Financial stability and credit markets in Europe: Opportunities and risks in the current setting Dinner talk at the second Süddeutsche Zeitung conference on the topic of "private debt and direct lending"

Check against delivery.

It is nearly ten years ago to the day that the global financial crisis reached its initial peak. The global economic crisis that followed was the most severe since the Great Depression. In the wake of the crisis, reforms to the financial markets were introduced with the aim of making financial markets more resilient, and many of these reforms have already been implemented. After all, the stability of the financial system is a key prerequisite for an efficient and dynamic economy. Just as preventive medical care and a good immune system help to limit the effects of disease, a prudent approach coupled with good defences helps the financial system to mitigate the effects of economic shocks. The question today is how far the international financial system is better placed to deal with unexpected developments than it was just a decade ago.

The global economy is currently fraught with uncertainty on a number of fronts. Geopolitical tensions have escalated, and trade disputes have erupted, some of which threaten to tip into a trade war. In Europe it is unclear under what circumstances the United Kingdom will leave the European Union. Germany's economy may be booming right now, but every period of growth, no matter how long it lasts, ultimately gives way to an economic downturn. How well prepared is the German financial system to face a potential economic slump? What happens if risks materialise?

1 With the global economy in good shape and interest rates low, risks can be underestimated.

The world economy is currently doing well. According to calculations by the International Monetary Fund (IMF), global growth will amount to 3.9% both this year and next year (IMF 2018). For the coming year, the IMF is forecasting only a slight fall in growth from 2.4% to 2.2% for industrial countries and from 2.2% to 1.9% for the euro area.

At the same time, the IMF has emphasised that this growth is not without risk and that some risks are already materialising. For example, the debt level in some emerging market economies has gone up sharply in recent years, and these liabilities are often denominated in foreign currency. This has created vulnerabilities which have surfaced in recent weeks and months. For example, the Turkish lira has lost nearly 40% of its value in the year to date, and the Argentine peso as much as 50%, or thereabouts.[1] Thus far, market participants have regarded these issues as relatively isolated incidents. Currently, the effects on global financial markets are small. But possible contagion effects and interactions with global risks are difficult to forecast.

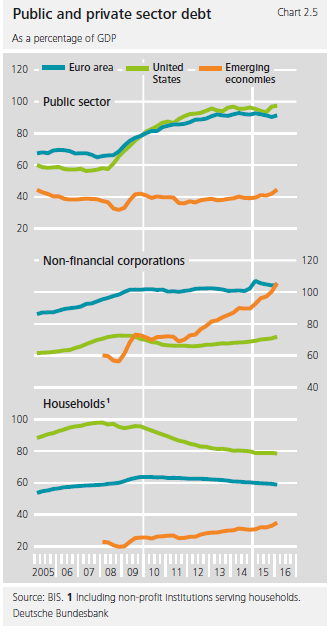

Public and private debt, which are close to their all-time highs in global terms, are one of the global financial system’s vulnerabilities. Industrial countries which bore the brunt of the crisis have seen public debt levels balloon, largely on the back of measures to shore up the financial sector. This has shifted risk from the private sector to the government sector. In many emerging market economies, by contrast, it is above all (non-financial) private sector debt that has increased. In fact, it has more than doubled in recent years. Compounding this situation further, some of these sectors are highly exposed to currency risk.

Banking sector debt has generally diminished in recent years. Measured in terms of risk-weighted assets, the capitalisation of the banking sector at the end of 2017 stood at roughly 17% in the euro area, compared with 14.2% in the United States. However, measured in terms of total (unweighted) assets, these ratios were significantly lower, at 5.8% in Europe and 9.3% in the United States (CGFS 2018). It should be noted that, due to the differing accounting standards, these figures are not directly comparable.

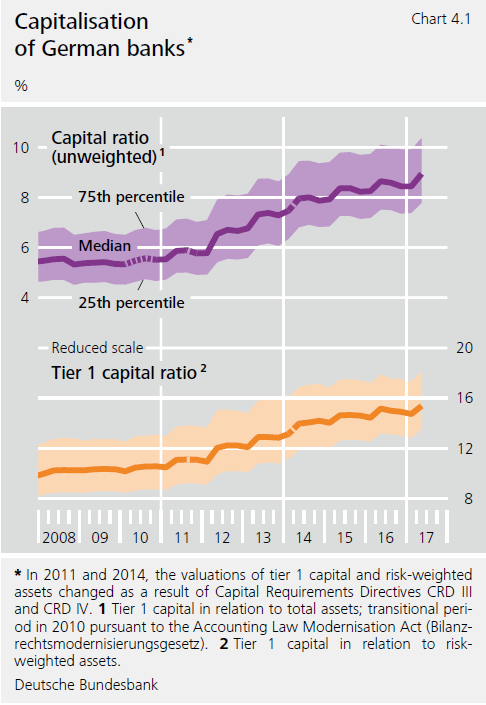

In Germany, banks’ tier 1 capital ratio – i.e. tier 1 capital in relation to risk-weighted assets – has climbed from from 9% at the start of 2008 to 16.4% at the start of 2018 (Chart). The unweighted capital ratio, i.e. tier 1 capital in relation to total assets, rose in the same period from 3.1% to 6.2%.

{kind=link}

Furthermore, capital adequacy levels sometimes vary significantly from one bank to the next. The tier 1 capital ratio of the large, systemically important financial institutions in the first quarter of this year stood at 16.9%, while the unweighted capital ratio came to 4.9%. For small and medium-sized banks, the equivalent figures were 15.6% and 8.1%.

The wide variation in capital ratios shows that the amount of capital banks have to cushion against unexpected events depends not least on how well future risks are captured by the risk weights. At the moment, the economic environment in Germany is highly favourable. The German economy has now been expanding for nine consecutive years, which is the longest period of growth since German reunification. According to the Bundesbank’s projections, the economic boom is set to continue, with gross domestic product forecast to rise by 2% this year and 1.9% next year (Deutsche Bundesbank 2018). Enterprises and households alike can borrow cheaply, and they have accumulated comfortable capital buffers. The number of insolvencies and credit defaults is low, and valuations in financial markets are high. This upbeat macroeconomic situation is conducive to a gradual rise in interest rates. Assuming the economy does indeed follow its expected path, the risks to financial stability will probably be limited.

But what if the economy takes an unexpected turn for the worse? What if there is an unforeseen downturn in real economic momentum and interest rates remain low – and close to zero – for even longer, or if political risks materialise and risk premiums spike in financial markets?

A resilient financial system needs to be in a position to weather such scenarios, which though unexpected, cannot be fully ruled out. This is especially true in boom periods, because the longer these continue, the more market participants tend to take them for granted and not prepare for gloomier times. Unexpectedly weak growth and an increase in volatility could then have even greater repercussions.

Scenarios like this are not out of the question, even for Germany. The German economy is closely interlinked with the global economy, so it would be hit hard by possible abrupt corrections in international markets. Possible negative effects can be amplified if many market participants are exposed to similar risks.

2 The German financial system is vulnerable to negative macroeconomic developments.

Over the last decade, German banks have improved their resilience and built up capital. However, this capital is also counterbalanced by greater macroeconomic risk. The effects of risks on individual banks is something that supervisors keep a watchful eye on. However, an assessment of the overall risk situation needs to look at more than just individual participants or sectors in isolation. A macroprudential, or systemic, perspective is therefore needed to complement the microprudential approach. This way, it is possible to take into account contagion mechanisms in the financial system that can give rise to systemic risks. After all, problematic developments in individual parts of the financial system can ripple out across institutions and ultimately take their toll on the real economy. These amplification effects can particularly come to bear if many banks are exposed to the same risk and if macroeconomic risks correlate strongly with each other.

Monitoring systemic risk in Germany is the task of the German Financial Stability Committee (AFS). The Committee consists of representatives from the Federal Financial Supervisory Authority (BaFin), the Deutsche Bundesbank, and the German Federal Ministry of Finance, which acts as chair. In its latest report to the German Bundestag, the Committee examined the state of Germany's financial system (German Financial Stability Committee 2018).

At present, there is a danger that future economic risks might be underestimated. For example, there could be an unexpected downturn in the economy, which would result in insolvency rates and thus credit risks rapidly rising. Reserves and capital might be insufficient to cover the losses from such an unexpected event, particularly if risk assessments scarcely take into account periods of crisis fraught with economic downturns and correspondingly higher credit default rates, or even ignore them altogether.

In the current long period of economic expansion, there is the possibility that credit risks are being underestimated in the real estate market. This market, which is significant for Germany in macroeconomic terms, could harbour risks to financial stability. This would be the case, for example, if a sharp increase in real estate prices led to an excessive rise in lending and a loosening of credit standards. Prices are continuing to rise dynamically. Bundesbank estimates indicate that house prices in German towns and cities were overvalued by between 15% and 30% in 2017. Growth in residential loans currently stands at 4.3% (second quarter 2018) and thus below its long-term average of 4.8%.[2] At the same time, there is no clear evidence to suggest that banks have loosened their credit standards for residential loans. However, given the strong upward pressure on prices in recent years, it cannot be ruled out that the value of loan collateral is being overestimated. The value of loan collateral will probably turn out to be lower, particularly in the event of an economic downturn. This increases the risk of unexpected losses arising as a result of defaults on loans.

One key macroeconomic risk that the German financial system is exposed to is interest rate risk. In recent years, banks have sharply increased the share of new loans with long interest rate lock-in periods. The share of newly issued loans with an interest rate lock-in period of over ten years stood at 45% in the second quarter of 2018; at the start of 2010, this share was markedly lower, at 26%. By contrast, bank funding tends to be of a short-term nature, and often at variable interest rates. This means that banks have become more vulnerable to a potential rise in interest rates. An abrupt increase in interest rates would drive up banks’ financing costs, but their interest income would rise less quickly to begin with.

If risks materialise that are larger than expected, this could set negative momentum in motion in the financial system. In the short term, a critical situation is a particularly inopportune time for banks to raise capital in the markets, at the very time this capital would be needed to absorb losses. Individual banks would then have to shrink their balance sheets in order to fulfil the increased capital requirements. They would have to sell assets, scale back existing lines of credit to the real economy, or cut back on the issuance of new loans. If fire sales send securities or real estate prices plummeting, this can also take its toll on institutions for which loan losses were barely an issue to begin with.

3 Now is the time to strengthen the financial system’s resilience in readiness for tougher times ahead.

"The time to repair the roof is when the sun is shining

".[3] The International Monetary Fund has repeatedly drawn attention to this principle in recent times. Public sector budgets need to be put on a sustainable footing, debt levels need to be reduced, and budgetary leeway for more difficult times needs to be created.

That said, protection against unexpected macroeconomic developments also needs to be put in place in the financial system, too. Everyone should make provisions for unexpected developments to ensure that they can still service their debt if the economic conditions worsen. Unexpected developments can happen in the home market, but they can also occur in emerging market economies or other industrial countries and then spill over to Germany. Many mature economies are currently experiencing buoyant economic conditions, output gaps have been closed in many cases, and cyclical risks in the financial system are mounting.

Financial institutions with higher levels of capital are more robust and thus also make the financial system as a whole more resilient. If all market participants have strong defences, the risk of contagion falls. Unexpected events will then have less severe consequences.

However, resilience needs to be built up in good time – once a recession has begun it may already be too late. It's rather like building up protection against the flu. Once a wave of influenza has broken out, it is too late to get vaccinated. The only problem is that when the weather is fair and you feel well, it is all too easy to forget that times may also take a turn for the worse.

It is therefore important to take preventive action. If the financial system is not resilient enough, this can amplify an economic downturn. Banks would then excessively curtail their lending precisely when the economy is already running into difficulties. This is precisely what happened around the globe in the last crisis. Defences therefore have to be built up when times are good.

Currently, the sun is shining on the markets, we are experiencing the longest period of growth since the 1970s, and credit losses are low. Now is the time to build up sufficient capital, which will strengthen the resilience of individual institutions and the financial system as a whole in the event of an economic downturn.

4 List of references

- Committee on the Global Financial System – CGFS (2018). Structural changes in banking after the crisis, CGFS Papers No 60, January 2018.

- Deutsche Bundesbank (2018). June 2018 Monthly Report.

- German Financial Stability Committee (2018). Fünfter Bericht an den Deutschen Bundestag zur Finanzstabilität in Deutschland, June 2018.

- International Monetary Fund – IMF (2018) World Economic Outlook Update, July 2018.

- Source: Bloomberg, 14 September 2018.

- See the Bundesbank’s system of indicators for the German residential property market:

- https://www.bundesbank.de/Navigation/EN/Statistics/

Enterprises_and_households/System_of_indicators/

system_of_indicators.html - This quote is attributed to John F. Kennedy.