Understanding inflation

{kind=link}

How intensely a change in prices impacts on one's own purse depends on individual preferences and habits. Those who eat meat regularly are happy about a price reduction, while those who prefer fruit and vegetables are forced to dig deeper into their pockets. When prices increase not only of individual goods but persistently across the board, economists speak of inflation.

Stable prices benefit all

High inflation can have detrimental effects on businesses and consumers in the same way a prolonged decline in prices can. In the euro area, the Eurosystem – the European Central Bank (ECB) and the national central banks (NCBs) of the member states which use the euro as their single currency – have thus been tasked with safeguarding price stability.

For instance, as part of its monetary policy, the Eurosystem determines through the policy rate the cost at which commercial banks can borrow short-term money from central banks. In this way, the Eurosystem indirectly influences the interest rates at which banks grant credit to other banks or loans to businesses and consumers. These interest rates decide whether a business deems an investment to be worthwhile. Furthermore, they determine the share of income consumers choose to save rather than spend. Monetary policy thus impacts on aggregate demand and, by extension, on consumer price inflation.

Large basket of goods

In Germany, the Federal Statistical Office measures exactly how overall consumer prices are developing. To this aim, it continuously monitors a large basket of goods and services purchased by consumers in Germany. This includes many different kinds of food as well as petrol, package holidays and insurance premiums. The contents of the basket of goods are adjusted on an ongoing basis to reflect goods being purchased. Every month, the statisticians from the Federal Statistical Office capture more than 300,000 individual prices for the around 600 categories of goods. On the basis of this vast amount of data, the Federal Statistical Office each month calculates what is referred to as the consumer price index (CPI), which summarises all prices relevant to consumers in one single figure. For instance, if the CPI is currently 1.5% higher than it was twelve months earlier, this corresponds to an inflation rate of 1.5%.

With the help of regular extensive surveys, statisticians obtain information on the goods and services purchased on average by consumers in Germany. For this purpose, the various purchases are broken down into categories of varying sizes. A particularly large category of goods comprises housing rents, as it makes up around 20% of average expenditure. Bikes, on the other hand, amount to just under 0.2% of monthly expenditure, as consumers simply do not purchase them very often. Due to their low importance in overall monthly household expenditure, an increase in the price of bikes would hardly impact on the CPI and, thus, on the inflation rate.

Important benchmark

For the Eurosystem, the HICP in the euro area is the most important indicator of its objective of price stability, which the ECB Governing Council has defined as a year-on-year increase in consumer prices of below 2%. In the medium term, the ECB aims to achieve an inflation rate of below, but close to, 2%.

If the inflation rate falls below or exceeds this target in the short term, the Eurosystem is not necessarily called upon to adjust its monetary policy stance straightaway. For example, if harvests are unexpectedly bad due to a heat wave, this may temporarily push food prices up. However, with the next good harvest, prices ought to fall again. Monetary policy makers are unable to counteract such short-term price fluctuations fast enough with the instruments at hand because their measures take time to take effect. However, if it looks as though prices are rising or falling persistently, this could be an important signal for central banks to react with monetary policy measures. Ultimately, medium-term price developments are what counts from a monetary policy perspective.

Strong fluctuations in oil price

The oil price has a large impact on how inflation develops in the short term. As soon as it decreases, the prices for fuel and heating oil usually fall, too. When oil becomes more expensive, this is rapidly reflected in higher fuel and energy costs, which account for as much as around 10% of average monthly consumption expenditure. The oil price therefore not only affects an important category of goods it also fluctuates relatively strongly. Due to its key importance for the economy as a whole, the oil price is rather sensitive to developments that may affect the supply or demand of oil. That is why the oil price exhibits more pronounced and more rapid fluctuations than other prices.

A look at core inflation

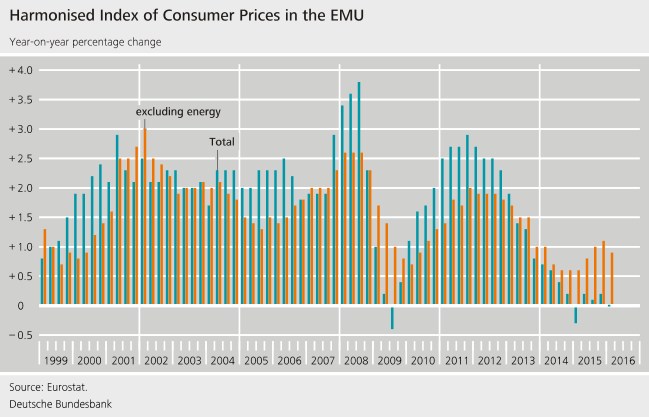

As a result, central banks across the world also look to specific indicators of consumer prices: core inflation rates. These rates indicate how consumer prices develop when selected items in the basket of goods are not included in the calculation. For the most part, such items are known to have strongly fluctuating prices, eg all goods which depend directly on the oil price. For example, when calculating the core inflation rate, statisticians do not then include prices for energy, especially heating oil, fuel, electricity and gas. The extent to which this changes average price developments is also reflected in the graph, which shows that headline inflation usually leans more in one direction than the core inflation rate excluding energy does.

The direction of price developments indicated by both inflation rates is often the same, whereas the intensity of the core inflation rate fluctuations often tends to be weaker. The core inflation rate therefore provides valuable additional information in determining the direction prices are headed in the medium term. At the same time, core inflation rates are not always the more reliable barometer for medium-term price pressures. For instance, the headline inflation rate reflects price developments more accurately than the core inflation rate if energy prices move in one direction over an extended period of time. Monetary policy guided solely by the core rate excluding energy would react too slowly and fail to meet its objective of price stability. Central bankers therefore never rely only on just one figure in their analysis, but rather strive for a picture that is as differentiated as possible based on numerous indicators.

Second round

However, central banks do not completely ignore oil price developments - quite the opposite, in fact. If petrol and heating costs rise following an oil price hike, consumers will adjust to this price change. Not only may their shopping behaviour change, they may also expect prices to increase further in the future. This could result in compensation demands in the next pay round to offset past or current increases in energy prices. If wages and salaries rise accordingly, the price inflation becomes entrenched as higher wage costs may prompt businesses to raise the prices of their goods. In this connection, economists speak of second-round effects, a consequence of which could be a spiral of rising wages and higher prices. It is, therefore, essential from a monetary policy perspective to identify second-round effects in time so as to implement countermeasures with the aim of ensuring a stable development of prices. Central banks will then be able to use their repertoire of instruments, including the policy rate, to somewhat curb economic activity so that consumers can expect a reduced rate of inflation.