Short selling below the radar Research Brief | 10th edition – February 2017

A new EU regulation sheds the first light on the hitherto hidden practices of short sellers. This legislation requires short positions to be made public as soon as they exceed a certain threshold. How are market participants responding to this new transparency? A new study looks into this question.

In a covered short sale, an investor sells a security which they had previously borrowed for a fee over a certain period of time. The investor needs to repurchase the security at the end of the borrowing period, or earlier, in order to return it to the lender. If the price of that security falls during that period, the investor makes a profit; otherwise they suffer a loss. Hence, short selling can be a profitable strategy for investors who are expecting prices to decrease. It is this speculative feature of short selling which has mostly met with a negative public reaction, and criticism is particularly intense when markets go through phases of heavy losses. Yet at the same time, short selling is an important risk management instrument, and it is also used by market makers who regularly quote buy and sell prices in the markets, thereby ensuring a sufficient level of liquidity. There are a number of studies which indicate that short selling plays an important role in financial markets on account of its contribution to pricing efficiency and higher market liquidity (Beber and Pagano, 2013; Boehmer, Jones and Zhang, 2013).

The 2008-09 financial crisis was the cue for reforms to financial market regulation, one of which addressed the regulatory treatment of short selling. In November 2012 the European Union eventually adopted a uniform regulation on short selling which prescribed new transparency requirements for short sales of stocks. The new rules give supervisory authorities and every market participant an accurate and near-time overview of short sellers’ activities. The regulation consists of a two-tier reporting and publication system. First, if an investor’s net short position reaches 0.2% of a company’s issued share capital, they must report this to the national supervisory authority. Second, if the net short position is 0.5% or higher, the investor must even make this position public. Publication includes the name of the investor, the amount of their short position as well as the name and identifier of the stock in question. For the German stock market, a list of these short positions is available to the general public on the Federal Gazette's website.

Requiring individual investors to make their short positions public is a regulatory novelty, and it remains to be seen how investors respond to this new degree of transparency. It is frequently said that investors will seek to remain below the disclosure threshold as a way of keeping their cards close to their chest. Our current discussion paper (Jank, Roling and Smajlbegovic, 2016) uses the two-tier reporting and publication model set out in the EU’s short selling regulation to answer this question. In it, we analyse the short positions reported for the German stock market in the period from November 2012 to March 2015, as provided to us by the German Federal Financial Supervisory Authority (BaFin).

Cast a glance below the publication threshold

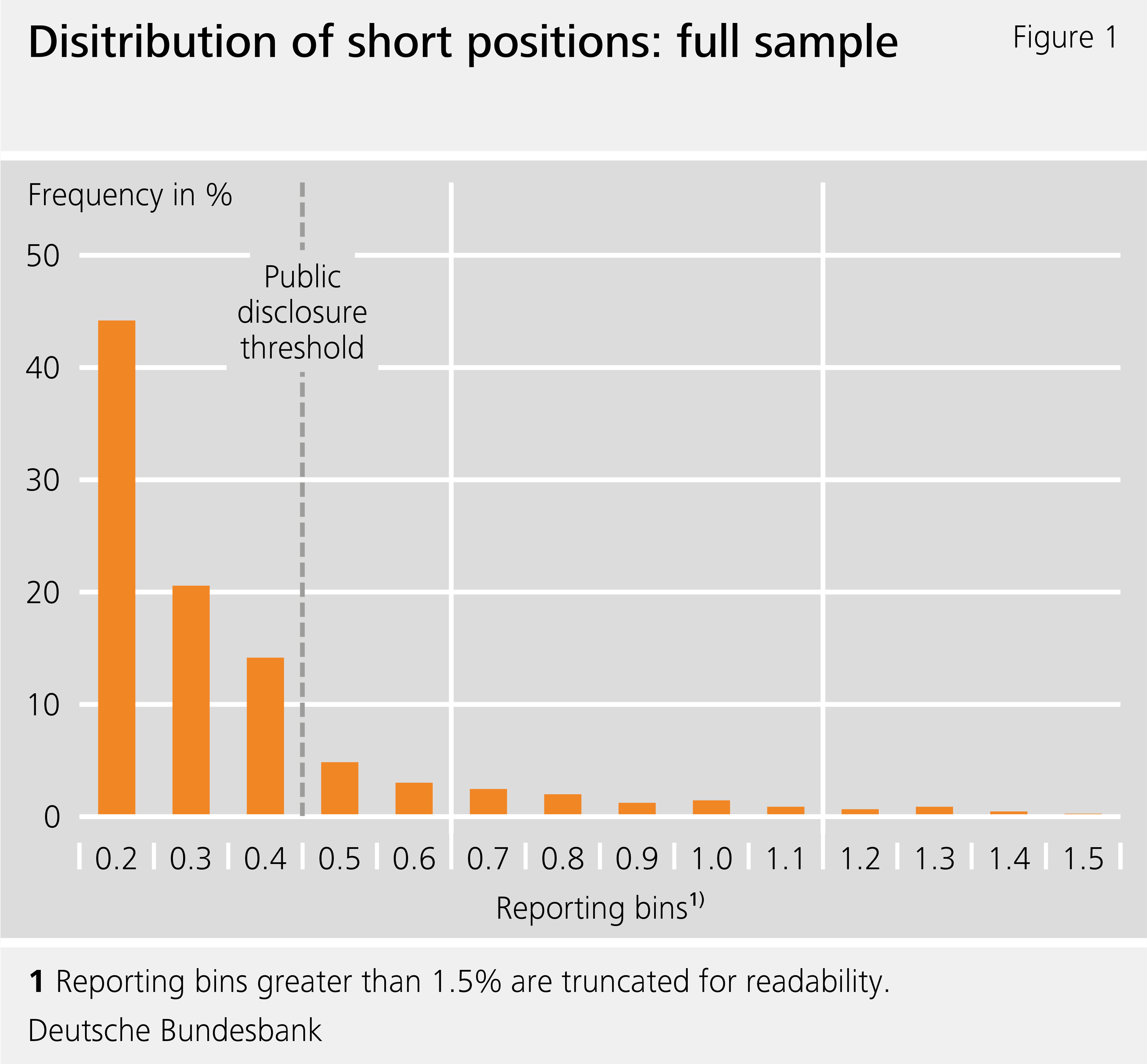

Figure 1 shows the frequency distribution of the reported short positions, with positions being grouped together in intervals that are 0.10 percentage point wide. Disclosed short positions account for around 21%, while the bulk of the reported positions (79%) are below the publication threshold. The final reporting interval below the public disclosure threshold – the one encompassing short positions between 0.40% and 0.49% (otherwise known as the 0.4 interval) – can deliver important insights on whether investors are avoiding publication. In case investors are looking to “fly below the radar”, we would expect to see a concentration of short positions just below the threshold value. The simple frequency distribution displayed in Figure 1, however, presents no apparent indications as to whether investors are avoiding publication or not.

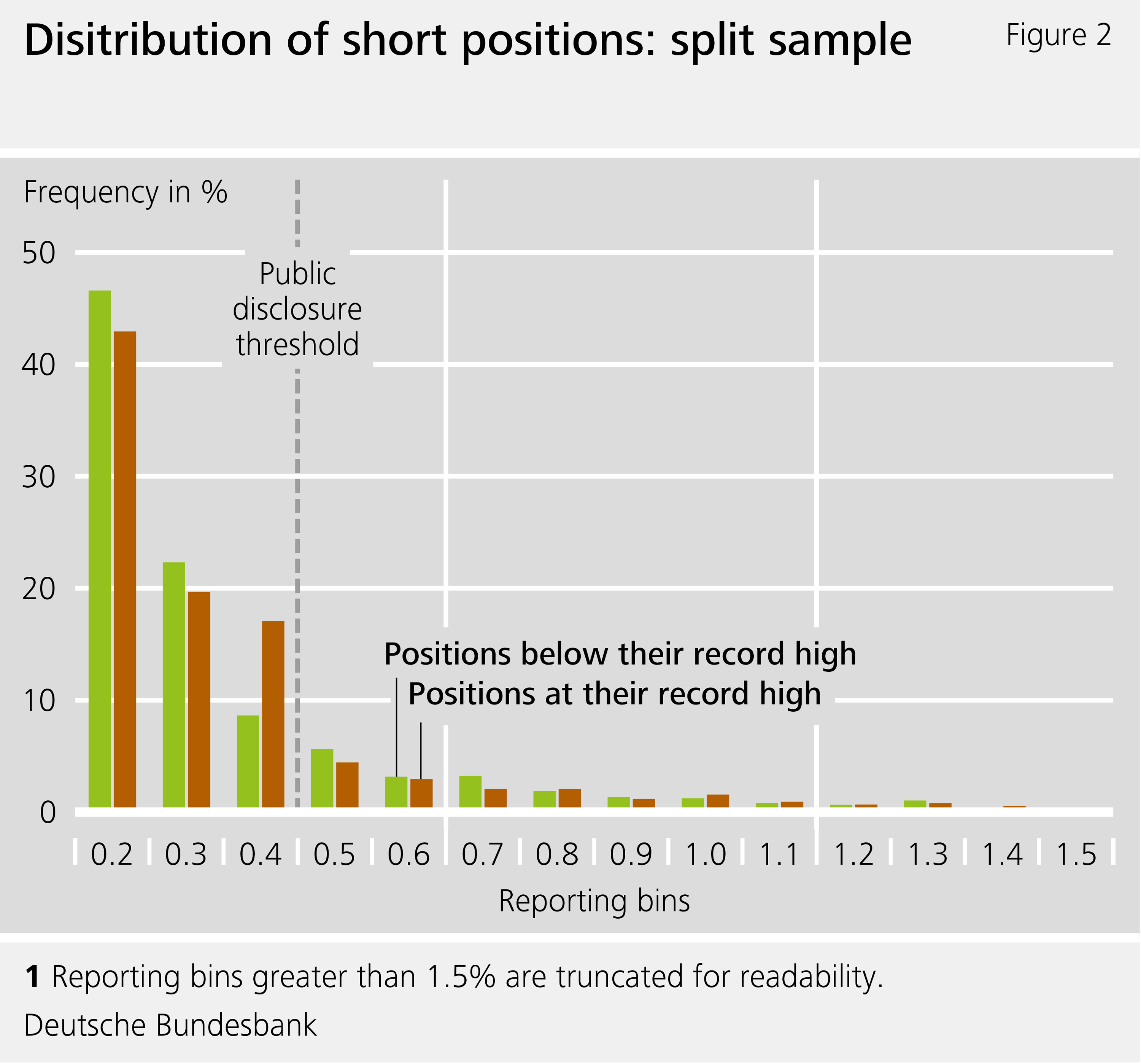

We therefore test this theory in greater detail by focusing on a subgroup of positions that are each at a record high – that is to say, the investor in question never before had a higher short position in that particular stock. This subgroup is particularly revealing for the following reason. If a position in the 0.4 interval is at its record high, this means that this position has never previously exceeded the publication threshold. These are precisely the positions where we expect to see particularly pronounced avoidance effects. By contrast, there would presumably be smaller avoidance effects for positions that have already been published in the past.

Figure 2 presents the distribution of short positions for both of these subgroups. The brown bars depict the frequency distribution of positions which are currently at their record high. A substantial concentration just below the publication threshold is discernible for this group. In the 0.4 interval, positions at their record high are roughly twice as frequent as positions which are below their record high. While this is an intentional simplification, our subsequent formal tests confirm that a significant share of investors prefers to stay out of the public eye.

Various reasons for discretion

Which factors determine the decision to publish a short position? Do specific features of the shorted stocks or investor characteristics play a role? Our analysis reveals that investors who have never disclosed short positions in the past are highly unlikely to publish positions in the future. And it is indeed the case that certain investors did not once exceed the disclosure threshold during the entire sample period, but remained just below it. This suggests that investors tend to decide whether to publish short sales not on a case-by-case basis but more as a matter of principle.

Another finding is that investors who generally avoid publication earn a superior return on their short sales than investors who do not. This indicates that short sellers who operate under the radar tend to be well-informed investors. This outcome suggests that the protection of intellectual property, such as private information on companies or newly developed investment strategies, plays an important role in this context.

Negative impact on price discovery

How does the behaviour described above affect the price discovery of stocks? The price discovery process, as it is known, represents an important mechanism in the financial market by means of which private information is incorporated into stock prices. If, say, a market participant has private information that a stock is overvalued, they can exploit this information by selling or short selling it. The sales adjust the price downwards until the stock is no longer overvalued. However, if an informed investor remains below the prescribed regulatory publication threshold, the price may take some time to adjust, thus impairing the price discovery process. In our analysis we find that negative information about a company is not directly incorporated into the stock price, precisely when a short position turns out to hide just under the publication threshold. Hence, the strategy of avoiding publication by remaining below the disclosure threshold appears to have a negative impact on the price discovery process in the stock market.

Conclusion

Our analysis shows that a considerable share of short sellers avoid disclosing their positions by remaining below the corresponding statutory threshold. Moreover, our results suggest that investors tend to decide for or against publication as a matter of principle, rather than on a case-by-case basis. Investors who stay below the radar tend to be well-informed. As a result, the efficiency of the price discovery process in the stock market is reduced.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- A Beber and M Pagano (2013), Short-selling bans around the world: evidence from the 2007-09 crisis, Journal of Finance 68(1), 343-381.

- E Boehmer, C M Jones and X Zhang (2013), Shackling short sellers: the 2008 shorting ban, Review of Financial Studies 26(6), 1363-1400.

- S Jank, C Roling and E Smajlbegovic (2016), Flying under the radar: the effects of short-sale disclosure rules on investor behavior and stock prices, Deutsche Bundesbank Discussion Paper 25/2016.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein