechsler and Schnabl 2014, Alter and Schüler 2012).

The mutual dependence of banks and government has a long history. Historically, governments often needed a financier to enable warfare and trade. During the 16th century, the role of banks became more important as Europe evolved from decentralized feudalism to a more centralized system of a few dominant nation-states (Calomiris and Haber 2014). But banks were not only important financiers, they also helped the sovereign placing its debt on the market.

One indication for the close financial relationship between banks and sovereign is that banks tend to overinvest into bonds issued by the home government compared to a well-diversified international bond portfolio (De Marco and Macchiavelli 2016, Horváth, Huizinga, and Ioannidou 2015). To what extent this pattern reflects a “home bias” in banks’ investment portfolios is hard to assess, given that investment patterns depend on preferences, incentives, regulations, and transaction costs.

The regulatory treatment of sovereign debt certainly affects portfolio choices of banks (Deutsche Bundesbank 2014, 2017; Kirschenmann, Korte and Steffen 2017). Under current bank capital regulations, exposures of banks to sovereign debtors in the country’s own currency are assigned a risk weight of zero. In addition, these claims are exempted from limits on large exposures that would otherwise apply to large exposures to non-sovereign entities. Similar exemptions apply to liquidity regulations. Yet, claims on governments are not immune to the risk of default or of illiquidity.

c) Implicit Subsidies and Systemic Risk

Implicit guarantees for liabilities of financial institutions are a key channel through which private and public debt are linked. They are contingent liabilities for the government which can turn into explicit payment obligations in times of crisis. Quantifying this implicit subsidy and thus the expected bailout that debt holders expect to receive is not an easy task. Funding costs advantages of banks which are deemed “too big to fail” (TBTF) may serve as a proxy (Siegert and Willison 2015). The size of the funding cost advantage for a bank depends on the expected probability of default, the loss given that a default has occurred, and the expected recapitalization through the government. The probability of being bailed out, in turn, is influenced by factors such as the resolution regime and the fiscal capacity necessary to make the implicit guarantee credible.

Financial institutions that are deemed “too-big-to-fail” are indeed a recurrent theme in the history of financial crises. Individual banks can become too big, too interconnected with the rest of the financial system, or too complex to disorderly exit the market. In 2011, G20 members thus agreed on reforms addressing the “systemic and moral hazard risks associated with systemically important financial institutions

” (FSB 2011). Three sets of policies have been implemented to achieve this objective: (i) improved loss absorbency and resilience, (ii) improved recovery and resolution, and (iii) improved supervision.

Assessing the effects of reforms requires a distinction between private as well as social costs and benefits. The internalization of systemic externalities and the withdrawal of implicit TBTF subsidies results, ceteris paribus, in an increase in funding costs. Like the introduction of a pollution emission tax, an increase in funding costs will be perceived as a cost of reforms by private market participants while, at the same time, contributing to lower “emissions” – hence lowering the costs of financial crises to the taxpayer.

The withdrawal of subsidies also has implications for the risk-taking of banks. The optimal level of risk taken by TBTF banks from a private perspective can be higher than the socially efficient level of risk: Owners of banks fully reap potential profits but only partially bear potential risks due to the expected government bailout in case of distress.

Excessive risk-taking implies costs for society: If risks materialize, taxpayers may face additional costs related to the need to rescue the bank. Regulatory reforms aimed at internalizing the external costs through, for example, higher loss absorbing capacity and provisions to facilitate the orderly resolution of TBTF banks thus have the potential to increase social welfare. But these reforms may come at a net private cost for the affected banks as they will incur costs to comply with the new regulation and are likely to face higher funding costs.

In an ongoing evaluation conducted in 2019 and 2020, the Financial Stability Board assesses whether the implemented reforms are reducing the systemic and moral hazard risks associated with systemically important banks (SIBs). [9] The evaluation will also examine the broader effects of the reforms to address TBTF for SIBs on the overall functioning of the financial system.

This project focuses on a core objective of the G20 financial reforms: To address the systemic and moral hazard risks associated with systemically important financial institutions (SIFIs) (FSB 2011). Beyond resolution regimes, policy measures to address the “too-big-to-fail (TBTF)” problem include a more intense supervision of SIFIs and higher requirements for their loss absorbing capacity. The project will assess whether perceived implicit funding subsidies have changed; how much progress has been made regarding the resolvability of systemically important banks; whether this has affected bank behavior; and whether there have been broader effects of the reforms on the real economy.

The FSB published its work plan, invited feedback on it, and solicited supporting evidence of reform effects from respondents. This is in line with the FSB’s aim to be open and transparent and engage in a dialogue with a broad range of stakeholders. To put the evaluation on a firm methodological foundation, the project is conducted with input from academic advisors. There are further opportunities for interaction with the FSB evaluation teams: External stakeholders will engage with the team in workshops and roundtables, and a consultation report will be published in June 2020.

The Role of Macroprudential Policy in a Monetary Union

Credit booms and a potentially resulting debt overhang are crucial determinants of the likelihood of financial crises, their severity, and the strength of the recovery that follows. This is why monitoring debt levels and macroprudential policy are particularly important in a monetary union with a joint responsibility for monetary policy but national responsibilities for key policy areas potentially affecting financial stability.

Most central banks relate the stability of the financial system to its ability to cushion shocks so as to mitigate the costs of financial distress for the real economy. The Bundesbank’s definition is in line with this notion. It follows the idea that the financial system should constantly be able to fulfil its key macroeconomic functions: Financing investment, providing savings opportunities, allocating risks, and maintaining the payments system. A stable and resilient financial system fulfils these functions and does neither amplify nor trigger an economic downturn. It should consistently be in a position to absorb losses from both financial and real economic shocks.

Consider a negative shock to the economy and to the net worth of firms. This may trigger a negative spiral, causing credit defaults, and a reduction in banks’ capital. Capital ratios will decline, potentially leading to the breach of regulatory capital requirements. At the same time, market participants will revise expectations and require higher levels of capital over and above the regulatory minimum. How can banks react? In theory, they could accumulate additional equity capital internally through retained earnings or by raising fresh capital on markets. In practice, however, this route will be blocked in a crisis. Hence, banks can restore required levels of capital only by divesting assets and deleveraging. This adjustment, in turn, has effects on other market participants: Direct contagion through contractual linkages or indirect contagion through fire sales of assets affect market prices and thus all other institutions that are exposed to the same types of risk. The result can be a credit crunch, which amplifies the initial shock and has negative repercussions on the real economy. Bank capital is thus the most important determinant of a banks’ loss absorption capacity. Sufficient equity buffers of banks can be a “circuit breaker”.

Microprudential supervision is thus the backbone of a stable financial system. But safeguarding financial stability requires a complementary, macroprudential perspective. The financial system is highly interconnected, shocks to large financial institutions may affect the stability of the system, and common exposures to macroeconomic risks matter. All of this creates systemic risk externalities. Even if all financial institutions properly manage their risks and behave prudently, amplification and contagion effects may threaten the stability of the system as a whole. This is why one should not fall victim to the “fallacy of composition”: The resilience of individual institutions is a necessary, but not a sufficient condition to ensure the resilience of the financial system.

It was the Global Financial Crisis that prompted the re-think in terms of legal mandates, in terms of regulation and policymaking. Macroprudential policy was introduced as a new policy area. In Europe, it is a shared responsibility between the national and the European level. Almost every member state has a national Financial Stability Council, which is responsible for the implementation of macroprudential policy domestically. While institutional arrangements differ across countries, central banks often play an explicit role in macroprudential policy and surveillance of risks to financial stability.

Financial stability begins at home and is a national mandate. Yet, it calls for close collaboration within Europe, given the close integration of markets and the potential of spillovers. This is why, at the European level, the European Systemic Risk Board (ESRB) has been monitoring financial stability in the EU since early 2011. The ESRB can issue warnings and recommendations addressed to the EU as a whole or to Member States, the European Commission, the European supervisory authorities or national authorities. Moreover, building on the financial market reforms agreed upon at the international level by the G20, the European institutional structure has been adjusted to make crises less likely and less costly. The European Stability Mechanism (ESM) and a resolution regime for distressed banks are key components of the post-crisis institutional architecture.

In 2014, the institutional setup of the European supervision changed fundamentally with the establishment of the Banking Union: Banking supervision of euro area banks was assigned to the Single Supervisory Mechanism (SSM) within the ECB which directly supervises systemically important banks of all member states. The Single Resolution Board was established as the central resolution authority. Together with the national resolution authorities, it forms the Single Resolution Mechanism (SRM).

With the formation of the Banking Union, the ECB has assumed macroprudential responsibilities in the banking sector alongside national authorities. The ECB has the power to top-up national macroprudential measures but not relax them. It thus has the possibility of counteracting a possible inaction bias at the national level.

Compared to other regions of the world, Europe is thus fairly advanced regarding cross-border policy coordination of macroprudential policy (BIS, FSB, IMF 2016). Coordinating policies is particularly important in Europe because of the high degree of financial integration and cross-border activity of banks within the Single Market and the Euro Area. At the same time, financial markets retain a strong national flavour, reflecting different traditions, preferences, and responsibility of national policymakers for policies affecting financial institutions and markets. Not least, the institutional set-up in Europe recognizes that macroprudential policy is an important complement to monetary policy: In a state of “financial dominance”, the central bank might come under pressure to provide liquidity in order to support the banking sector (Brunnermeier and Sannikov 2014). In this sense, macroprudential policies do not only contribute to a stable financial system but also ensure that monetary policy can focus on its price stability mandate (Deutsche Bundesbank 2015b).

5 Summing Up

Over the past two decades, the macroeconomic and institutional environment in which European central banks operate has changed significantly. Monetary policy has been a joint responsibility of central banks in the Eurosystem for 20 years now. Over the past 10 years, central banks have assumed additional responsibilities with regard to macroprudential policies; responsibilities for microprudential supervision and resolution have been moved to the European level. At the same time, many core policy areas, which may have an impact on financial stability, remain under national responsibility. This includes fiscal policy but also other financial market policies which affect balance sheet risks and risk-taking incentives. In this environment, effective macroprudential supervision is particularly important to prevent the build-up of financial instabilities.

This paper has made three key points.

First, instabilities on private financial markets and public debt can be closely interrelated. Hence, a comprehensive framework to monitor financial stability risks needs to take both into account. Risks to financial stability can arise not only if debt levels are too high compared to fundamentals from an ex ante perspective, but also if risks going forward are underestimated. Inaccurate beliefs about (future) fundamentals can lead to risks for financial stability (Gennaioli and Shleifer 2018). For example, in a protracted spell of low interest rates, coupled with favourable financing conditions and an ongoing economic boom, there is a tendency to ignore downside risk scenarios (Deutsche Bundesbank 2018). Market participants may underestimate future credit risk and being overly optimistic concerning their loss-absorbing capacity. Many market participants may then no longer take sufficient account of periods of crises and economic downturn in their risk assessment.

Second, implicit subsidies of the public sector for private debt are a channel through which distress can spill over from the private to the public sector. These implicit subsidies are, by definition, not directly observable. Different types of systemic risk externalities can give rise to such implicit subsidies – financial institutions can be too-big-to-fail, too-connected-to-fail, but also too-many to-fail.

Third, macroprudential policy is the first line of defence against excessive debt. History shows that private and public debt are closely interwoven. If any of the two becomes excessive and threatens financial stability, monetary policy can come under pressure, too. By reducing the probability and the effects of financial crisis, effective (macro)prudential policy protects the balance sheets of governments and – ultimately – central banks.

6 References

Acharya, V., I. Drechsler, and P. Schnabl (2014). A pyrrhic victory? Bank bailouts and sovereign credit risk. The Journal of Finance 69(6), 2689-2739.

Alter, A. and Y. S. Schüler (2012). Credit spread interdependencies of European states and banks during the financial crisis. Journal of Banking & Finance 36(12), 3444–3468.

Bank for International Settlements (BIS), Financial Stability Board (FSB), International Monetary Fund (IMF) (2016). Report on macroprudential policy frameworks, August. Basel and Washington DC.

Benguria, F., and A. M. Taylor (2019). After the Panic: Are Financial Crises Demand or Supply Shocks? National Bureau of Economic Research. NBER Working Paper 25790. Cambridge MA.

Bornhorst, F. and M. Ruiz-Arranz (2013). Indebtedness and Deleveraging in the Euro Area, 2013 Article IV Consultation on Euro Area Policies: Selected Issues Paper, Chapter 3, IMF Country Report 13/206. Washington DC.

Brandt, W., C. Buch, M. Hellwig, H.-H. Lotter, H. Merkt and D. Zimmer (2011). Strategien für den Ausstieg des Bundes aus krisenbedingten Beteiligungen an Banken. Gutachten des von der Bundesregierung eingesetzten Expertenrates. Berlin.

Brunnermeier, M. K. and Y. Sannikov (2014). Monetary Analysis: Price and Financial Stability, in: ECB Forum on Central Banking: Monetary Policy in a Changing Financial Landscape, Conference Proceedings. Frankfurt a.M.

Buch, C. M. and B. Weigert (2019). Macroprudential policy in a currency union. Review of World Economics 155(1), 23-33.

Bundesgesetzblatt (1957). Gesetz über die Deutsche Bundesbank, vom 26. Juli 1957. Teil I, Nr. 33, 745-755.

Bundesgesetzblatt (1997). Sechstes Gesetz zur Änderung des Gesetzes über die Deutsche Bundesbank, vom 22. Dezember 1997. Teil I, Nr. 88, 3274-3275

Bundesgesetzblatt (2013). Gesetz zur Stärkung der deutschen Finanzaufsicht, vom 28. November 2012. Teil I, Nr. 56, 2369-71

Calomiris, C. W. and S. H. Haber (2014). Fragile by Design: the Political Origins of Banking Crises & Scarce Credit, Princeton University Press, Princeton, New Jersey.

Cecchetti, S. G., M. Mohanty and F. Zampolli (2011). The Real Effects of Debt, Economic Symposium Conference Proceedings, Jackson Hole, 145-196.

De Marco, F. and M. Macchiavelli (2016). The Political Origin of Home Bias: The Case of Europe, Finance and Economics Discussion Series No 2016-060, Board of Governors of the Federal Reserve System. Washington DC.

Deutsche Bundesbank (2014). The Sovereign-bank Nexus, Financial Stability Review, November, pp. 89-99. Frankfurt a.M.

Deutsche Bundesbank (2015a), Annual Report 2014, March. Frankfurt a.M.

Deutsche Bundesbank (2015b). The Importance of Macroprudential Policy for Monetary Policy, Monthly Report, March, pp. 39-71. Frankfurt a.M.

Deutsche Bundesbank (2017). Financial Stability Review, November. Frankfurt a.M.

Deutsche Bundesbank (2018). Financial Stability Review, November. Frankfurt a.M.

Eggertsson, G. and P. Krugman (2012). Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo Approach, Quarterly Journal of Economics, 127, 1469–1513.

Eichengreen, B., A. El-Ganainy, R. Esteves, and K. J. Mitchener (2019). Public debt through the ages, CEPR Discussion Paper 13471. London.

Farhi, E. and J. Tirole (2012). Collective moral hazard, maturity mismatch, and systemic bailouts. American Economic Review 102(1), 60-93.

Financial Stability Board (FSB) (2011). Policy Measures to Address Systemically Important Financial Institutions. Basel.

Financial Stability Board (FSB) (2019). Evaluation of too-big-to-fail reforms: Summary Terms of Reference. Basel.

Fisher, I. (1933). The Debt-Deflation Theory of the Great Depression, Econometrica 1, 337–357.

German Council of Economic Experts (2011). Annual Report 2011/2012. Wiesbaden.

Gennaioli, N. and A. Shleifer (2018). A Crisis of Beliefs – Investor Psychology and Financial Fragility. Oxford University Press. Oxford.

Guerrieri, V. and G. Lorenzoni (2011). Credit Crises, Precautionary Savings, and the Liquidity Trap, Quarterly Journal of Economics 132(3), 1427-1467.

Horváth, B., H. Huizinga, and V. Ioannidou (2015). Determinants and Valuation Effects of the Home Bias in European Banks' Sovereign Debt Portfolios', CEPR Discussion Paper No 10661.

International Monetary Fund (IMF) (2016). Debt – Use it wisely. Fiscal Monitor October 2016. Washington DC.

International Monetary Fund (IMF), Financial Stability Board (FSB), Bank for International Settlements (BIS) (2016). Elements of Effective Macroprudential Policies: Lessons from International Experience. Basel and Washington.

Jones, C., T. Philippon, and V. Midrigan (2011). Household Leverage and the Recession. NBER Working Paper 16965. Cambridge MA.

Jordà, O., M. Schularick, and A. Taylor (2016a). The great mortgaging: housing finance, crises and business cycles. Economic Policy 31, 107-152.

Jordà, O., M. Schularick, and A. Taylor (2016b). Sovereigns vs. banks: Credit, crises, and consequences. Journal of the European Economic Association 14(1), 45-79.

Kaminsky, G. L. and C. M. Reinhart (1999). The twin crises: the causes of banking and balance-of-payments problems. American Economic Review, 89(3), 473-500.

Kirschenmann, K., J. Korte, and S. Steffen. (2017). The Zero Risk Fallacy? Banks’ Sovereign Exposure and Sovereign Risk Spillovers. ZEW Discussion Paper No 17-069. Mannheim.

Krugman, P. (2009). Making banking boring. New York Times, April.

Laeven, L., and T. Laryea. (2009). Principles of Household Debt Restructuring, IMF Staff Position Note 09/15. Washington DC.

Lang, J. H. and P. Welz (2018). Semi-structural credit gap estimation, ECB Working Paper No 2194. Frankfurt a.M.

Laryea, T. (2010). Approaches to Corporate Debt Restructuring in the Wake of Financial Crises. IMF Staff Position Note 10/02. Washington DC.

Levine R. (1997). Financial Development and Economic Growth: Views and Agenda. Journal of Economic Literature, 35(2), 688–726.

Mbaye, S., M. Badia and K. Chae (2018).Bailing Out the People? When Private Debt Becomes Public. IMF Working Paper No. 18/141. Washington DC.

Mian, A. R., K. Rao, and A. Sufi (2013). Household Balance Sheets, Consumption, and the Economic Slump. Quarterly Journal of Economics 128, 1687–1726.

Mian A. and A. Sufi (2014). What Explains the 2007-2009 Drop in Employment? Econometrica 82, 2197–2223.

Mian, A., A. Sufi and E. Verner (2017). Household Debt and Business Cycles Worldwide. Quarterly Journal of Economics 132 (4), 1755-1817.

Mishkin, F. (1978). The Household Balance Sheet and the Great Depression, Journal of Economic History 38, 918–937.

Olney, M. L. (1999). Avoiding Default: The Role of Credit in the Consumption Collapse of 1930, Quarterly Journal of Economics, 114, 319–335.

Pagano M. (1993). Financial markets and growth: An overview. European Economic Review, 37(2–3), 613–622.

Philippon, T. and P. Schnabl (2013). Efficient Recapitalization. Journal of Finance 68: 1–42.

Rajan, R. G. (2011). Fault Lines: How Hidden Fractures Still Threaten the World Economy, Princeton University Press, Princeton, New Jersey.

Rajan, R. G. and L. Zingales. (1998). Financial Dependence and Growth. The American Economic Review, 88(3), 559-586.

Romer, C. D. (1993). The Nation in Depression. Journal of Economic Perspectives, 7, 19–39.

Romer, C. D., and D. H. Romer (2019). Fiscal Space and the Aftermath of Financial Crises: How it Matters and Why. National Bureau of Economic Research. NBER Working Paper 25768. Cambridge MA.

Schularick, M. and A. M. Taylor (2012). Credit Booms Gone Bust: Monetary Policy, Leverage Cycles, and Financial Crises, 1870-2008, American Economic Review 102(2), 1029-61.

Shambaugh, J. C. (2012). The Euro’s Three Crises. Brookings Papers on Economic Activity, 43(1), 157-231.

Siegert, C. and M. Willison (2015): Estimating the Exctent of the ‘too big to fail’ Problem – A Review of Existing Approaches. Bank of England Financial Stability Paper No. 32. London.

Taylor, A.M. (2014). The great leveraging. In: The Social Value of the Financial Sector: Too Big to Fail or Just Too Big? edited by V. V. Acharya, T. Beck, D. D. Evanoff, G. G. Kaufman, and R. Portes. World Scientific Studies in International Economics, vol. 29. World Scientific Publishing, Hackensack, New Jersey.

Tobin, J. (1980). Asset Accumulation and Economic Activity: Reflection on Contemporary Macroeconomic Theory. University of Chicago Press, Chicago, Illinois.

7 Figures and Tables

Figure 1: Long-Run Trends in Private and Public Debt

Panel A of this Figure plots the aggregate private and public debt ratio over time for 17 advanced economies since the late 19th century (in red). Maximum and minimum levels of that ratio at any po

int in time are shown in shading The panel also shows the average private (ratio of bank lending to GDP, in green) and the average public debt ratio (in blue) separately, again based on data for 17 advanced economies. Panel B of this figure displays the private and public debt ratio country-by-country.

a) Aggregate Data

b) Country-by-Country

Figure 2: Public and Private Debt Before and After Financial Crises

The figure shows the evolution of public debt and the volume of bank lending relative to GDP (in %) 5 years before and after a systemic crisis. The data is the average for 17 advanced economies. Year 0 corresponds to a systemic financial crisis.

Figure 3: Effect of Financial Sector Assistance on Public Debt

The graphs show the level of public debt relative to GDP (in %) in the euro area and Germany (Maastricht debt level) – including and excluding measures connected to the financial crises. Measures connected to the financial crisis relate to government activities undertaken to directly support financial institutions. It does not include support measures for non-financial institutions or general economic support measures. The effect of financial sector assistance on debt is based on the „supplementary tables for reporting government interventions to support financial institutions” published under the excessive deficit procedure of the European Commission.

- For the legal background see Bundesgesetzblatt (1957, 1997, 2013).

- For an overview of different arrangements with regard to macroprudential supervision and the assignment of this mandate to central banks, see International Monetary Fund, Financial Stability Board, Bank for International Settlements (2016).

- See Mbaye, Badia and Chae (2018a) who analyze data on private and public debt dynamics in 150 countries since the 1950s.

- See Eggertsson and Krugman (2012), Guerrieri and Lorenzoni (2011), Jones, Philippon and Midrigan (2011), Mian and Sufi (2014) or Mian, Rao and Sufi (2013),

- See Mishkin (1978), Olney (1999), or Romer (1993).

- These results are based on a sample 30 countries for the years 1960-2012.

- These measures are the Economic Stability Plans 1 and 2 (Konjunkturpaket 1 and 2), enacted in 2008 and 2009 respectively, and the Growth Acceleration Law (Wachstumsbeschleunigungsgesetz), enacted in 2009. None of these packages became effective before 2009.

- See Brandt, Buch, Hellwig, Lotter, Merkt and Zimmer (2011) for a discussion of the German case.

- For details on the TBTF evaluation of the FSB, see: https://www.fsb.org/2019/05/fsb-launches-evaluation-of-too-big-to-fail-reforms-and-invites-feedback-from-stakeholders/