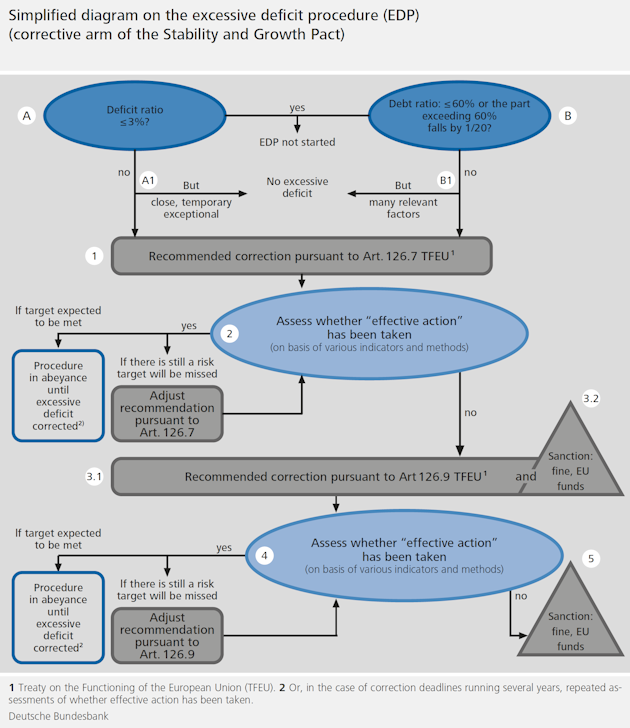

Bundesbank criticises developments in the European fiscal rules

The Bundesbank’s economists take a critical view of the fact that the European fiscal rules have been weakened rather than strengthened over the past few years. "The rules have become increasingly complex and considerable room for discretion has been opened up

," they note in the current Monthly Report. It is claimed that the European Commission, which is responsible for monitoring compliance with the rules, has, in agreement with the Council of the European Union, increasingly shifted the focus towards making the rules more flexible. "Now, It is virtually impossible to understand how they are being implemented. There is an impression that the interpretation of the rules is partly the outcome of a political negotiation process."

Fiscal rules are designed to safeguard monetary policy

The fiscal rules are a cornerstone of monetary union and their objective is to help promote sound public finances in the countries of the euro area. They are designed to prevent fiscal policy involving constant recourse to deficits and an expansionary stance. The rules are intended not least to prevent monetary policy from "succumbing to pressure to fund overindebted countries, thereby neglecting the objective of maintaining price stability and from redistributing risks through central bank balance sheets,

" the Monthly Report states.

Fiscal rules weakened more and more

Since the launch of the euro in 1999, there has often been a failure to comply with the cited regular quantitative targets and requirements stipulated in the SGP, say the economists. "Although the sovereign debt crisis and increased fiscal and monetary policy risk-sharing have highlighted the need for rules to have a stronger binding force, this has played only a minor role as time has gone on."

Ultimately, with regard to the debt criterion, there is little probability of a decision on the existence of an excessive deficit and, to date, there has been no instance of this happening,” say the Bundebank’s economists. All things considered, this gives the impression that “the rules are being adapted to the fiscal policy of the individual countries, rather than the other way round"

.

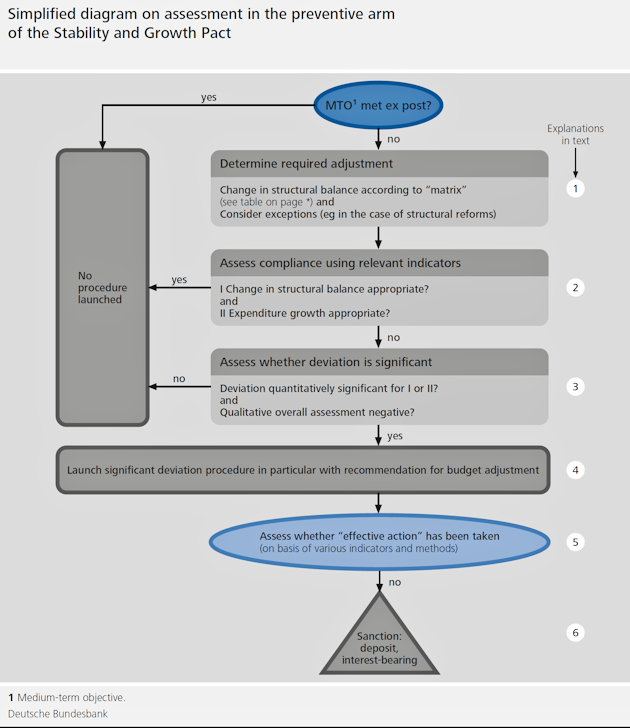

Making fiscal rules stronger again

For the future, it is important to make the monetary union more resistant to crises, it is stated in the Monthly Report. The burden arising from levels of sovereign debt that are still very high in some cases is currently being strongly mitigated by the low-interest-rate environment. With regard to a normalising of monetary policy, it is of fundamental importance that all countries rapidly achieve a sound basic position. "It is essential to tighten up fiscal rules again, not least in order to sustain confidence in public finances even given a less expansionary monetary policy stance in the future,"

is the call made by the economists. This includes a simple transparent design and implementation of the rules. Doing this will "require a marked restriction of exceptions, factors and adjustments to be considered

”.

In terms of a more targeted and less political approach, the Bundesbank believes it would be prudent to transfer the monitoring of compliance with the rules from the Commission to a new or another institution – say, the European Stability Mechanism. Moreover, under the no-bailout principle, the member states would be given incentives to pursue a sound fiscal policy in borrowing on the capital market. Credible fiscal rules could support borrowing on the markets without any notable risk premiums. By contrast, extending mutual liability, for instance, to compensate for a loss of confidence in the public finances of individual countries due to soft fiscal rules, would further weaken the balance between liability and control.