From an individual-bank view to a system-wide view on capital requirements under crisis scenarios Research Brief | 17th edition – February 2018

How much capital is needed both at the individual bank level and for the system as a whole especially in situations of macroeconomic stress? And is the capital in the system distributed across individual banks in the optimal way to cover potential systemic losses? A new study gives answers to these questions in an integrated supervisory framework.

Since the introduction of the first Basel Accord, German banks have been required to fulfil minimum capital requirements in accordance with their risk taking behavior. This helps to reduce the risk of failing of individual banks due to negative credit shocks.

One of the lessons of the recent global financial crisis was that looking at individual banks in isolation is not sufficient. Therefore, the recent Basel III framework takes a broader view on how to safeguard the stability of the entire banking system and now complements microprudential regulation with macroprudential regulation that also takes into account systemic risk.

Shocks to individual institutions can become systemic because banks are interconnected. These interconnections arise through direct lending of funds but also through similarities in assets. Due to this indirect interconnectedness which is the focus of our study, banks become vulnerable to the same type of shocks at the same time.

The probability of a systemic event is typically low, but once it occurs it is generally associated with large system-wide losses to many or all institutions. If banks do not maintain sufficient capital by themselves these losses may eventually be borne out by taxpayers. The transposition of the Basel III framework into the EU legal framework, thus, foresees that individual banks top up their minimum capital requirements by a range of capital buffers that address systemic risk.

A joint model of micro- and macroprudential capital requirements

In our study, we propose a framework to jointly analyse micro- and macroprudential capital requirements in an integrated framework. The novelty of our approach lies in studying the macroprudential dimension by taking into account systemic risk. We call our approach M-PRESS CreditRisk (short for Micro- and MacroPrudential REquirements Systemic Stress Credit Risk).

The core of our approach is an advanced model for credit risk assessment called SystemicCreditRisk, which builds on and extends the Systemic Risk Monitor of the Oesterreichische Nationalbank (Boss et al., 2006; Elsinger et al., 2006). We argue that our credit risk model considerably reduces the scope for the possible underestimation of credit risk in the banking system.

In our credit risk model we consider the entire portfolio of German banks, which can then be aggregated to the banking system’s aggregate portfolio. For this purpose, we use information from the German credit register of loans of 1.0 million euro or more on a very detailed and disaggregated level which allows us to link single borrowers situated in a particular sector in Germany or in another country to their banks.

We measure systemic risk as the expected shortfall of the banking system. It shows the loss the banking system’s aggregate credit portfolio is expected to incur in the case of a rare crisis. We assume a one-percent probability for such an event to occur in the presence of macroeconomic stress, and only 0.1 percent in normal times.

Our portfolio model focuses on the indirect interconnectedness of banks. For example, consider a German bank that lends to borrowers in Spain. A macroeconomic shock occurring in Spain will directly increase the default probabilities in the credit portfolio of the German bank. In our model, domestic German borrowers across different sectors and foreign borrowers in different countries are all interconnected, to varying degrees. In this way the default of borrowers in Spain also indirectly raises the individual probability of default for the borrowers in particular sectors in Germany and in other countries. Therefore, the probability that borrowers will default simultaneously increases according to the individual composition of the banks’ credit portfolios. At the same time, the systemic risk in the banking system as a whole increases since different banks are interconnected through their exposures to the affected borrowers. Therefore, in our paper we concentrate on the channel of systemic risk propagation represented by correlation of bank exposures.

Policy application

Our portfolio model is integrated into a macro stress testing framework. This framework can serve as a tool to answer the following questions. How much capital is needed both at the individual bank level and for the system as a whole especially in situations of macroeconomic stress? And is the capital in the system distributed across individual banks in the optimal way to cover potential systemic losses? These questions have been the subject of a heated scientific debate for several years (Admati and Hellwig, 2013; Dagher et al., 2016).

To answer these questions, we first calculate the microprudential capital requirements for individual banks. Second, we calculate the expected shortfall for the whole banking system under normal macroeconomic conditions. We call this additional capital requirement "Pillar 2 add-on", because it represents the share of "Pillar 2" capital needed to support losses that may materialise due to changing macroeconomic conditions.

Finally, we calculate the expected shortfall for the whole banking system in situations of macroeconomic stress. This measures the macroprudential capital requirements for the system as a whole. Additionally, we can optimally distribute these system-wide macroprudential capital requirements across individual banks.

Results for twelve major German banks

We demonstrate how our macro stress testing framework could work in practice. We concentrate on the twelve major German banks that the German Federal Financial Supervisory Authority (BaFin) identified as other systemically important institutions in 2013. Systemic importance is attributed to large and interconnected banks. Among them are big banks, some Landesbanken, and other internationally active banks. We use data as of the end of 2013.

We generate three macroeconomic stress scenarios – a financial crisis, fiscal contraction and an oil price shock – with a model of the world economy. The first two scenarios consider country-specific stress with hypothetical shocks hitting the economies of Greece, Italy, Portugal and Spain, while the third scenario is a global shock that affects all countries. We translate the macroeconomic shocks into probabilities of default via the satellite multi-country macroeconometric model, which are fed into the portfolio model.

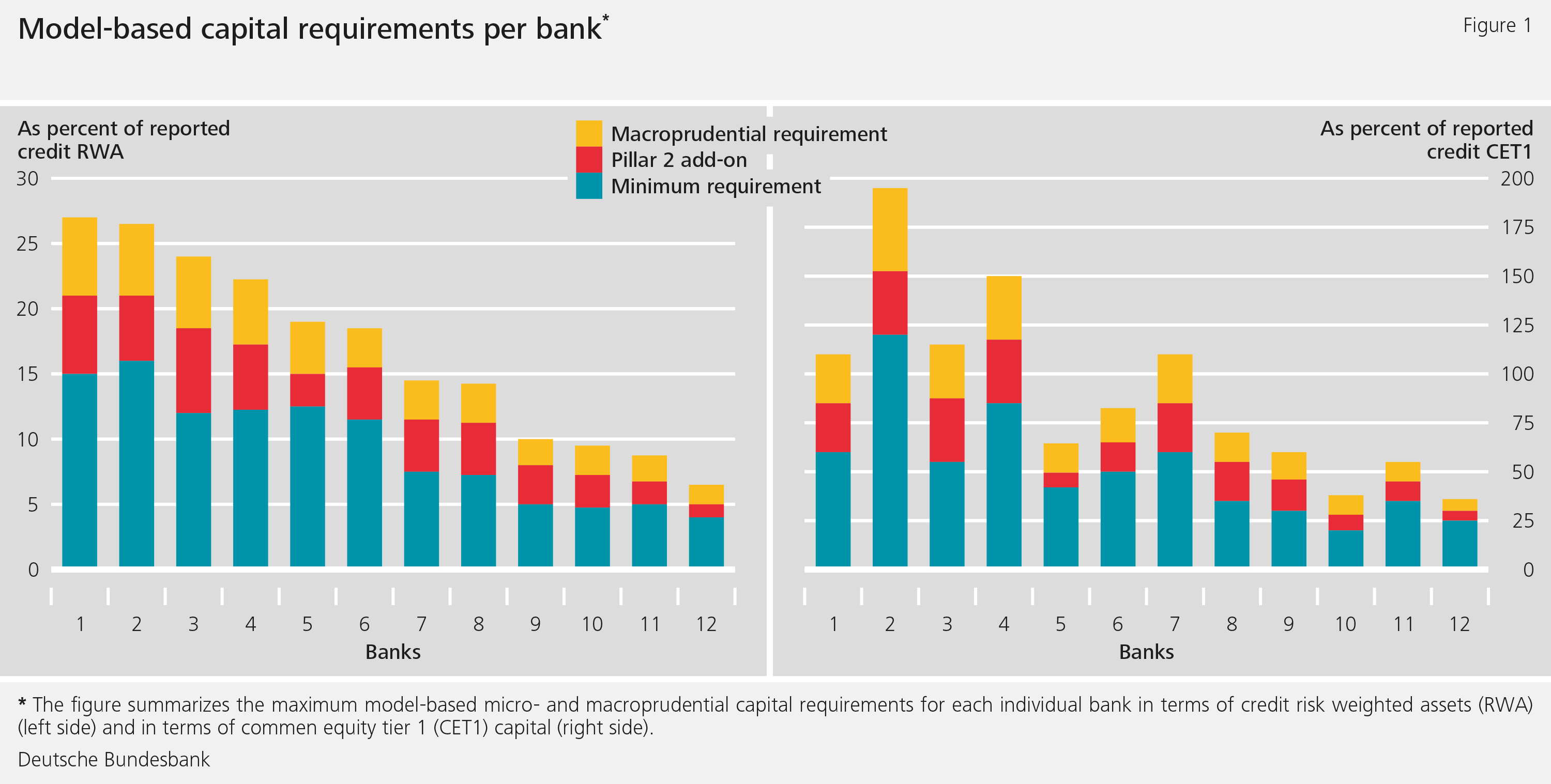

Our results suggest that there was enough capital in the system as a whole to withstand the adverse macroeconomic developments. In our three stress scenarios, the system's expected shortfall never exceeds 18% of the reported credit risk weighted assets or 88% of the available common equity tier 1 capital requirements.

Nevertheless, the bank level results shown in Figure 1 prompt the conclusion that capital allocation among the banks is not necessarily optimal from the systemic point of view. In the worst of our three scenarios, the left-hand panel shows that the combined micro- and macroprudential capital requirements calibrated to the model range from 6.3% to 27.2% of the reported credit risk weighted assets. The right-hand panel shows that for banks 1,2,3,4 and 7 these requirements would exceed their reported tier 1 common equity capital (CET 1).

Conclusion

Wrapping up, M-PRESS-CreditRisk develops a sophisticated portfolio model that captures a significant part of systemic credit risk. This tool can help supervisors to calibrate different micro- and macroprudential capital requirements in one holistic supervisory framework.

Needless to say, due to model uncertainty our numerical results should be treated with caution. One caveat is that we concentrate on the systemic risk that arises through the indirect interconnectedness of banks’ credit portfolios, and disregard other channels of systemic risk propagation such as contagion. Nevertheless, we think that our approach represents an important step forward in designing capital requirements in a way that takes a systemic view into account.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Admati, A. and M. Hellwig (2013). The bankers' new clothes: What's wrong with banking and what to do about it. Princenton University Press.

- Boss, M., G. Krenn, C. Puhr, and M. Summer (2006). Systemic risk monitor: A model for systemic risk analysis and stress testing of banking systems. Financial Stability Report 11, Oesterreichische Nationalbank.

- Dagher, J., G. Dell'Ariccia, L. Laeven, L. Ratnovski, and H. Tong (2016). Benefits and costs of bank capital. IMF Staff Discussion Note SDB/16/04, International Monetary Fund.

- Elsinger, H., A. Lehar, and M. Summer (2006). Risk assessment for banking systems. Management Science 52 (9), 1301-1314.

- Tente, N., N. von Westernhagen, and U. Slopek (2017). M-PRESS-CreditRisk: A holistic micro- and macroprudential approach to capital requirements. Discussion Paper 15/2017, Deutsche Bundesbank.A. Admati und M. Hellwig, Des Bankers neue Kleider: Was bei Banken wirklich schief läuft und was sich ändern muss, FinanzBuch Verlag, 2013.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein