The effects of the ECB’s new inflation target on private households’ inflation expectations Research Brief | 43rd edition – November 2021

Is there a difference between the inflation expectations of private households in Germany formed under the ECB’s previous target definition of “below, but close to, 2%” and those under the new inflation target of “symmetrically 2%”? New survey results from the Bundesbank Online Panel Households (BOP-HH) show that the new inflation target is associated with moderately higher inflation expectations for the next two to three years. The differences become more accentuated when the respondents are also told that the new monetary policy strategy entails the possibility of inflation exceeding the target.

In July 2021, the Governing Council of the European Central Bank (ECB) announced its new monetary policy strategy. Having previously pursued to keeping inflation “below, but close to, 2%” over the medium term, it now considers price stability to be best maintained by aiming for a 2% inflation target over the medium term. The new target is “symmetric”, meaning that deviations both above and below target are equally undesirable. To prevent negative deviations becoming entrenched, however, the ECB’s actions might result in the possibility of transitory periods in which inflation is moderately above 2%.

The ECB has also set its sights on making its communication with the general public as clear and intelligible as possible. To assess whether households take the ECB’s strategy into account when forming judgements on future price developments, we used the August 2021 Bundesbank Online Panel Households (BOP-HH) to ask around 3,000 households about their inflation expectations for the next two to three years, just after the changes in monetary policy were introduced.

Survey set-up

The household survey on the ECB’s current monetary policy takes the form of a randomized control trial. There are three steps to the experiment. To start with, all participants are told that the strategy until July had been to keep annual inflation “below, but close to, 2%” over the medium term and that, under the new strategy in place since July, the target is inflation of 2% over the medium term. The fact that this new target is symmetric, meaning that negative and positive deviations from it are considered to be equally undesirable, is also explicitly laid out in an easy-to-understand manner.

Second, all participants are asked to assume that the ECB, as hitherto, is aiming for an inflation rate of “below, but close to, 2%” over the medium term. The respondents then state what inflation rates they expect for the next two to three years. This period is based on the ECB’s projection horizon.

Third, the participants are randomly split into different groups and presented with different assumptions in terms of monetary policy and the inflation environment. A total of five sub-samples were formed in the August 2021 survey. The first group was instructed to assume that the ECB is aiming for an annual inflation rate of 2% over the medium term, in line with its new strategy. Corresponding with the information text, the respondents again received the information that this inflation target is symmetric, meaning that negative and positive deviations of inflation from the target are equally undesirable. The text for the second group is essentially the same as that for the first; however, they were also provided with an explicit version of the ECB’s official press release on the new inflation target that details the possibility of above-target inflation.

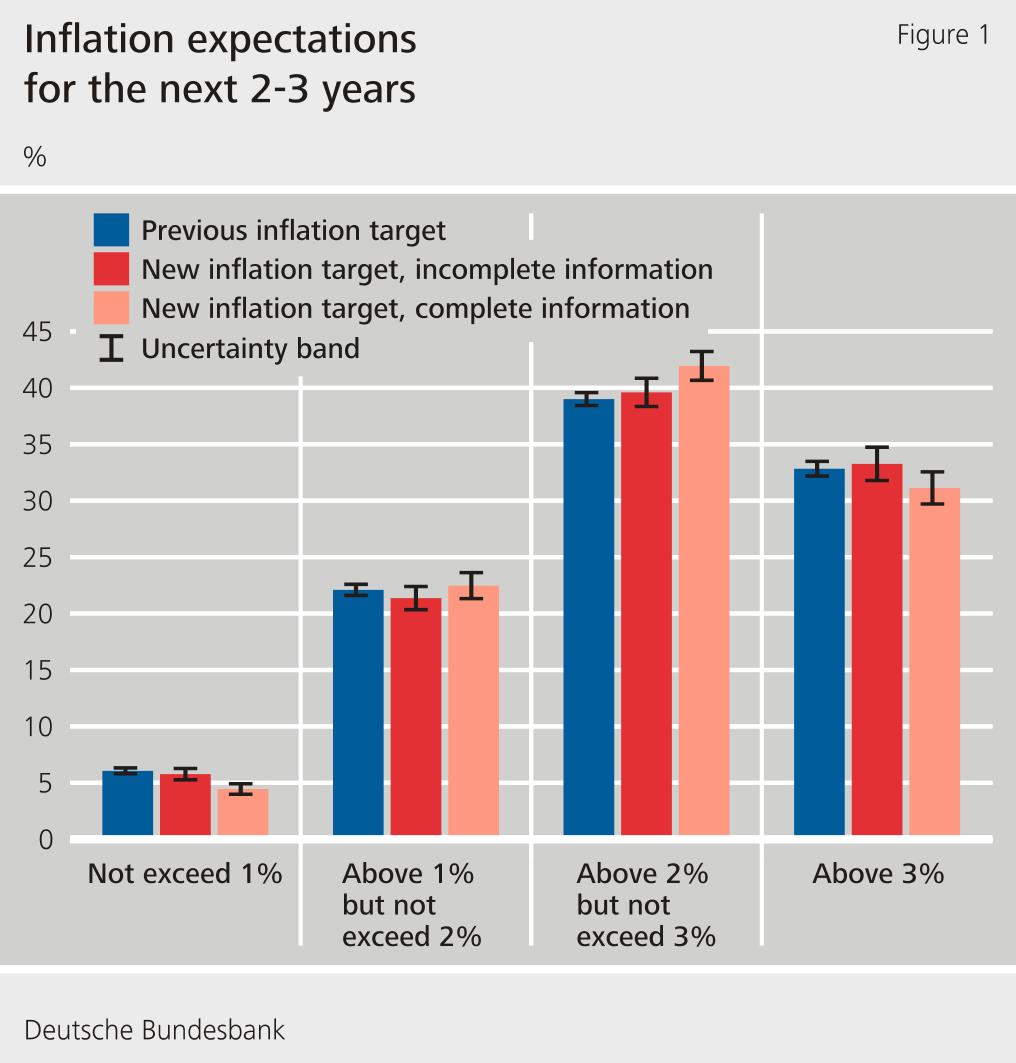

Comparing the previous and new monetary policy strategies

On the basis of these observations, we can infer that the respondents initially draw relatively little distinction between an inflation target of “below, but close to, 2%” and a “symmetrically 2%”. It appears, however, that the survey participants pay very careful attention to the information provided: the additional explanation that the inflation rate may exceed the 2% target under certain circumstances produced a statistically significant shift to the right in inflation expectations. Most notably, more respondents stated that they expect an inflation rate above 2% but no higher than 3% over the medium term. Meanwhile, under the ECB’s new strategy, inflation rates below 1% and above 3% were seen as significantly less likely than in the context of the previous strategy.

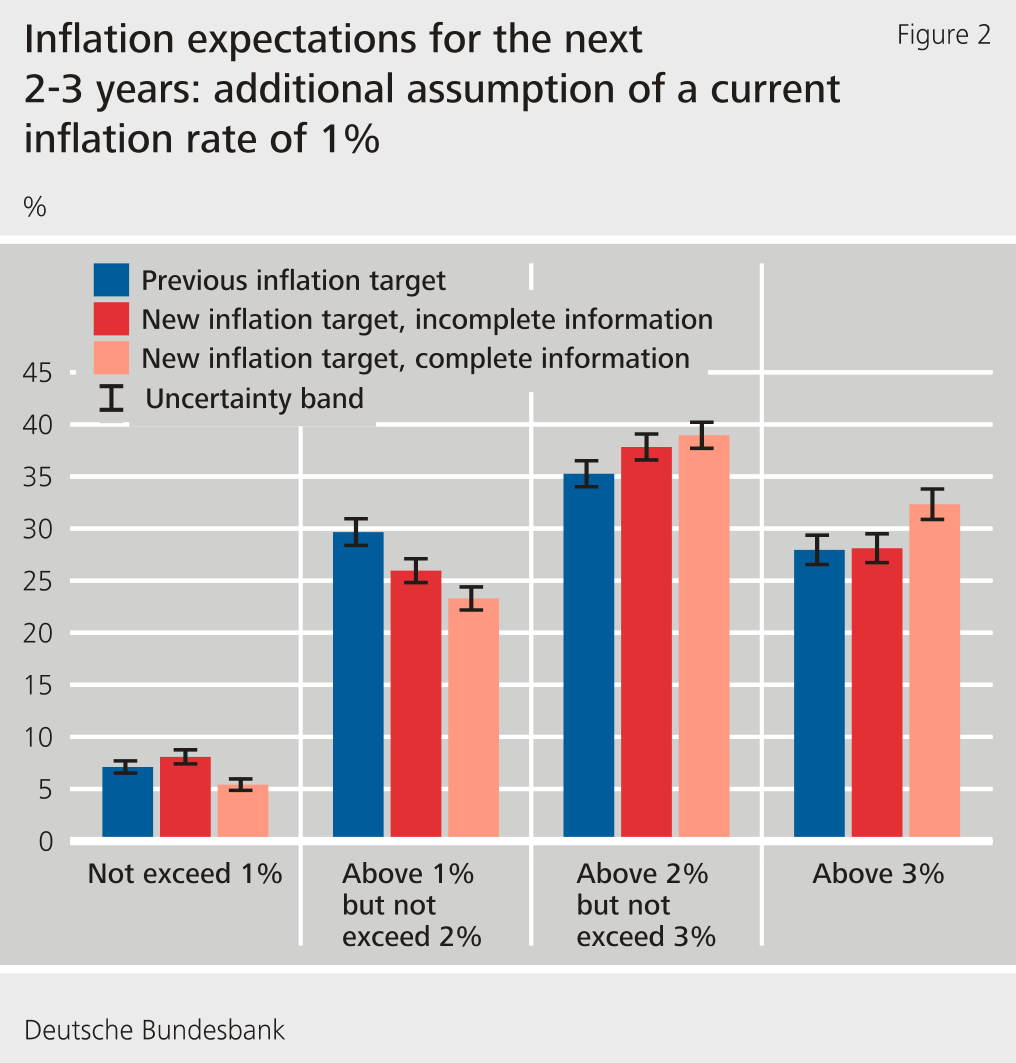

Additional assumptions about the inflation setting

Central banks can more easily reach their inflation target when they are able to steer inflation expectations through their communications. To test whether households would also understand a more complex central bank communication, we presented in the next step of the experiment three further groups of respondents with an additional assumption. In this case, the survey participants are asked to imagine they are in a low inflation environment, as has been the case in the euro area over the last ten years, and assume that the inflation rate will be only 1% for the next twelve months. This expanded assumption models a significant negative deviation from the inflation target, which, according to the ECB’s new monetary policy strategy, is to be avoided to become entrenched.

Having established this premise, one of the groups is then asked to assume that the previous ECB monetary policy of “below, but close to, 2%” remains in force. Two further groups are asked to assume that the new “symmetrically 2%” inflation target applies. As before, one of these groups of respondents is then shown the incomplete version of the ECB press release which does not mention the possibility of temporarily overshooting the inflation target, while the other group of respondents receives the complete version. Both groups of participants are asked to assume that the inflation rate will be just 1% over the next twelve months. These additional assumptions should allow a comparison of the extent to which the previous and new monetary strategies are able to affect inflation expectations. In order to effectively combat lasting negative deviations from the inflation target, the ECB’s new strategy entails the possibility of transitory periods in which the inflation rate could moderately top 2%. Provided households have trust that the ECB is committed to its new strategy, it is possible that they will adjust their inflation expectations to be above the target value. Where the previous strategy of “below, but close to, 2%” is assumed, there should be somewhat less strong adjustment of expectations, as the strategy does not tolerate potentially overshooting the inflation target following a hypothetical below-target rate of inflation of 1%.

In a more detailed regression analysis, which is not shown here, the statistically significant differences between the groups of respondents were confirmed to also apply to the average individual mean inflation value.

Conclusion

In August 2021, immediately after the introduction of the ECB’s monetary policy innovations, around 3,000 households in Germany were asked about their inflation expectations for the following two to three years via the Bundesbank Online Panel Households. Our analysis of these inflation expectations shows that households can distinguish between the ECB’s new symmetrical inflation target of an annual inflation rate of 2% over the medium term and the previous monetary policy target of an annual inflation rate of “below, but close to,2%” over the medium term. This result was particularly noticeable when respondents were explicitly informed about the possibility of temporarily exceeding the inflation target, which is entailed in the new ECB strategy. Furthermore, it shows that households understand the manner in which the new strategy is intended to function. After a period of very low inflation rates which fall short of the target value, the majority of respondents expects them to reach levels above the inflation target in the future. The results illustrate that clear monetary policy communication is suited for guiding the expectation formation process of private households.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein