A costly Brexit? De-liberalisation of trade in services and its potential cost Research Brief | 23rd edition – December 2018

In many areas, the ramifications of Brexit are not yet clear. It is likely, however, that the United Kingdom’s departure from the European Union will lead to a de-liberalisation of trade in services. A new study examines what this change could mean for individual EU Member States.

When it comes to trade in goods and services, the European Union (EU) is the United Kingdom’s most important partner. By the same token, the United Kingdom is also an important trading partner for the EU. The United Kingdom’s departure from the EU means that new market access arrangements need to be agreed between the two parties. These changes are likely to come with a hefty price tag for both sides. If we want to quantify these costs, though, it is not enough to simply look at goods transactions and traditional trade barriers such as customs tariffs to provide a quantitative picture of the possible repercussions of Brexit. Both the United Kingdom and individual EU Member States rank among the world’s most important exporters of services, which is why, in a new study, we investigate – among other issues – the potential costs of a de-liberalisation of trade in services.

Due to the existence of the Single Market, trade in services within the EU is largely free of barriers between Member States. An array of more recent preferential trade agreements also serve to ease market access conditions on a mutual basis. Thus trade agreements, like those laid down between Member States in the EU treaties, and the arrangements that the EU has struck with third countries go far beyond trade liberalisation in the traditional sense of relief from customs duties.

The economic consequences of the preferential liberalisation of trade in services are far reaching. This is because services play a particularly important role in domestic and transnational value chains, and the production of goods is growing ever more complex. Not only do cross-border service barriers implicitly raise the prices charged by the affected service providers both at home and abroad, but they also make for higher price tags for goods on account of input costs.

Data on trade in goods and services

Data on trade in goods, aggregated to varying degrees (e.g. country pairings, products and country pairings, firms and products as well as destination countries), are readily available; data on trade in services, meanwhile, are hard to come by – especially broken down by sector. The World Input-Output Database (WIOD, see Timmer et al., 2015) provides goods and services linkages for sectors and country pairings covering the period from 2000 to 2014. These data illustrate the significance of individual service inputs not only for other service sectors but also in terms of manufacturing. The interlinkages depicted in the WIOD cover 43 countries.

In addition to the WIOD, we also use the Statistics on International Trade in Services (SITS) collected by the Bundesbank (see Biewen and Lohner, 2017). These are extremely useful for our analysis, partly because of the size of Germany’s economy but also because of the detailed breakdown by service type that they provide. The data enable us to form a granular picture of the relationship in the German economy between services trade metrics and firm characteristics.

A model for trade in services

We construct a model for trade in services so as to analyse international interlinkages in trade in services and enable us to quantify outcomes of a potential de-liberalisation. Newer models of international trade (for example Chaney, 2008) generally rest on two assumptions. First, that destination markets differ in terms of the fixed costs of serving that market. Second, that firms differ in terms of their productivity – and thus their economic activity and size. In particular, it is assumed that firm productivity follows the same Pareto distribution across all sectors and destination markets. This would imply a disproportionately large number of small businesses with low productivity, while highly productive and – by extension – large firms are uncommon. Most existing models also assume that all consumers (both households and firms) in the destination country are equally accessible.

The SITS data on Germany’s services trade paint a different picture. The ratio of small to large firms varies significantly across the destination markets for Germany’s service exports and cannot be adequately described by a conventional Pareto distribution. There are, in fact, significantly more smaller exporters of services than we would expect to see if firm sizes were truly Pareto-distributed. Extremely successful and large firms, meanwhile, are infrequent to varying degrees in different destination markets.

We therefore apply a model which describes these characteristics better than conventional trade models. Consistent with the granular data, our model assumes that not all consumers in a market are equally reachable. Furthermore, service providers exhibit market-specific variation as regards productivity.

Aided by our model, we can thus determine (1) market-specific productivity distribution at the sectoral level, (2) the profit margins of specific sectors and (3) market penetration, that is to say the reachability of consumers in the specific destination market. Furthermore, we can use the WIOD data to decompose the general costs of serving a market into political cost factors (such as membership of trade agreements relating to services) and natural determinants (for instance geographical or linguistic barriers). All in all, our model is a highly effective reflection of the economic world mapped out in the WIOD.

Costs for the United Kingdom not inconsiderable

Our services trade model is well suited to simulating the potential costs of services trade de-liberalisation.

Our study considers multiple scenarios; here, for the purposes of illustration, we cover just one, positing an end only to preferential market access for services between the United Kingdom and all other EU countries, which – up until now – has been ensured by the EU treaties. This scenario represents a hard Brexit for the services industry but without the imposition of restrictions on goods and capital.

On the basis of data for 2014, our simulation shows a services Brexit alone resulting in a 0.33% drop in real consumption in the United Kingdom. These economic costs would stem from the United Kingdom’s service-related trade barriers with the EU being raised to a level equalling that already in place for third countries such as the United States. Real wages and real dividends in service sectors would see falls of a similar order, averaging 0.38% and 0.32% respectively. In the manufacturing sector, real wages and real dividends would fall by just under 0.1% on account of input-output relationships and adjustments in input markets alone. Of course, it is not only the United Kingdom which would encounter additional costs. It can be assumed, however, that, due to their market size, the relative costs for larger trading partners – in this case the entire rest of the EU – would be less than for smaller parties – here the United Kingdom.

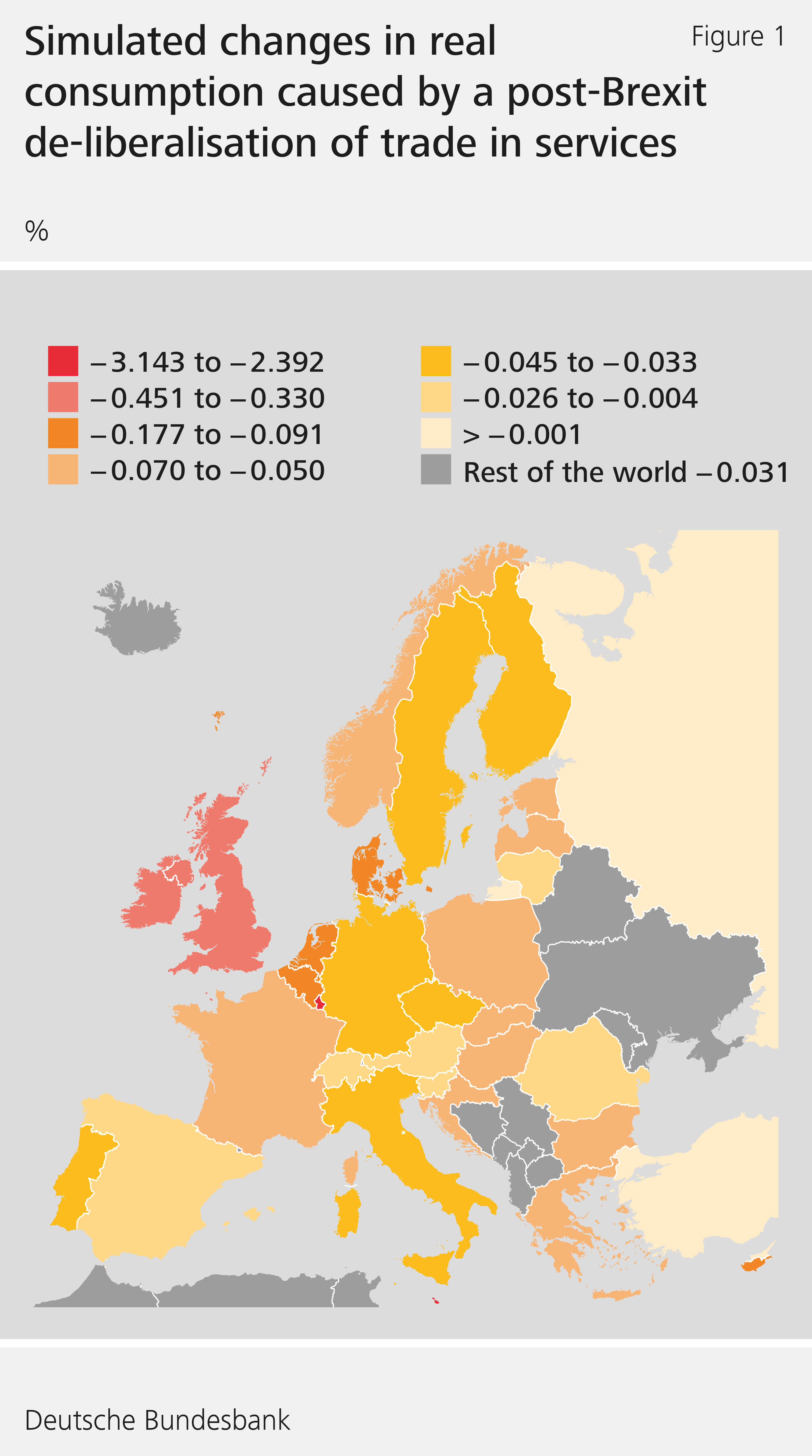

Figure 1 shows how real per capita consumption would change in different European countries under this scenario. Countries such as Germany and France would also see declines in real consumption, albeit modest at 0.03% and 0.06% respectively. In smaller countries, such as Luxembourg, the drop in real consumption would be more pronounced, at 2.4%, however. These results clearly show that the costs of Brexit stemming just from the de-liberalisation of trade in services could also be hugely significant for individual countries.

In the event of a hard Brexit, the changes described would represent just a fraction of the total costs. De-liberalisation of the free movement of goods, capital and people would also ensue. These changes have been explicitly excluded here due to the focus on services.

Conclusion

Our study analyses liberalisation and de-liberalisation measures for cross-border trade in services. The behaviour of firms and households was described using a variety of input, including detailed information on cross-border activities of firms in Germany, one of the world’s largest exporters of services. Employing the quantitative model, we simulated the effects of services trade de-liberalisation brought about by Brexit. The results show that increased barriers for trade in services alone would suffice to drive real consumption down significantly in some countries.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Biewen, E., and S. Lohner (2017), Statistics on international trade in services – Data Report 2017-07 – Metadata Version 1, Research Data and Service Centre, Deutsche Bundesbank.

- Blank, S., P. Egger, V. Merlo, and G. Wamser (2018), A Structural Quantitative Analysis of Services Trade De-liberalization, Deutsche Bundesbank Discussion Paper 47/2018.

- Chaney, T. (2008), Distorted Gravity: The Intensive and Extensive Margins of International Trade, American Economic Review, 98(4), 1707-1721.

- Timmer, M. P., E. Dietzenbacher, B. Los, R. Stehrer, and G. J. de Vries (2015), An Illustrated User Guide to the World Input-Output Database: the Case of Global Automotive Production, Review of International Economics, 23(3), 575-605.

| The authors | |

| Sven Blank Research economist at the Deutsche Bundesbank’s Research Centre | Peter H. Egger Professor of Applied Economics at ETH Zurich |

| Valeria Merlo Professor of International Economics at the University of Tübingen | Georg Wamser Professor of Economics at the University of Tübingen |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein