Is the single monetary policy producing different effects across euro-area countries? Research Brief | 13th edition – June 2017

The Eurosystem’s monetary policy is geared towards macroeconomic developments over the entire euro area. Does it produce different effects in the individual member states? And, if yes, how big are the differences? Our empirical study on interest rate policy examines this question for Germany, France, Italy and Spain, the four largest economies in the euro area.

The introduction of the euro meant that monetary policy in the member states was replaced by the Eurosystem’s single monetary policy, which is geared to economic developments over the entire euro area. One key issue is whether the impact of the single monetary policy is consistent across the member states. For example, an interest rate increase by the Eurosystem could affect economic activity and price developments in individual countries to varying degrees, implying different adjustment burdens for the member states. We are in fact able to show that, on average, prices in Germany do not fall even half as much when interest rates increase as in France, Italy or Spain.

In our study we will examine to what extent the Eurosystem’s monetary policy had a different effect on economic developments in the four large member states (Germany, France, Italy and Spain) for the period 1999 to 2014. Our analysis is confined to the impact of interest rate policy, in other words standard monetary policy measures. Our study does not take into account non-standard monetary policy, such as the Eurosystem’s current asset purchase programmes, for example.

We use a Bayesian vector autoregressive multi-country model in our analysis, which allows us to evaluate and compare the effects of monetary policy on the four economies within a single model. Furthermore, it allows for interactions among economic variables, such as gross domestic product (GDP), the price level and government bond yields across countries. In our model, we calculate the difference in the impact of monetary policy for each pair of countries and, using the statistical distribution of this difference, we can evaluate whether monetary policy produces different effects on the two countries.

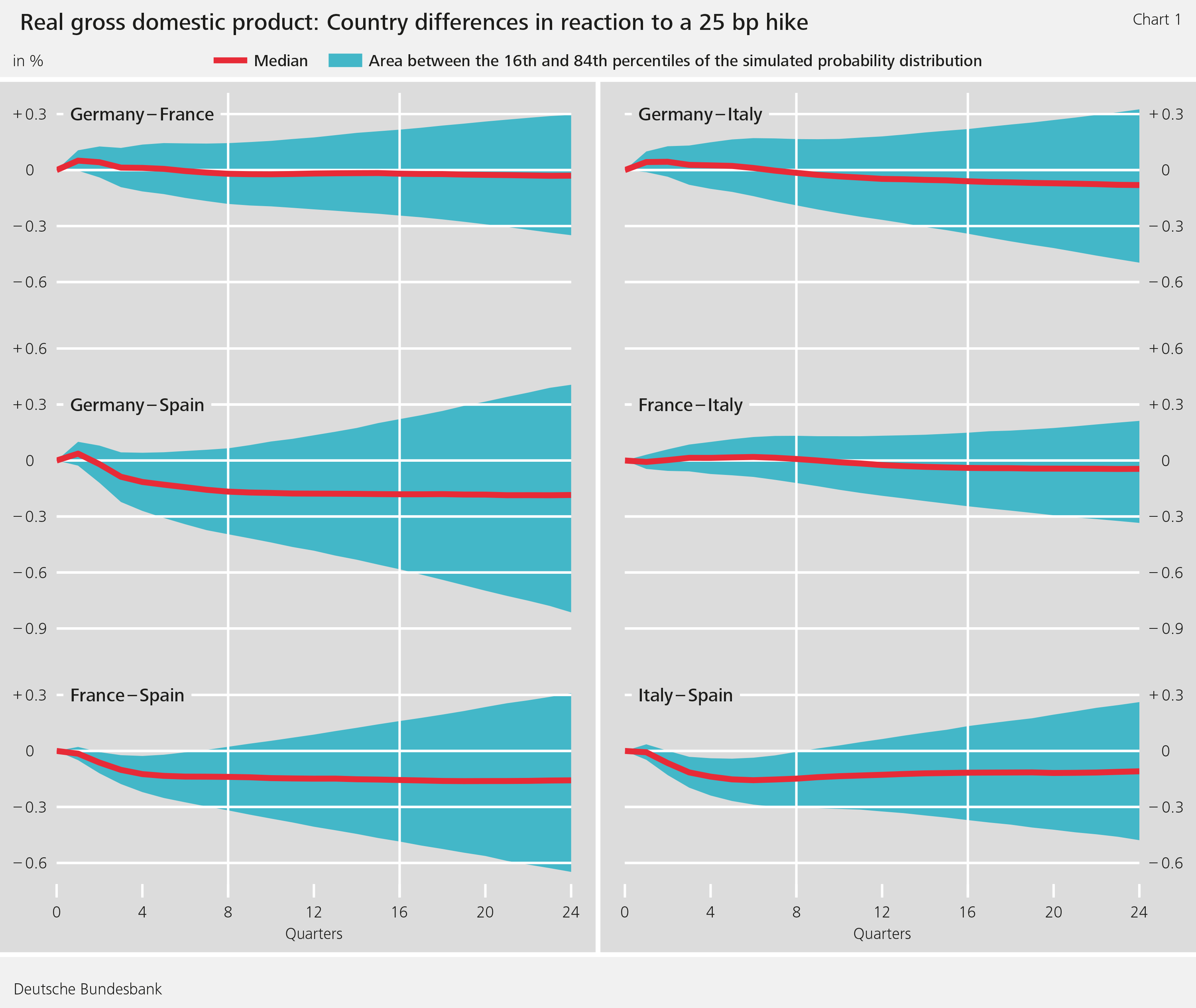

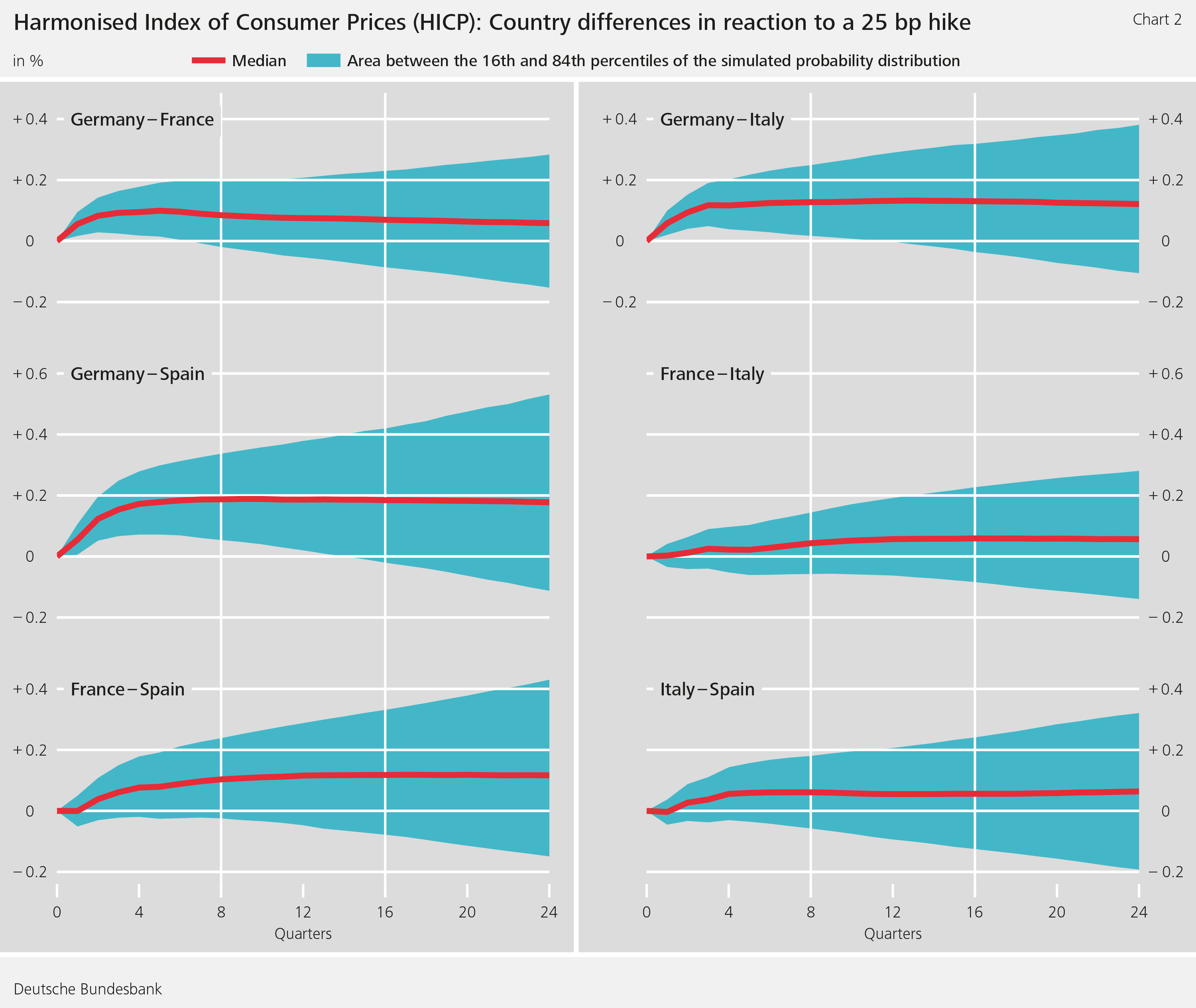

Charts 1 and 2 show, in a cross-country comparison, how a 25 bp hike affects real GDP and the Harmonised Index of Consumer Prices (HICP). The effects of an interest rate reduction of 25 bp are the same apart from the sign. Each panel shows the difference between the percentage effects of monetary policy in both of the countries represented in the chart, for the observed variable.

Chart 1 on the top left shows the effect of an interest rate increase on real GDP in Germany minus the effect on real GDP in France. The estimation method provides a probability distribution for this difference. The solid red line depicts the median of the distribution, the blue shaded area the space between the 16th and 84th percentiles.

In the above-mentioned example, negative values imply that the decline in real GDP in Germany after the interest rate rise is more pronounced than in France. Positive values, however, point to a smaller reduction in Germany than in France. From the position of the probability distribution relative to the zero line, we can conclude how strongly the reactions of the observed variables differ between the countries. For the pairwise comparisons of Germany, France and Italy, the distributions shown do not provide any evidence of pronounced differences in the effect of an interest rate increase on GDP. However, when comparing the effects in Germany, France and Italy with those in Spain, a clearly greater part of the distribution lies below zero, which shows that the reduction in GDP in the former countries is stronger than in Spain. The results are quantitatively meaningful. The median difference between Germany and Spain after six quarters is just under -0.18% and is thus only slightly smaller than the effect of the interest rate increase on real GDP in Germany and France of -0.23%. This implies that, in comparison to the other countries, real GDP in Spain reacts very weakly to interest rate changes by the Eurosystem. This result is surprising as economic developments in Spain were shaped by a property boom; one would expect interest rates changes by the central bank to have a stronger impact given the importance of mortgage loans with variable interest rates for real estate financing in Spain. Other studies arrive at a similar result (eg Cavallo and Ribba, 2015 and Georgiadis, 2015), however, and the findings remain valid in a series of robustness analyses we have conducted using modified model approaches.

For the impact of an interest rate increase on the consumer price index, Chart 2 shows that the distribution is mainly in positive territory in a comparison of the effects in Germany with all three other countries. This means that the decline in the price level in Germany is not as marked as in the other countries. The median difference between Germany and the other countries lies between 0.1% and 0.18% after six quarters. The decline in prices in Germany is thus less than half as large as in the other countries on average following an interest rate hike. When comparing France with Spain and – less clearly – Italy with Spain, the results also indicate that the decline in the consumer price index in Spain is stronger than in the former two countries. Together with the estimates for the effects of monetary policy on GDP, these results point to a flatter slope of the aggregate supply function in Germany in comparison with Spain.

The main achievement of our empirical analysis is that the methodology we use allows a statistically well-founded comparison of the effects of monetary policy on the four countries. An economic explanation of the estimated differences is not possible with the approach used, however, and must be left for future research. Possible explanationscould be differences in economic structure, labour market institutions (see Georgiadis, 2015, for example), the degree of competition in product markets and the associated scope for price setting or the fact that inflation expectations are anchored to varying degrees.

Conclusion

The results of our statistical comparisons suggest that the single monetary policy has, in some cases, different effects on the euro-area countries. This poses a challenge for the Eurosystem. The exact costs of these asymmetric effects cannot be examined within our empirical model framework and further research is needed in order to determine their size.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- A Cavallo and A Ribba (2015), Common macroeconomic shocks and business cycle fluctuations in euro area countries, International Review of Economics and Finance, 38(C), 377-392.

- G Georgiadis (2015), Examining asymmetries in the transmission of monetary policy in the euro area: Evidence from a mixed cross-section global VAR model, European Economic Review, 75, 195-215.

- M Mandler, M Scharnagl and U Volz (2016), Heterogeneity in euro-area monetary policy transmission: results from a large multi-country BVAR model, Discussion Paper No 03/2016, Deutsche Bundesbank.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein