The crux of the matter with deposits: low interest rates squeezing credit institutions' margins Research Brief | 4th edition – June 2016

Persistently low interest rates are depressing German credit institutions' profitability – this is revealed in a survey undertaken by the Bundesbank and the German Federal Financial Supervisory Authority (BaFin). The banks will have to subject the sustainability of their business model to critical analysis.

The protracted low-interest-rate environment will, especially in the medium term, pose an enormous challenge for German credit institutions, since their business models depend to a large extent on net interest income. This is confirmed by the survey on the low interest rate environment conducted in 2015 by the Bundesbank and the German Federal Financial Supervisory Authority (BaFin). In mid-2015, the less significant institutions (LSIs) were asked about their expectations in the low interest rate environment. The significant institutions, which are supervised directly by the ECB, were, by contrast, the subject of the 2014 comprehensive assessment and, in some cases, are taking part in the 2016 EBA stress test that is currently being conducted. In light of this, they were not included in the survey on the low interest rate environment.

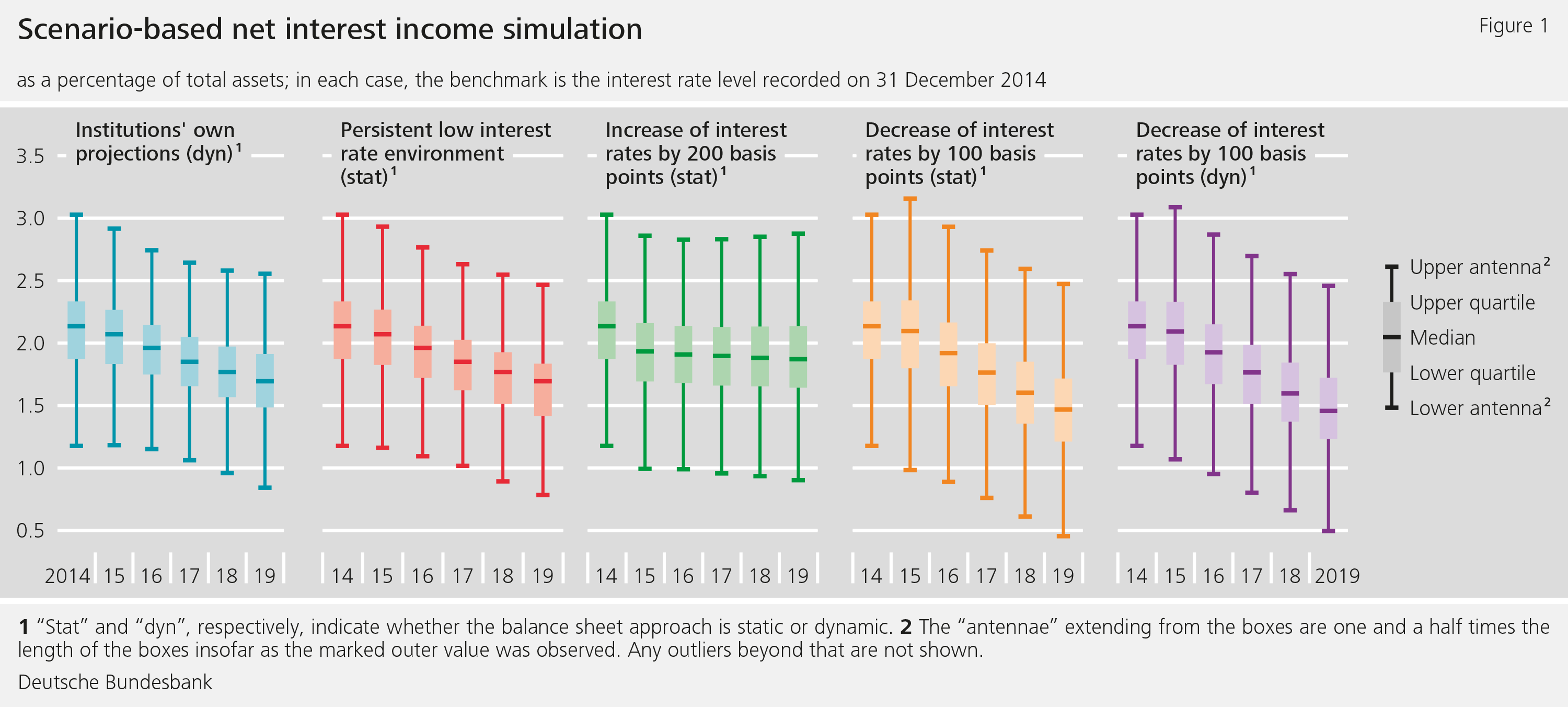

Around 1,500 German credit institutions submitted data on their profit and loss accounts as well as balance sheet items for their internal planning and projections for the period from 2015 to 2019 (plan). In addition, the banks had to prepare projections based on four further pre-defined interest rate scenarios. The low interest rate setting (LIR) scenario assumes that interest rates will persist at a low level. The "+200 basis points" ("+200 bp") and the "-100 basis points" ("-100 bp") scenarios, respectively, assume a sudden change in the yield curve by the said amounts starting from the baseline level at 31 December 2014. The latter scenario is to be calculated assuming both a static (stat) and dynamic (dyn) balance sheet. The definition of a static balance sheet specifies that there are no balance sheet adjustments over time.

Unfavourable outlook

The projections show that banks' profitability is coming under increasing pressure. In the median ("median bank"), the credit institutions expect their net interest income to decline by around 20% relative to total assets. The four scenarios present an even worse picture. The outlook is poor, especially in the scenarios in which the interest rate level shifts by -100 basis points, where the banks are expecting net interest income to fall by around 32%.

The persistent low interest rate environment is placing a strain on credit institutions' net interest income in two ways. First, banks are having to replace expiring, comparatively high-yield investments in the low interest rate setting with ones that are less well remunerated. Second, there is a limit to how far they can reduce the rates of interest that customers receive on their deposits. As a result of competition and endeavouring not to lose customers to their rivals, the de facto downward limit on the deposit rate, at least for private customers, so far appears to be mostly 0%. As soon as interest rates become significantly negative, if not earlier, customers might withdraw their deposits and hold them as cash.

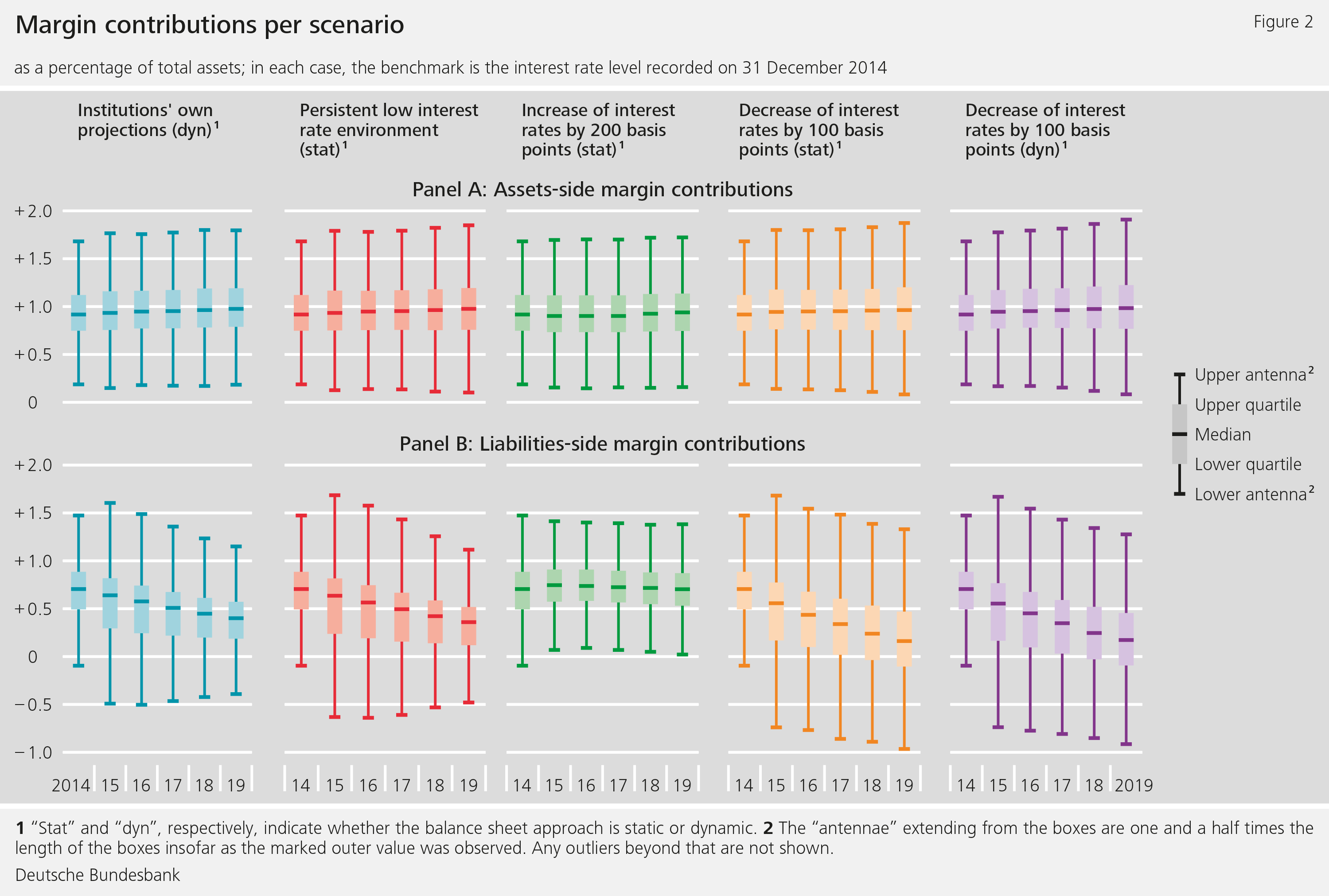

In order to analyse the changes in interest rate business more closely, net interest income was split into the structural contribution as well as the margin contributions on the assets and liabilities sides of the balance sheet. The structural contribution corresponds to the interest income which the banks achieve when they make a long-term investment using funds that are available in the short term. The assets-side margin contribution indicates the spread between a credit operation and an investment with the same maturity in the money or capital market. The liabilities-side margin contribution, by contrast, is the spread between a customer deposit and wholesale funding with the same maturity.

It is obvious from the target figures that the credit institutions expect no more than a slight increase in the spread between short-term and long-term interest rates. Consequently – assuming all other things are equal – the structural contribution should at all events be showing a slight increase. The declines in the expected net interest income can thus only be explained by the margin contributions.

The analyses in Figure 2 show that the assets-side margin contribution (Panel A) remains virtually approximately unchanged in all the considered scenarios. It can nevertheless be observed that the margin contribution from the liabilities side (Panel B) comes under noticeable pressure in all the scenarios except the "+200 bp (stat)" scenario.

No negative interest rates for customers

This is due to the following factors. As the banks see it, competition and customer behaviour imply, at least for private customers, a de facto interest rate floor of 0% on the liabilities side. Accordingly, at the time of the survey last year, banks did not expect to be able to pass on negative rates of interest to their private customers, even though such rates can be observed in the case of reference rates for short residual maturities in the market.

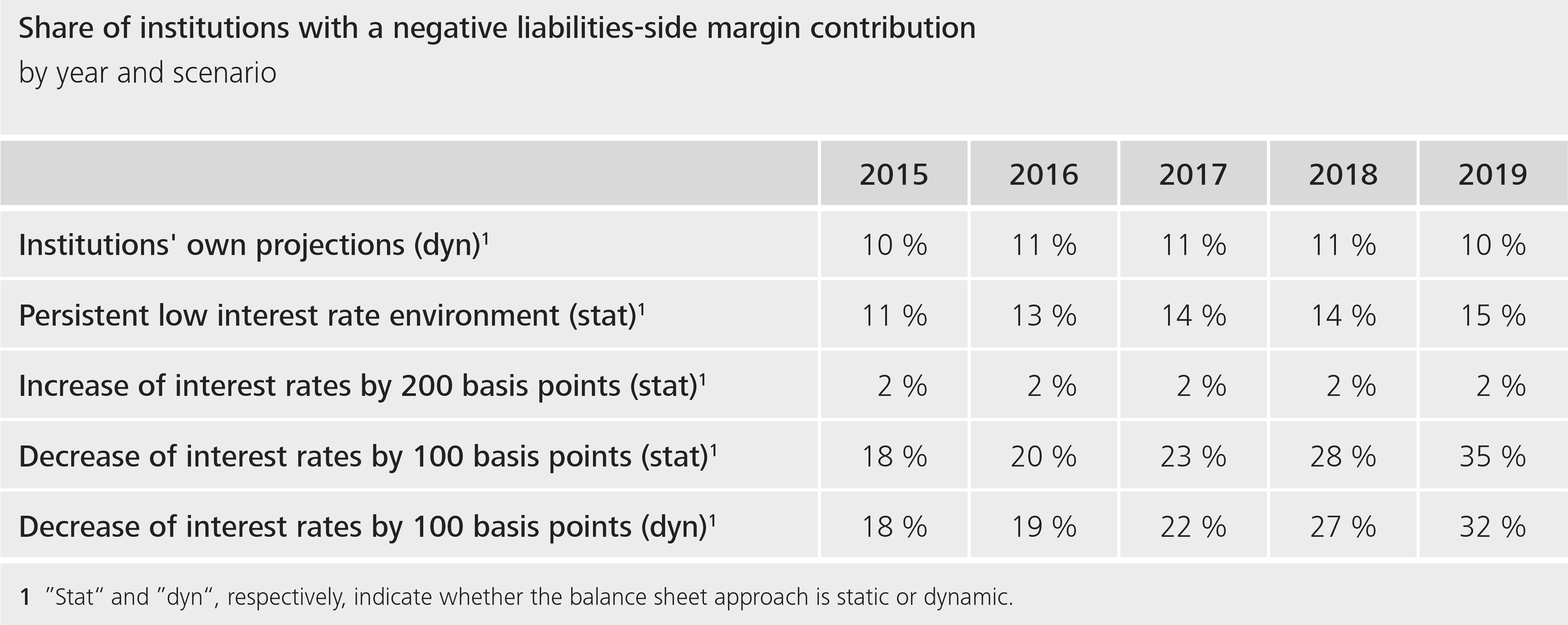

This is causing a collapse in the expected liabilities-side margin contribution and is even leading, in some cases, to markedly negative contributions to profit. According to the budgeted figures, the number of credit institutions showing negative liabilities-side margin contributions will increase from 4% in 2014 to 10% in 2019. In the interest rate scenarios based on a negative interest rate shock, as many as one institution in three is predicting a negative liabilities-side margin contribution for 2019.

Up to now, it has been an advantage for banks to obtain funding from customer deposits instead of (with the same maturity) through the market. In the wake of the low interest rate setting, this funding structure has increasingly become a burden for the credit institutions, as borrowing in the money and capital market is becoming perceptibly more attractive and, for some banks, has in fact already become a more favourable source of funding than customer deposits.

To counteract this, some institutions have already switched to charging negative rates of interest to institutional customers and enterprises. At the time of the survey, the participating institutions were not planning to do so with their private customers, however. Even in the negative interest rate scenario ("-100 bp"), most of the institutions do not assume that they would be able to demand negative rates of interest. Only 37.5% of institutions expect to be able, if necessary, to pass on negative interest rates on enterprises' deposits. With regard to the private customer segment, the relevant figure for credit institutions is only 16.4%. The banks are instead planning to expand their commission business. This relates to account management fees, for example, as well as customers' securities business.

Conclusion

A survey among around 1,500 German banks last year shows that the low interest rate environment is placing a growing strain on German credit institutions'expected profitability. The breakdown of net interest income shows that it is chiefly the interest rate spread between funding through customer deposits and wholesale funding which is having a negative impact. Declining profitability poses a challenge for the credit institutions and is forcing them to tap new sources of income and/or expand existing ones. Even though the good capital base currently represents a buffer for bad times, the institutions will have to examine how far this situation can equally be maintained under poorer macroeconomic conditions.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |