Why central banks should aim for a positive inflation target Research Brief | 46th edition – May 2022

The rate of inflation has a bearing on the relative price of individual products and therefore on demand for those products. Using new micro price data, we investigate how high the optimal inflation rate must be to prevent relative product demand from being distorted. Contradicting a common claim, we find that the optimal rate is not zero for a large part of the euro area, but is, in fact, clearly in positive territory.

With a few exceptions (e.g. petrol prices), the prices of individual goods are not normally adjusted on a continuous basis. As a result, relative product prices become distorted when inflation is too high or too low. This long-established effect of inflation is firmly embedded in macroeconomic theory models. Relative prices are affected by inflation through at least two channels. First, inflation reduces relative product prices. As long as the price of a product remains unchanged, inflation – i.e. a rise in the average price via price increases in all other goods and services – means that the product in question becomes cheaper in relation to other products over time. Second, enterprises that reset their prices set them higher as they are anticipating an inflation-induced price drop.

Distorted relative prices affect relative product demand in their turn, meaning that demand for certain products is then either too strong or not strong enough simply because prices are not continuously being adjusted. From a macroeconomic perspective, then, price distortions are a key source for the economic costs of inflation. In a new study (Adam, Gautier, Santoro and Weber 2021), we estimate the inflation rate that would reduce these costs to a minimum for Germany, France and Italy.

Zero inflation as a reference point?

In many macroeconomic theory models, inflation close to zero minimises the economic costs resulting from price distortions. This is because such models do not consider the fundamental forces driving trends in relative prices over time. In part, this is why zero inflation has become entrenched as an important reference point. However, once allowances are made for trends in relative prices – for instance, because products with increasing lifespans can be produced more efficiently, which ought to translate into declining prices – inflation can play a part in creating these desirable relative price trends. Although product prices themselves are rarely adjusted, the right level of inflation allows relative product prices to fall in line with potential efficiency gains over the lifetime of a product. The question surrounding the optimal inflation rate then becomes a question of which relative price trends are in fact justified by fundamental forces such as manufacturing efficiency.

Relative price distortion aside, there are, of course, other arguments for optimal inflation rates different from zero – the opportunity costs of holding money, for example, or the zero lower bound. Here, however, these arguments have been disregarded.

Our study is based on the micro price data from the official consumer price indices in Germany, France and Italy. These data have only recently been made available as part of the Eurosystem’s Price-setting Microdata Analysis Network (PRISMA), and comprise more than 80 million price observations over the period 2010 to 2019. Depending on the country, the data cover between 64% and 83% of the representative basket of consumer goods. Our empirical analysis leverages these data to estimate trends in relative prices over product lifetimes in many different product categories. An earlier theoretical analysis (Adam and Weber, forthcoming) shows that given plausible assumptions, these estimates can be interpreted as desirable trends in relative prices. The theory also illustrates how the estimated trends should be aggregated to determine the country-specific optimal inflation target and how the macroeconomic costs of sub-optimal inflation can be calculated.

Optimal inflation rate varies across countries and product categories

Our empirical analysis for the baseline period 2015 (2016 for Italy) to 2019 shows that the optimal inflation rate minimising the welfare costs associated with relative price distortions is clearly positive for each of the three largest euro area countries. Depending on the precise specification of the empirical analysis, this rate lies between 1.1% and 2.1% in France, 1.2% and 2.0% in Germany, and 0.8% and 1.0% in Italy. The weighted average across all three countries produces an optimal inflation rate of between 1.1% and 1.7%. These clearly positive optimal inflation rates can be explained by the fact that relative prices ought to decline in all three countries on account of fundamental forces such as manufacturing efficiency over the product lifetime. Positive inflation then reduces distortions in relative prices that arise because product prices are adjusted only irregularly. What this also means, however, is that the reference point of zero inflation for these countries is empirically less robust than previously thought.

| Table 1: Estimates of the optimal inflation rate (in % per year) in the baseline period and weightings (in %) in the consumption basket | ||||||

Food | Non-energy industrial goods | Services | ||||

Optimal inflation | Weighting | Optimal inflation | Gewicht | Optimal inflation | Weighting | |

France | 0.2 | 30.9 | 4.9 | 34.5 | 0.1 | 34.3 |

Germany | -0.1 | 26.5 | 5.5 | 39.3 | -0.9 | 34 |

Italy | 0 | 26.4 | 2.6 | 34.4 | -0.1 | 38.7 |

To gain a better understanding of the differences between the countries, let us examine the estimated optimal inflation rates for the broad product categories “Food”, “Non-energy industrial goods” and “Services” in Table 1. The estimated rate for food is close to zero in all three countries. The same is also true for services in France and Italy. The estimated rate for services in Germany is actually negative, meaning that German services become more expensive over their lifetime in relative terms. However, Table 1 also shows that the positive optimal inflation rates at the country level result from strongly positive optimal rates for industrial goods. These rates are close to 5% for France and Germany but considerably lower for Italy. Thus, the optimal overall inflation rate for Italy is lower than for Germany or France. Optimal goods price inflation is so low in Italy because seasonal price reductions in the fashion-driven goods category “Clothing & footwear” take place simultaneously there on almost all products and therefore have less of an impact on relative prices.

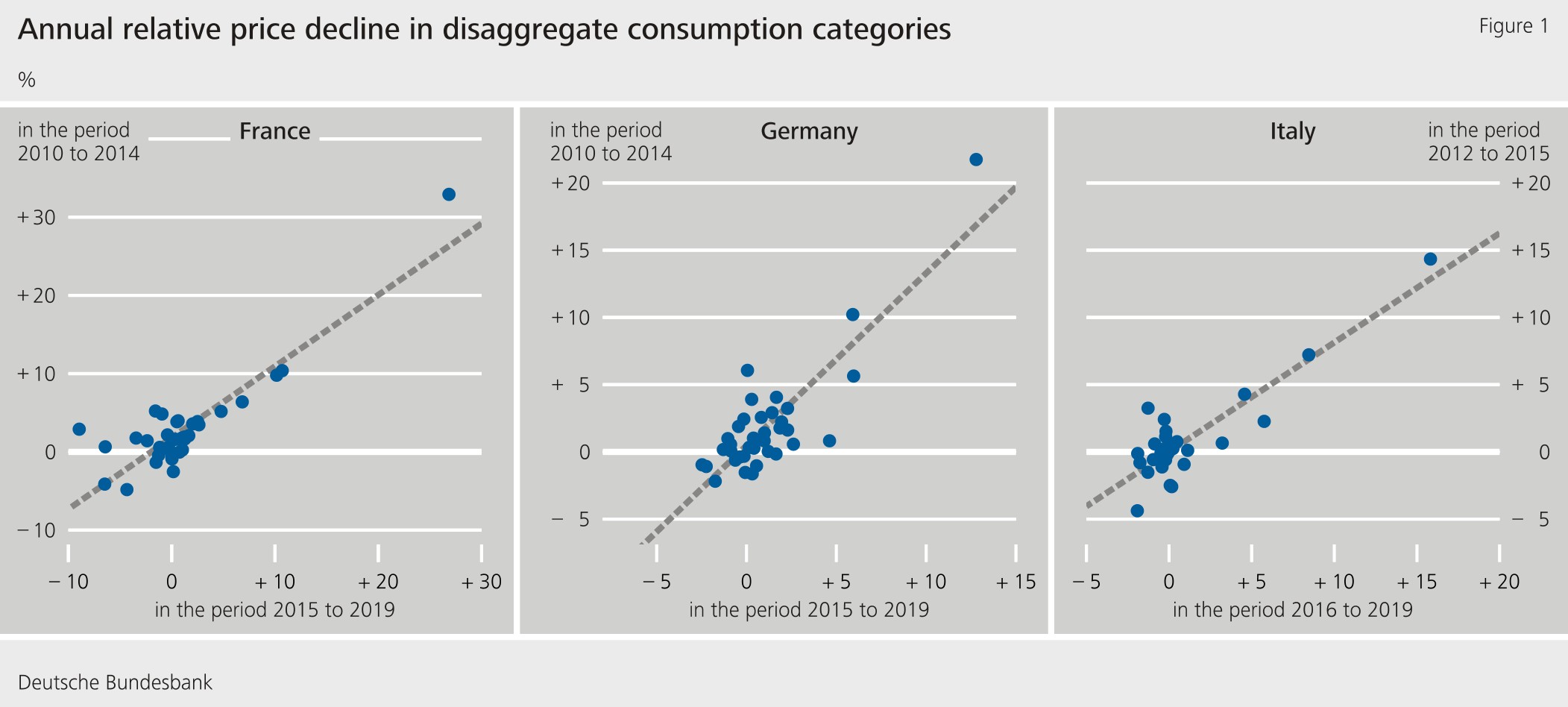

One key question is how strongly optimal inflation rates vary over time. Figure 1 shows a high correlation of relative price trends between the baseline period and an earlier time period. This suggests that, even for finely delineated product categories, the optimal rates are surprisingly stable over time. The optimal inflation rates for the baseline period could therefore also serve as a good indicator of optimal inflation rates after the pandemic.

Estimates of the optimal inflation rate that minimises the welfare costs associated with price distortions allow conclusions to be drawn regarding the costs of various inflation scenarios. If inflation returns to the same moderate level as in the 2015-19 period post-pandemic, the estimated costs will be low, as the inflation rate in each country during this period was close to the optimal rate. Were inflation to remain at zero over a longer period – that is, at the reference value deemed optimal in many theoretical models – the estimated welfare costs on an average across the countries under review would correspond to a 5% reduction in the present value of lifetime consumption. Should the inflation rate persist at its current level for a long time, the estimated costs would be considerably higher still.

Conclusion

The availability of detailed micro price data allows the existing theories on the optimal inflation rate to be developed further. Where economic reasons for a decline in relative prices over the product lifetime are taken into account, the inflation rate that reduces distortion in relative prices is clearly positive and lies between 1.1% and 1.7% in the three largest euro area countries. The previous reference point of zero inflation would therefore appear to be empirically less robust than previously assumed for these countries. Estimates of the optimal inflation rate played a role in the further development of the ECB’s monetary policy strategy last year and are likely to continue doing so in future.

Disclaimer |

The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Data sources

French micro price data were provided by the Institut national de la statistique et des études économiques (Insee) via the Centre d’accès sécurisé distant aux données (CASD). Micro price data for Germany were provided by the Research Data Centre of the Federal Statistical Office (Destatis) and of the Statistical Offices of the Federal States (“Einzeldaten des Verbraucherpreisindex 2018”, EVAS number 61111, 2010-2019, DOI: 10.21242/61111.2010.00.00.1.1.0 to 10.21242/61111.2019.00.00.1.1.0). Micro price data for Italy were provided by the Istituto nazionale di statistica (ISTAT).

References

- Adam, K. and H. Weber (forthcoming), “Estimating the optimal inflation target from trends in relative prices”, American Economic Journal: Macroeconomics.

- Adam, K., E. Gautier, S. Santoro and H. Weber (2021), “The case for a positive euro area inflation target: evidence from France, Germany and Italy”, London, Centre for Economic Policy Research.

Authors | ||

| Klaus Adam Professor of Economics, University of Mannheim | Erwan Gautier Economist at Banque de France | Henning Weber Economist at the Bundesbank’s Research Centre |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein