Basel III reform package: Bundesbank sees no impediments to SME funding

The European Commission has presented its proposal for transposing the bank capital rules that were revised as part of the Basel III reform package into European law and for applying them from 2025. The Commission’s proposals have attracted public debate, with critics claiming that the additional requirements would hit the funding of small and medium-sized enterprises (SMEs) in particular. The Bundesbank, meanwhile, does not believe the legislative proposal will impede SME funding: “The roughly 1,300 German institutions that primarily fund SMEs and use the standardised approach will hardly be affected by rising capital requirements,

” says Joachim Wuermeling, the Bundesbank Executive Board member responsible for banking supervision.

SMEs – defined in the Capital Requirements Regulation (CRR) as firms which have an annual turnover not exceeding €50 million – are largely financed by institutions that use the standardised approach for credit risk. This corresponds to just under 70% of the credit volume, Bundesbank experts say. These roughly 1,300 German institutions will see no changes as a result of the Commission’s proposed legislation. The Commission is proposing to leave the existing SME supporting factor (SF) unchanged: when this SF is applied, the 100% risk weight that would normally be allocated in the EU can be reduced by up to almost a quarter. Therefore, these firms will see no increase in their funding costs, the Bundesbank has found. For enterprises – i.e. SMEs and non-SMEs alike – funded by institutions that use the standardised approach, funding costs would actually become even lower in some cases. According to the Commission’s proposals, if an enterprise has a good external rating, the risk weight for a rating of BBB+ to BBB- would be 75%, rather than 100% as hitherto.

Transitional arrangements until the end of 2032

For institutions that use internal models of their own to compute their capital requirements, the output floor will, in future, limit the extent to which banks can lower their capital requirements relative to the standardised approaches. These calculations will also be subject to the relief outlined above. The Commission is furthermore proposing a transitional arrangement for internal model institutions, which would see them being allowed to apply a risk weight reduced by 35% when calculating the risk-weighted assets (RWAs) for the output floor in the case of certain corporate exposures, at least until the end of 2032. This approach is called a hybrid approach because it came about by blending two approaches that actually conflict under the Basel Standard. It applies to exposures to “investment grade” unrated corporates and SMEs with a suitably low probability of default. Bundesbank experts say the actual effect of the output floor, which is to reduce variability in the capital calculations based on the standardised approaches and internal models, is significantly reduced as a result. They also note that the fully loaded output floor of 72.5% will only come into force in 2030, meaning that the supply of credit to the economy is not in danger. Some credit exposures, however, might see an increase in lending rates.

Bundesbank experts present a number of examples to illustrate how the proposed new rules will affect SMEs. For example, an (unrated) loan of €4.8 million to an SME is currently, on average, subject to a risk weight (RW) under the standardised approach of 80% (100% RW x SME supporting factor of approximately 0.8 for this exposure). Under the internal ratings-based (IRB) approach, loans to SMEs with a low probability of default (investment grade) are currently subject, on average, to an RW of 32%, the remainder to 80%.

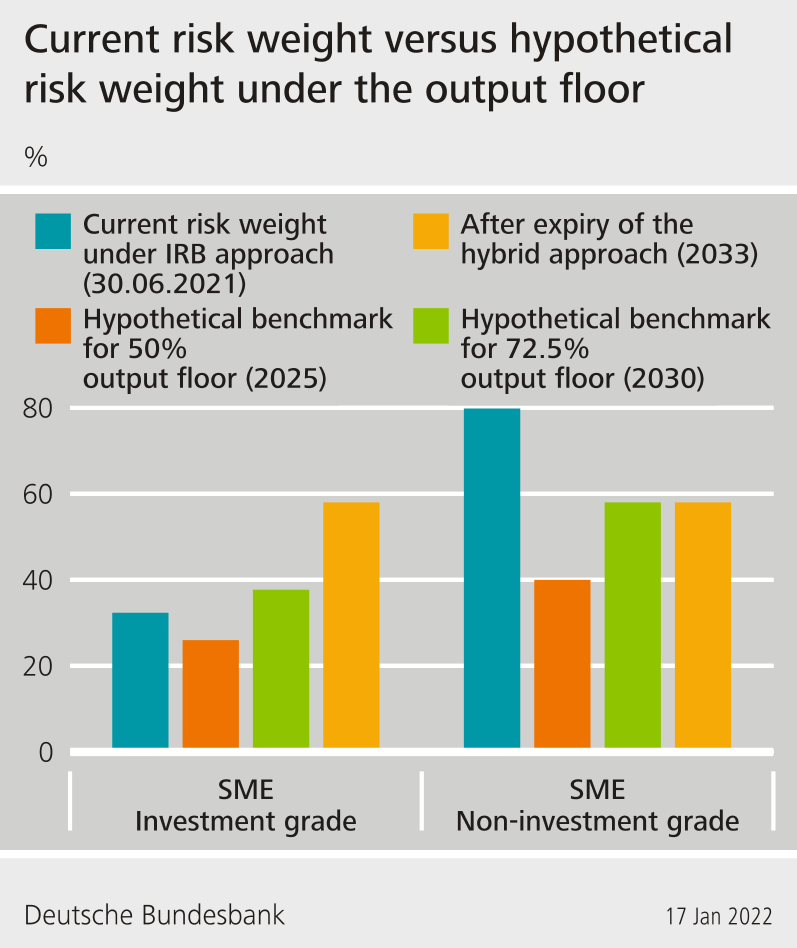

The chart below (Chart 1) shows the changes in risk weights for corporate exposures in comparison to the average risk weights currently reported for such exposures at institutions using the IRB approach that are constrained by the output floor. The Bundesbank’s experts point out that the output floor applies at the bank-wide level and not at the level of individual exposures or portfolios, meaning that the risk weights in the chart for the years 2025, 2030 and 2033 should be understood as maximum values. They say that offsetting effects with other risk areas in which only standardised approaches are used, such as operational risk, were not factored in. Furthermore, the experts explain that the reported average risk weights in 2021 relate both to externally rated and unrated enterprises, while the analysis of the impacts on the risk weights in 2025, 2030 and 2033 relates only to unrated enterprises, which means it is a conservative estimate. The applicable risk weights following implementation of the legislative proposal of the European Commission are shown for 2025 (assumption: initial application of output floor at 50%), 2030 (assumption: full introduction of the output floor at 72,5%) and 2033 (assumption: hybrid approach is no longer in force). The introduction of the output floor limits the internally calculated risk weights in comparison to the prudentially prescribed risk weights in the standardised approach.

The Bundesbank’s experts say that the use of the proposed hybrid approach would reduce the risk weight at institutions using the IRB approach to 26% in 2025. Where the output floor applies, the maximum possible risk weight for non-investment grade SMEs would fall from the current level of 80% to 40%, they explain. They point out that as of 2030, the risk weight would rise permanently to a maximum of 58%, which is 22 percentage points lower than the status quo.

The Bundesbank’s experts explain that the risk weight for investment grade SMEs would rise to a maximum of 38% as of 2030, and to a maximum of 58% following the expiry of the hybrid approach, which is 26 percentage points higher than the status quo.

However, they also note that changes in the risk weights of institutions using the IRB approach would only occur when they are constrained by the output floor. For all other institutions, they say that higher risk weights and thus higher financing costs for the real economy are not to be expected. According to the Bundesbank’s experts, the output floor was introduced with the intention of reducing undue fluctuations in the RWA calculations and curbing aggressive modelling by the institutions. The Bundesbank welcomes the fact that potentially underestimated risks are now being backed by capital.

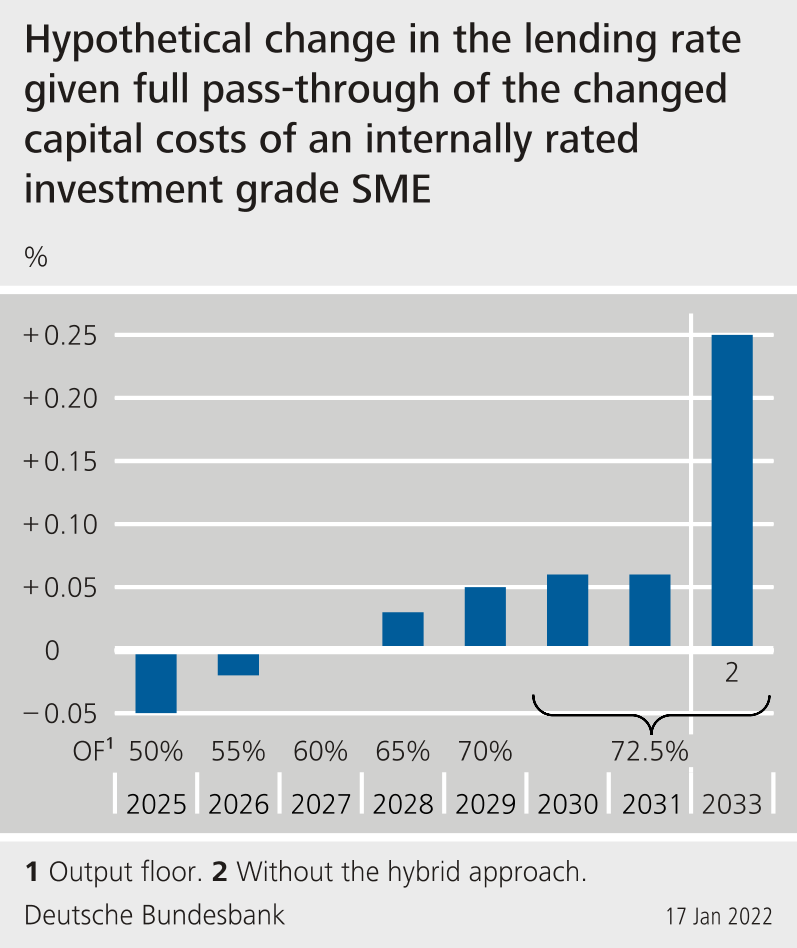

If the institutions fully pass on the capital requirements resulting from the increased risk weights to their corporate clients, an increase in lending rates is to be expected, say the Bundesbank’s experts. Chart 2 shows these possible changes over the phasing in of the output floor between 2025 and 2029, as well as with and without the impact of the hybrid approach. By way of example, the corporate financing assumed here is a loan to an investment grade SME in the amount of €4.8 million. The supporting factor for SMEs is around 0.8 in this case. During the introductory phase the interest costs would fall initially, say the experts, before rising again slightly as of 2028. Following the full introduction of the output floor, the interest cost of such a loan would rise by a maximum of 6 basis points for regulatory reasons, they explain. Only following the expiry of the hybrid approach as of 2033 would a rise of 25 basis points be possible, they say.