Why ECB announcements move markets Research Brief | 26th edition – June 2019

Whenever financial markets react to ECB Governing Council meetings, the explanation seems obvious: the Governing Council surprised markets, for instance, by changing its policy rate or by hinting at a future rate change. Any market reaction would thus stem from unexpected announcements about monetary policy. The response of different asset prices such as bond yields and stock prices, however, often contradicts this simple explanation. A new study indicates that these seemingly puzzling reactions are driven by information about the economic outlook that the ECB reveals via its announcements.

The immediate reaction of yields is often used to judge whether a central bank conducts expansionary or contractionary monetary policy. Announcements that lower yields, for instance, are regarded as a policy loosening. Such a loosening should be accompanied by rising stock prices, since it raises expectations about future dividends and lowers the interest rate at which these dividends are discounted. In actual fact, however, stock prices often decline alongside yields. Why?

Central bank information channel

A potential explanation for these seemingly contradictory market reactions is the so-called “central bank information channel”, which refers to new information about the economic outlook that the central bank reveals via its announcements. During ECB press conferences, for instance, the ECB President explicitly discusses the current and expected economic situation in the euro area. If this assessment is surprisingly negative, market participants might revise their growth expectations downwards. Both yields and stock prices would decline in this case.

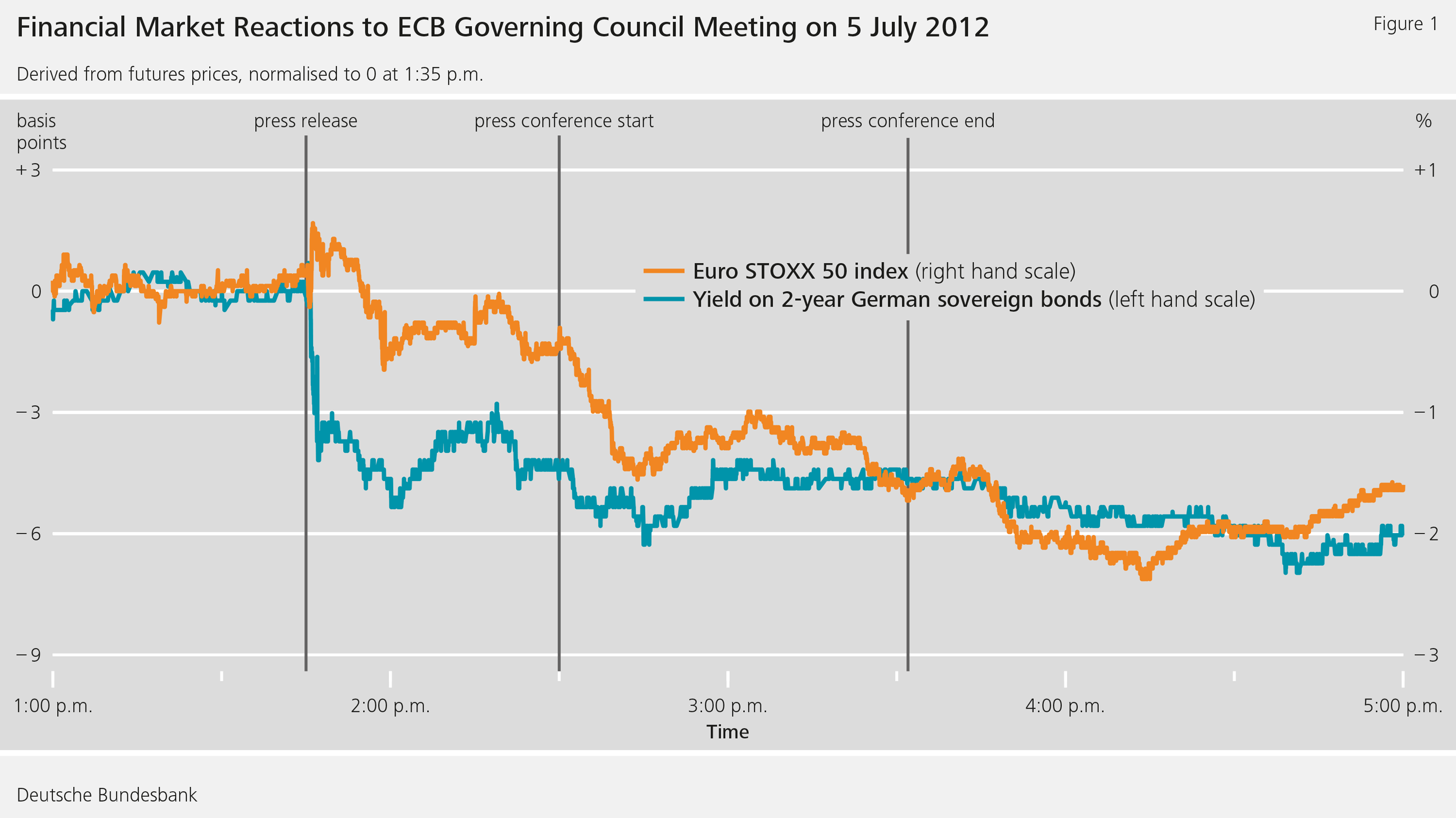

Figure 1 illustrates these considerations by way of example. On 5 July 2012, the ECB Governing Council decided to lower its policy rates by 25 basis points. The decision was announced via a press release at 1:45 p.m. and led to an immediate decline in bond yields, suggesting that the decision was not entirely anticipated by market participants. According to the standard view, the rate cut was thus an expansionary policy surprise, which should have raised stock prices. But in actual fact, stock prices declined by about 2 percent. The bulk of the decline occurred between 2:30 and 3:32 p.m., i.e. during the press conference, in which ECB President Mario Draghi declared that downside risks had materialised and that the euro area growth outlook would therefore remain weak. It seems likely that the simultaneous drop in yields and stock prices was driven by these pessimistic statements about the economic outlook – and not by announcements about monetary policy.

In a recent discussion paper (Kerssenfischer, 2019) I study the relevance of these non-monetary announcements by looking at market reactions on all 186 ECB Governing Council meeting days between March 2002 and December 2018. As a naive measure of monetary policy shocks, I use changes in the 2-year German bond yield around ECB announcements. This naïve measure corresponds to the above-mentioned view that any yield movement is exclusively driven by news about monetary policy.

To isolate news about the economic outlook from news about policy, I instead use changes in both yields and stock prices and assume the following relation (see Jarocinski and Karadi, 2018): a monetary loosening should lower yields and raise stock prices, whereas unfavourable news about the economic outlook should lower yields alongside stock prices. In this way, I obtain two further measures: one for pure monetary policy shocks and one for non-monetary news, the so-called central bank information shocks.

Yield movements not driven solely by monetary policy

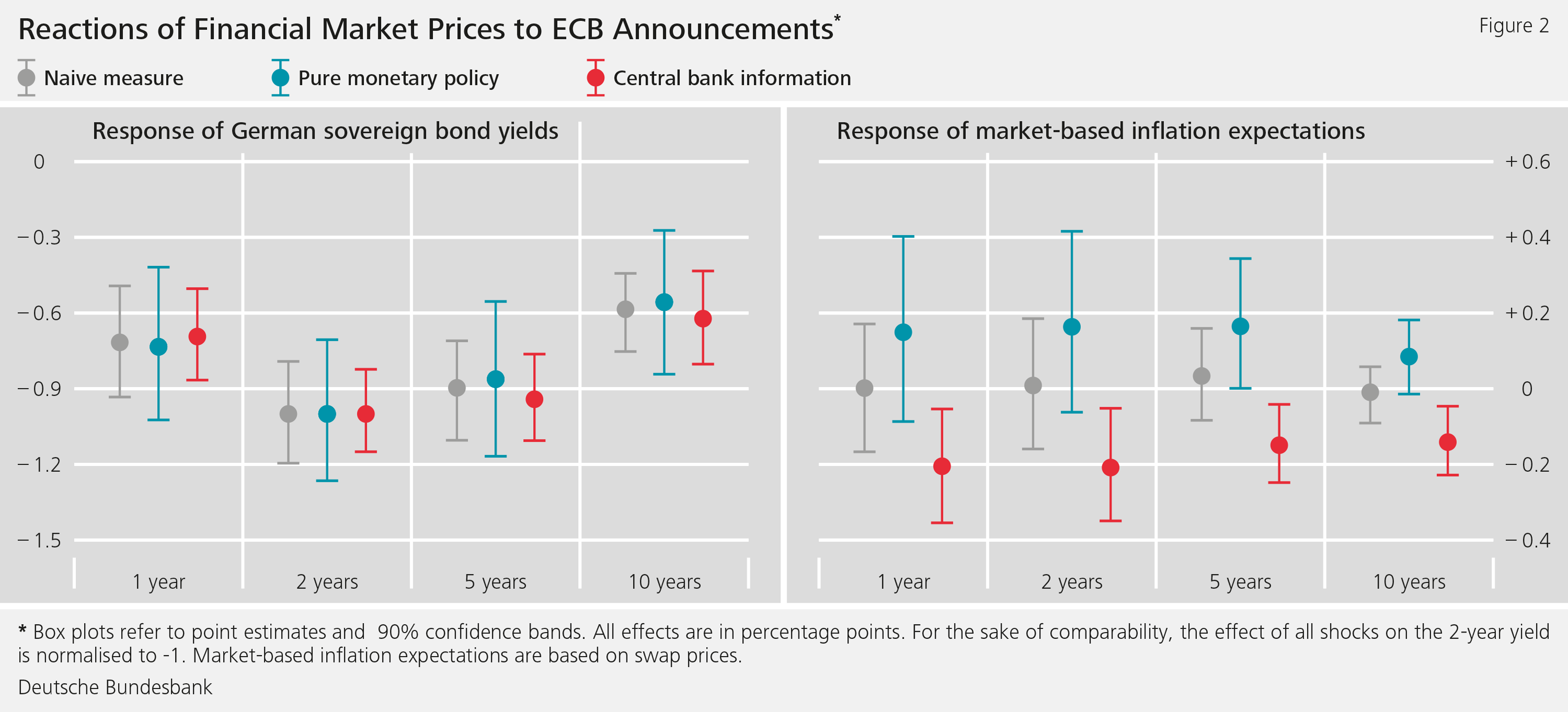

Figure 2 shows the effect each of the three shock measures has on nominal bond yields and market-based inflation expectations. The naïve shock lowers yields, particularly at the 2-year maturity, but it has hardly any effect on inflation expectations. This is at odds with the standard view, according to which a monetary loosening should raise short-term inflation expectations. The response of yields to ECB announcements, in other words, does not seem to be driven solely by news about monetary policy.

Differentiating between the two components of ECB announcements, in contrast, delivers intuitive results. When yields decline because of an expansionary policy shock, expected inflation rises. When yields decline because the ECB’s economic outlook is worse than expected, market participants lower their inflation expectations.

Importantly, the response of yields alone is not informative about the root cause of the market reaction. Both expansionary policy and unfavourable information about the economy have similar effects along the yield curve.

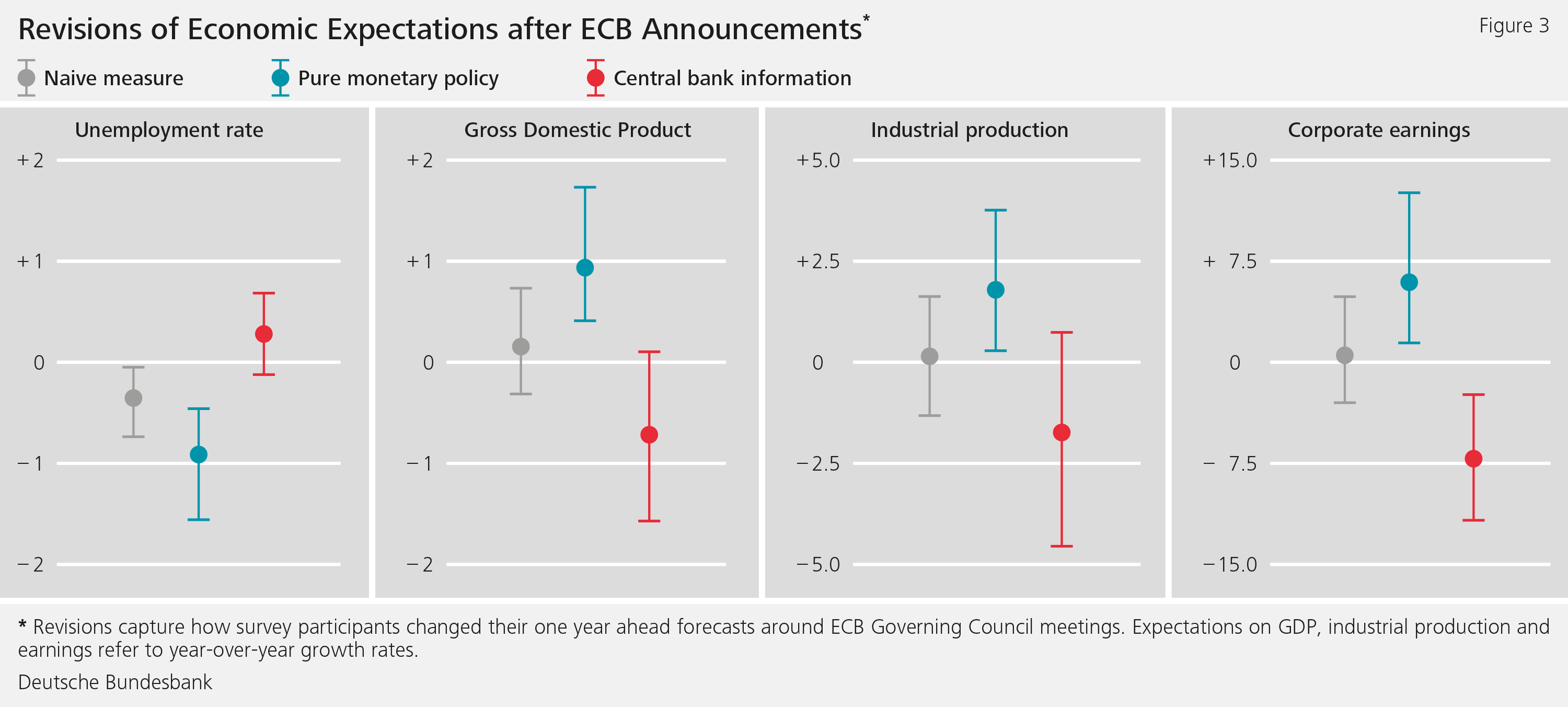

Surveys allow an even more direct assessment of how market participants revise their economic expectations in response to ECB announcements. Figure 3 shows that the naïve shock measure marginally reduces the expected unemployment rate, but otherwise barely affects economic expectations. The pure policy shocks, on the other hand, have strong effects across the board. Growth and earnings expectations, for instance, rise after an unexpected policy loosening and expected unemployment declines. In contrast, when yields decline because the ECB reveals unfavourable news about its economic outlook, market participants revise their expectations down.

Conclusion

Market movements around ECB announcements are usually attributed entirely to monetary policy. My study instead suggests that markets react not only to news about monetary policy but also to news about the economic outlook that the ECB reveals via its announcements. This non-monetary news can trigger revisions in market participants’ growth expectations and thus help explain the otherwise at times puzzling market reactions to ECB announcements.

Disclaimer |

The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Jarocinski, M. and Karadi, P. (2018), Deconstructing monetary policy surprises: the role of information shocks, ECB Working Paper 2133.

- Kerssenfischer, M. (2019), Information effects of euro area monetary policy: New evidence from high-frequency futures data, Deutsche Bundesbank Discussion Paper No 07/2019.

The author |

|

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein