Saving patterns in the low-interest-rate setting – results of the 2016 PHF summer survey Research Brief | 12th edition – April 2017

Households in Germany are expecting interest rates to stay low over the relatively long haul, with many intending to adjust their saving behaviour in response. These are two of the key findings from the 2016 Panel on Household Finances (PHF) summer survey.

The outbreak of the global financial crisis in 2008, induced a long-standing decline in interest rates on savings deposits, which are now entrenched at a low level. The persistent low-interest-rate setting was therefore the focal point of the Bundesbank's 2016 Panel on Household Finances (PHF) summer survey. Following an evaluation of the survey, we find that the protracted spell of low nominal interest rates has been increasingly impacting on households’ interest rate expectations: last year, 96.5% of households expected interest on savings to remain low for at least another year. This contrasts with only 65.4% in 2014. On the other hand, the share of households expecting interest rates to rise within the space of one year is down from 10% to 3.5%. In 2016, a majority of households (58%) was even expecting interest rates to stay entrenched at a low level for at least three more years. Are these distinct changes in interest rate expectations a sign that households have also adapted their saving behaviour?

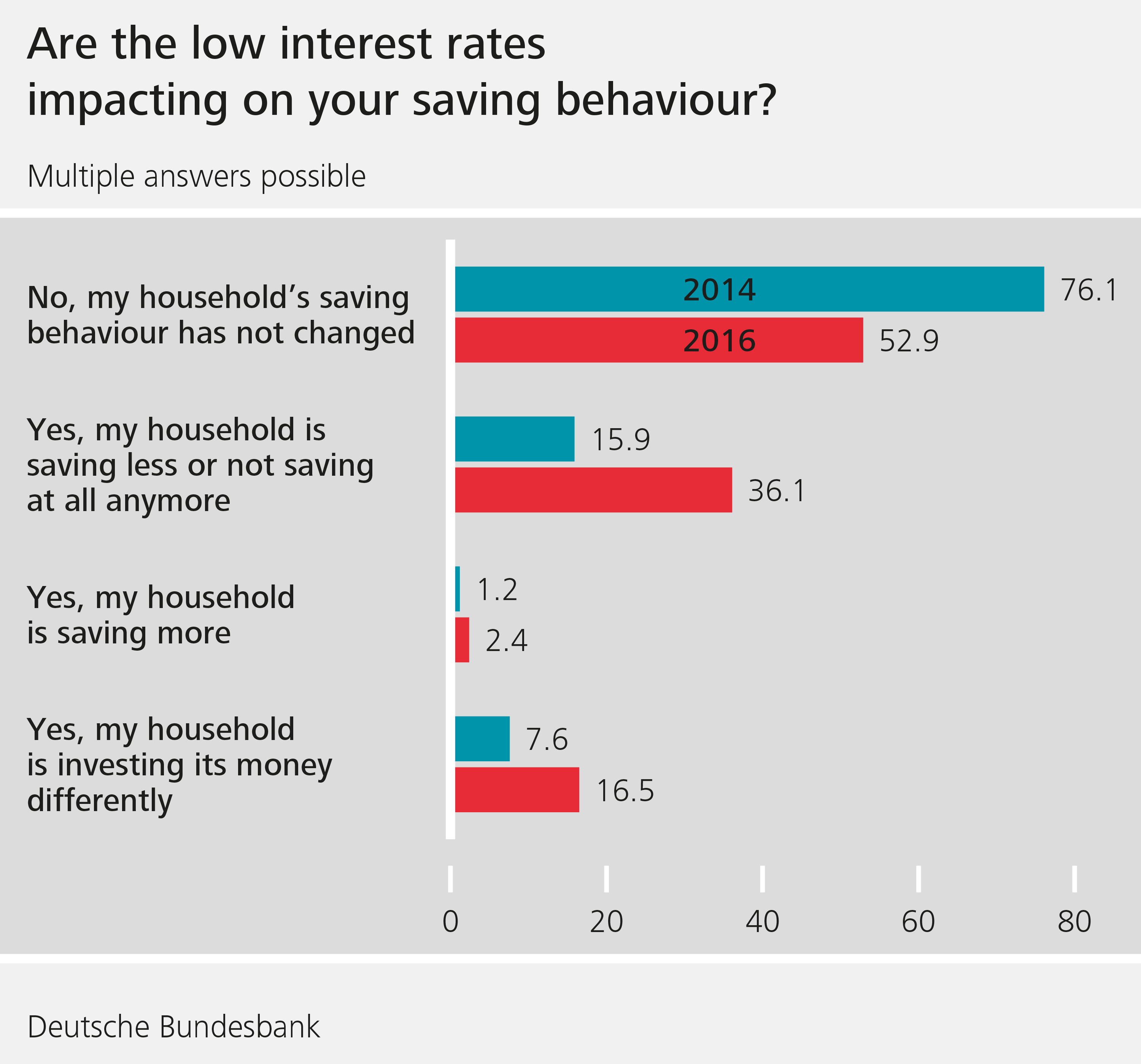

More than twice as many households adjusted their saving behaviour as in 2014

Nearly half of the households replied yes to the question of whether the low interest rates would impact on their saving behaviour. The share of households responding that they had adjusted their saving behaviour in response to the persistent phase of low interest rates was more than double its 2014 level (23%). Around 36% (15% in 2014) of households replied that they were saving less or not saving at all anymore on account of the low interest rates, whereas 16.5% of households (7.6% in 2014) reported that they were investing their money differently than before. Only 2% of those surveyed reported that they had increased their saving. What this indicates is that many households are not trying to make up for reduced interest income just by increasing their saving.

Interest expectations shaping saving

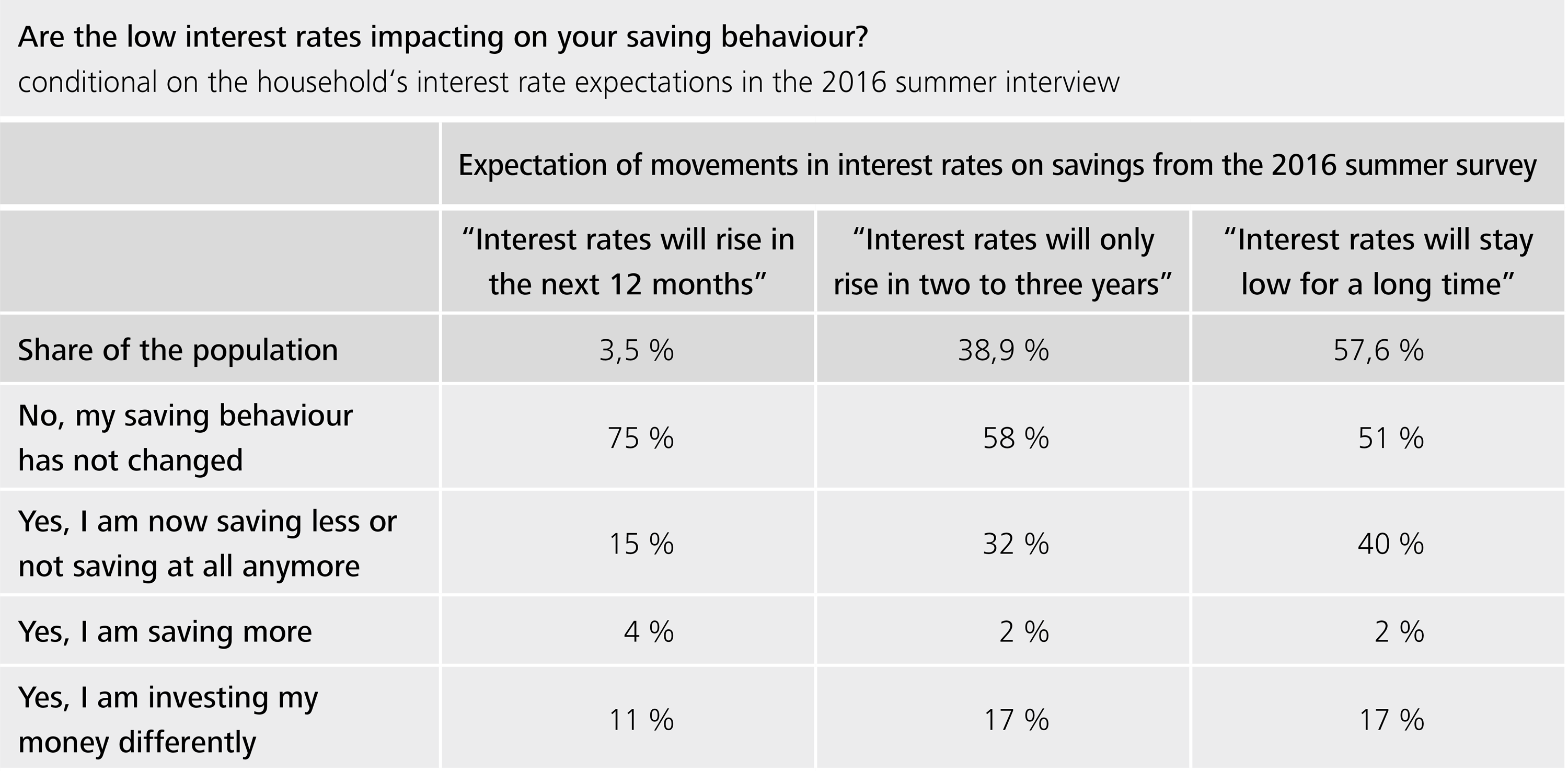

It appears as if current interest rates are not the only factor shaping households’ saving patterns. Households’ interest rate expectations are also a key factor for their savings behaviour. 40% of households expecting interest rates to stay low for more than three years planned on saving less or not saving at all anymore. By contrast, only 15% of the already-minuscule group of households (3.5%) expecting interest rates to go up planned on saving less or not saving at all anymore.

Households’ decision to change their saving patterns is likewise related to interest rate expectations. Around 17% of households expecting a protracted period of low interest rates reported that they invested differently than before. On the other hand, only 11% of households expecting interest rates on their savings to rise in the short term intend to change their saving behaviour.

Changes in saving behaviour also visible in aggregated figures

The financial accounts likewise show that households have recently changed their investment behaviour. Between 2014 and 2016, stocks of long-term savings deposits redeemable at notice of over three months, for instance, dropped by more than 30%, whereas the volume of short-term assets such as sight deposits (including cash) saw an increase of 22%. Households’ insurance claims and capital market investment likewise both showed inflows between June 2014 and June 2016. Claims on insurers were up by nearly 10%. Monetary assets invested in equities and mutual fund shares/units grew by 13% and 17%, respectively, with price movements accounting for around 5 percentage points of each respective increase.

Moreover, national accounts data show that, between 2014 and 2016, the household saving rate went up slightly, from 9.4% to 9.8%. At first glance, this appears to run counter to the findings from the Bundesbank survey. One reason for the discrepancy, then, could be that the survey did not cover the extent of saving, and that the aggregate household savings rate is shaped, in particular, by very wealthy households. The saving rate could therefore be on the rise even despite a decline in the percentage share of saving households. In addition, there is no firm proof that the surveyed households make a distinction between present and future saving behaviour. On top of that, there is also the possibility that the surveyed households do not regard the build-up of insurance provisions, capital market investment or repayments (especially for real estate) as an economic form of saving.

Conclusion

It follows from the 2016 PHF summer survey that households in Germany are expecting interest rates to remain low over the relatively long haul and, in comparison to the last survey wave in 2014, are increasingly seeking to adjust their saving behaviour. The survey data also show that saving behaviour is being shaped by households’ interest rate expectations. Of those households expecting interest rates to stay low, more than one-third reported that they were saving less or not saving at all anymore, whereas only a fraction of these households intend to save more.

| The PHF summer survey |

Since 2010, the Panel on Household Finances (PHF) has been surveying households resident in Germany on their assets and debt. The goal is to gain a better picture and understanding of households’ financial situation. For the PHF summer survey, roughly 5,000 households that had already taken part in the survey were asked to complete a short questionnaire in writing. A total of 2,816 households responded to the summer survey, representing 56% of households contacted. Most of the questions contained in the survey concern expectations and behaviour, in an attempt to capture, in particular, the impact of the protracted low-interest-rate setting on households’ decisions. |

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

| The author |

© Frank Rumpenhorst

Research economist |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein