Reasons for the low homeownership rate in Germany Research Brief | 30th edition – January 2020

Germany has the second lowest share of homeowners of all OECD countries. This is driven by housing policies that produce incentives to rent. New studies show that alternative policies could increase the homeownership rate and reduce wealth inequality.

In many countries, governments intervene in housing markets to create incentives for homeownership. However, still little is known about the effectiveness of such policies and their consequences for welfare and inequality. In a new study (Kaas, Kocharkov, Preugschat and Siassi, forthcoming), we focus on the case of Germany where only about 45 percent of households own their main residence. This is the second lowest number among all OECD countries, undercut only by Switzerland.

To better understand why homeownership is so low in Germany, we analyse the role of housing policies that differ in particular ways from those in other countries. Germany has high transfer taxes on buying real estate, no mortgage interest tax deductions for owner-occupiers, and a social housing sector with broad eligibility requirements. All these features potentially tilt incentives towards renting. Higher transaction taxes make real estate a more expensive and less liquid asset. The lack of mortgage tax deductions is tax-efficient but raises financing costs, and social housing rentals provide a low-cost alternative to homeownership.

The impact of housing policies

To gauge whether these policies matter for homeownership, we build a quantitative equilibrium model that in addition to housing policies includes other key factors for the homeownership decision of a household: uncertainty of earnings over the life cycle, house price, and rent risk as well as borrowing constraints. Moreover, we take into account that housing supply is not fully elastic and adjusts imperfectly to changes in demand.

We do not take into account aggregate house price risk, mortgage defaults, mortgage tax deductions on owned residential properties that are rented out or the potential dependence of homeownership preferences on historical events such as World War II. Long-term effects of homeownership on children’s education and health are not taken into consideration either. See, for example, Huber and Schmidt (2019) for a study on the relationship between culture and homeownership.

After estimating the model for Germany, we implement three policy experiments that mimic selected policies in the United States where the homeownership rate stands at about 65 percent. We analyse both the new long-run equilibria as well as the adjustment dynamics. In all experiments, we take into account that the government adjusts income taxes to balance the budget and to account for expenditure changes through the new housing policy measures. House prices and rents adjust to changes in housing demand, too. However, we do not account for any further effects such as house price changes affecting financial stability.

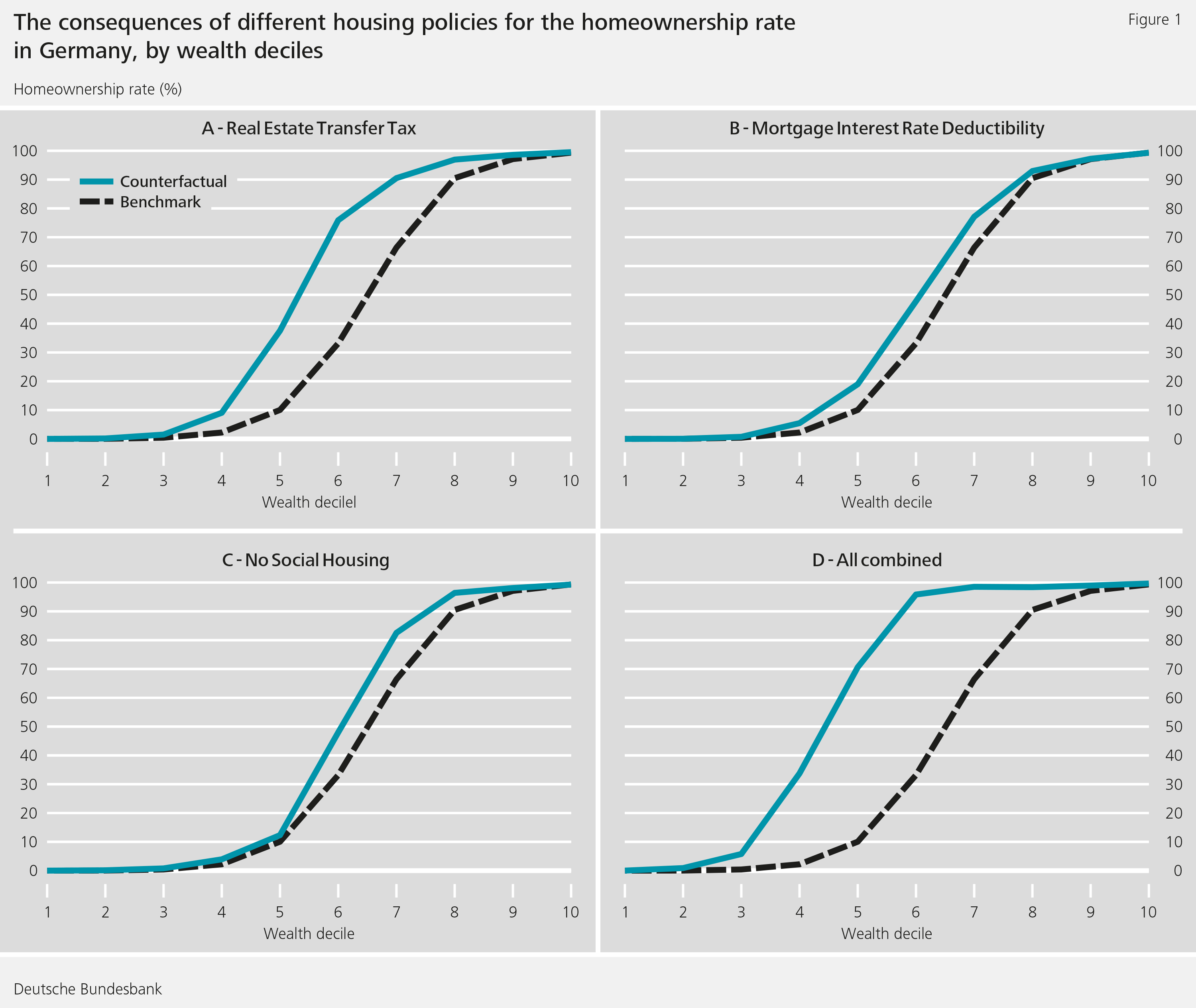

In our first experiment, we consider a reduction of the real-estate transfer tax (RETT) from its current average level of 5 percent in Germany to the average level of 0.33 percent in the U.S. Second, we make mortgage interest payments tax-deductible for owner-occupiers. Finally, we consider eliminating the subsidy on social housing and reduce income taxes for everybody with the saved amount.

Figure 1 depicts the impact of these experiments on the homeownership rate as a function of household net wealth. The first wealth decile corresponds to the poorest 10 percent of the population, the second to the next 10 percent, and so on. It shows that in the initial situation (black line), the homeownership rate among the poorest 30 percent in our model is zero, since all of these households are renters. By contrast, the homeownership rate for the richest 30 percent in the model is over 90 percent. In the data, this is very similar: almost all households in the top three deciles are homeowners, and almost all households in the bottom three deciles are tenants.

As can be seen from Figure 1, each policy experiment (blue line) has significant positive effects on the homeownership rate. The changes are mainly noticeable in the middle deciles of household wealth distribution; these are the households that make up the middle class in terms of wealth. The combined effect, shown in the bottom right graph, leads to a counterfactual homeownership rate of 58 percent.

Housing policy reforms generate heterogeneous welfare effects

Different housing policies would give more households an incentive to become homeowners. However, these policies would have distributional effects, too. For instance, tenants and homeowners would be affected differently. Then, would such policy changes increase welfare for society as a whole? As the reforms affect households differently, we measure welfare as the average benefit for all households in the model.

The reduction of transaction taxes lowers welfare by about the same amount as a decline in household consumption of 0.5 percent, or about 128 euros per year. The explanation is that this policy raises both house prices and rents. With lower transaction taxes, the house price (including ancillary costs) that owner-occupiers have to pay decreases, but the house price without tax, which real-estate companies pay as landlords in our model, increases and rents also rise. Thus, especially those households that remain renters after the policy change are affected negatively. In addition, the reform has redistributive effects. Low-income households, which are less likely to benefit from lower transaction taxes, need to pay higher income taxes to compensate for the government’s revenue losses.

On the other hand, the introduction of mortgage interest tax deductions for owner-occupiers brings about small welfare gains as it allows more households in the lower income deciles to own a home. Although this measure also leads to slightly higher prices and rents, the overall effect on welfare remains slightly positive.

If social housing is eliminated and income taxes are lowered as a consequence, we see significant welfare gains in our model. In principle, social housing offers cheap and stable rents. However, since there are relatively few social housing units, it is accessible only to a minority of eligible households. All others need to find a home in the private market where supply is low because part of the housing stock – social housing – is not available. Therefore, abolishing social housing while reducing income taxes will lead to welfare gains comparable to an increase in household consumption of around 78 euros per year. If social policy is further extended through an additional monetary housing subsidy for low-income households, the welfare gains increase to about 230 euros per year. The reason for this is that households value the additional insurance aspect of housing benefits, as is the case with other social security benefits.

Housing policy reforms could reduce wealth inequality

The policy changes that we discuss not only prompt a portfolio reallocation from financial assets towards real estate but also lead to an overall increase of total net wealth by more than 11 percent. This is because more households are willing and able to build up savings to overcome the down-payment requirements and to reap the benefits of homeownership. As can be seen from Figure 1, these are mostly households in the middle deciles of the wealth distribution.

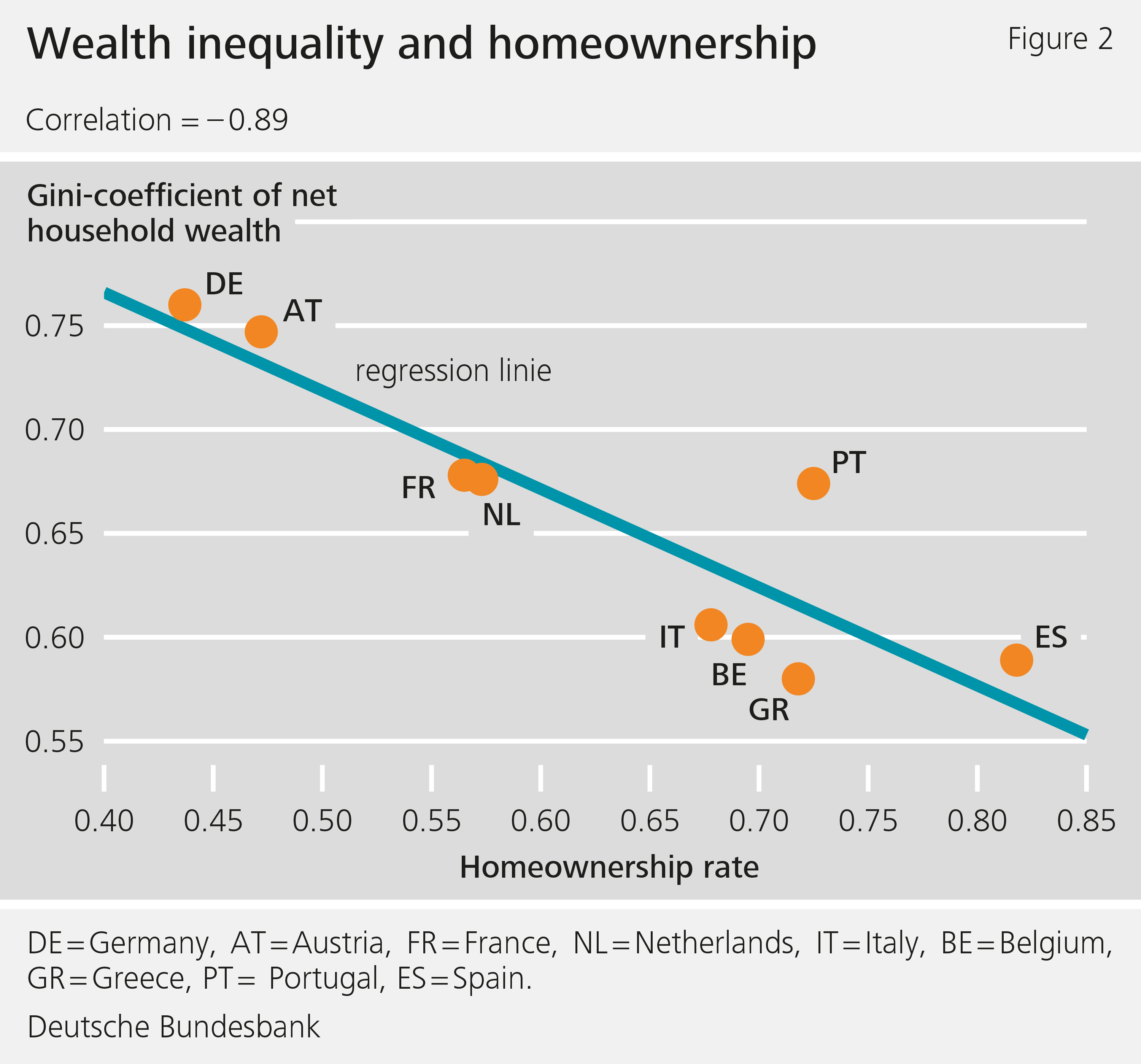

Therefore, housing policy, as well as other features of the social insurance system, have implications for the wealth distribution of the economy. Indeed, in another study (Kaas, Kocharkov and Preugschat, forthcoming), we document that there is a tight connection between homeownership rates and wealth inequality across European countries. Those countries with a low homeownership rate (such as Austria or Germany) also have the highest net wealth inequality (see Figure 2). The dominant factor behind this relationship is the average wealth difference between homeowners and renters, which is much lower in Southern European countries with higher homeownership rates.

Conclusion

Housing policy typically has a number of concrete goals. It also has welfare and distributive consequences. Our analysis shows that housing policy can significantly affect the homeownership rate and thus, indirectly, wealth inequality.

We show that a significant part of the low homeownership rate in Germany relative to other countries can be explained by the relatively high real-estate transfer tax, the absence of mortgage interest payments tax-deductibility for owner-occupiers and the existence of a social housing sector.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Huber, Stefanie, Schmidt, Tobias: Cross-country differences in homeownership: A cultural phenomenon, Deutsche Bundesbank Discussion Paper 40/2019.

- Kaas, Leo, Kocharkov, Georgi, Preugschat, Edgar, and Siassi, Nawid: Low homeownership in Germany – a quantitative exploration, forthcoming in the Journal of the European Economic Association.

- Kaas, Leo, Kocharkov, Georgi, Preugschat, Edgar: Wealth inequality and homeownership in Europe, forthcoming in the Annals of Economics and Statistics.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein