Bundesbank further increases provisions for risk

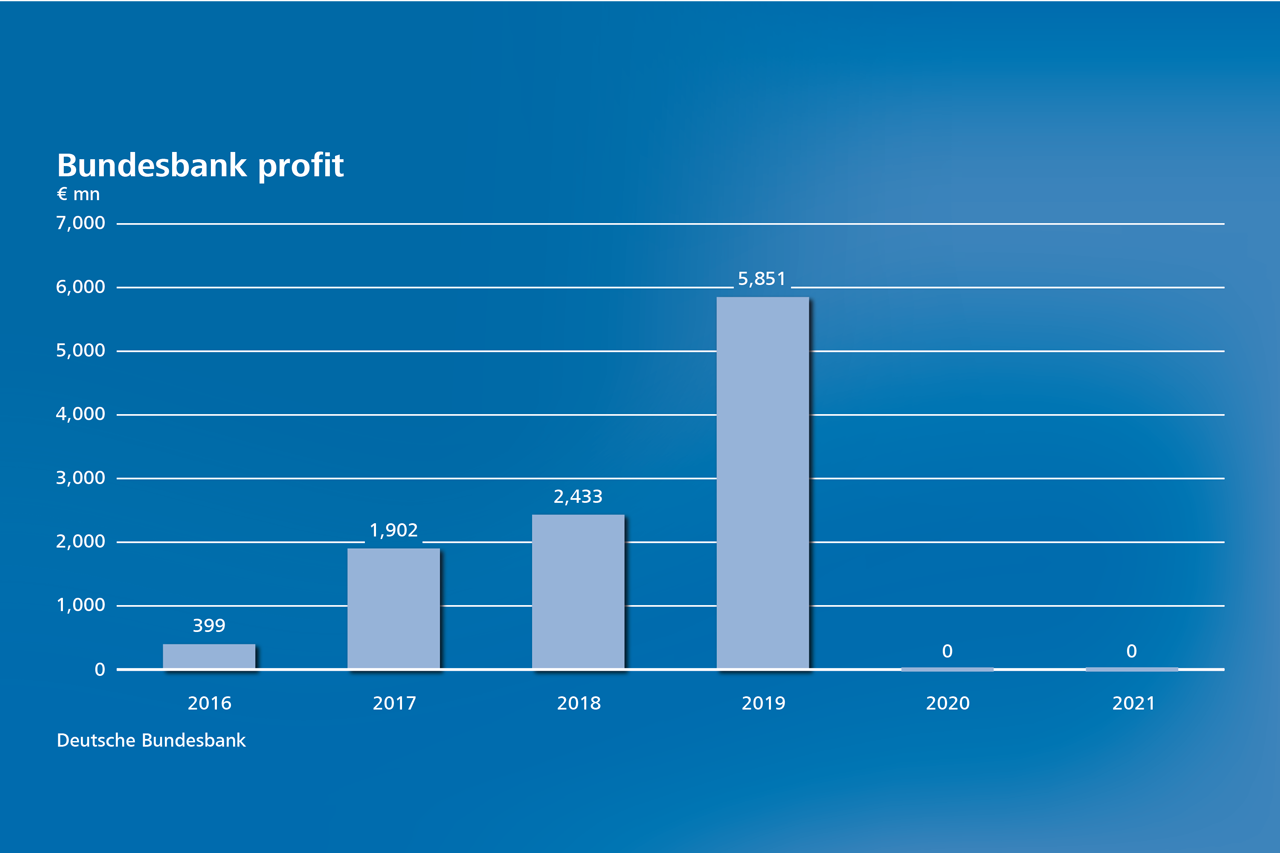

The Deutsche Bundesbank has presented a balanced result for the year 2021. As in the previous year, the Bank is not transferring any profit to the Federal budget. Explaining this decision, Bundesbank President Joachim Nagel said it was necessary to further increase the risk provisions on account of the emergency monetary policy measures taken to counter the impact of the pandemic. “In the years 2020 and 2021, the risks on our balance sheet increased substantially overall compared with the pre-pandemic period,”

Dr Nagel said in remarks on the Bundesbank’s annual accounts.

The Bundesbank President expressed his shock at Russia’s attack on Ukraine. “Our thoughts are with the people in Ukraine and the suffering they are enduring under this aggression,”

he said, adding that he decisively supports the agreed financial sanctions imposed on Russia. “The Bundesbank is implementing these measures in Germany”

, Dr Nagel explained.

Higher inflation forecast for 2022 expected

In Dr Nagel’s words, it is not yet possible at the present time to reliably estimate what effects the war will have on economic developments in Germany. What is clear is that a further surge in energy prices will also affect consumer prices. “I expect we will yet again have to raise our inflation forecast for Germany in 2022. We already thought in February that inflation as measured by the HICP could conceivably come to 4½%. The Bundesbank’s experts now believe that the inflation rate could reach 5% on average for the year,”

Dr Nagel said. “The euro area is also expected to record a high rate of inflation. We need to keep our sights trained on the normalisation of our monetary policy.”

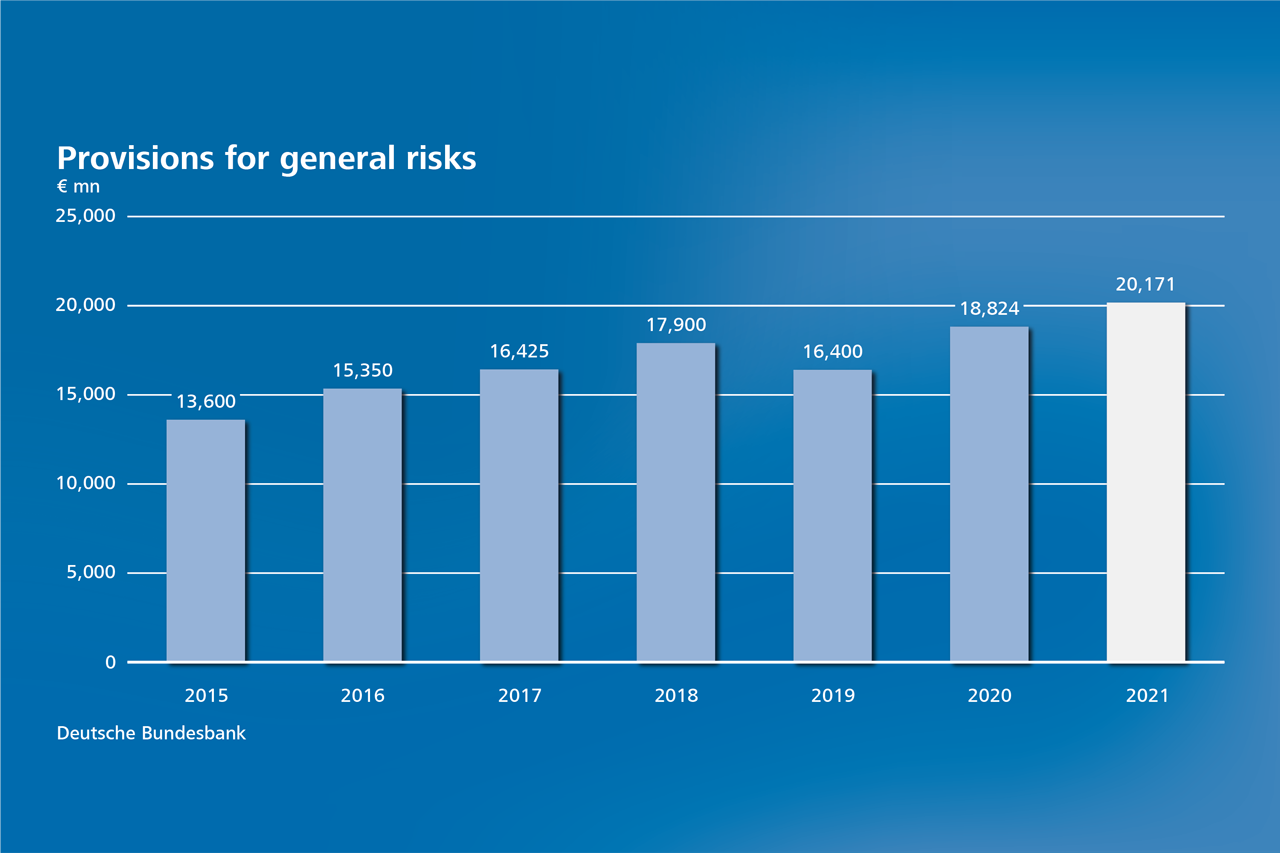

Balance sheet risks significantly increased

The Bundesbank’s balance sheet for 2021 shows that risks have increased. Interest rate risk was significantly higher in the last two years, mainly on account of the pandemic emergency purchase programme (PEPP). At the same time, the comprehensive purchases of securities, which also included corporate bonds, have added substantially to the Bank’s credit risk. “Being a prudent central bank, we need to set aside provisions for these risks,”

the Bundesbank President said, noting that he expects risk provisioning to be stepped up further in the 2022 annual accounts.

In financial year 2021, the Bank increased its provisions for general risks by €1.3 billion, the amount of the available result for the year, to €20.2 billion. In 2020, a more favourable earnings situation meant that the Bank had been able to allocate €2.4 billion to this item. The past year, however, saw net interest income, the most important item in the profit and loss account, contract from €2.9 billion to €2.5 billion. Furthermore, a one-off effect on staff provisions sent staff costs a significant €0.5 billion higher to €1.1 billion.

{kind=link}

Total assets reach new record level

“Total assets came to just over €3 trillion, the highest level in the history of the Bundesbank. This puts them 19% higher than the previous year’s record level of €2.5 trillion,”

explained Johannes Beermann, the Bundesbank Executive Board member responsible for accounting and controlling.

The main source of growth on the assets side of the Bundesbank’s balance sheet was the increased volume of euro-denominated securities held as part of the monetary policy asset purchase programmes, in particular the PEPP. Lending related to monetary policy operations was up as well, primarily on account of the third series of targeted longer-term refinancing operations (TLTRO-III) offered to credit institutions at particularly favourable terms in response to the pandemic. Liquidity inflows from other European countries were another factor contributing to balance sheet growth. These were reflected in an increase of €125 billion in the TARGET2 claim on the European Central Bank to around €1.3 trillion.

On the liabilities side of the balance sheet, the domestic provision of liquidity combined with liquidity inflows from abroad led to a considerable increase in deposits, as a result of which just over a quarter of all deposits of credit institutions throughout the Eurosystem are held with the Bundesbank.