Higher wages in Germany do not materially reduce trade imbalances Research Brief | 32nd edition – March 2020

Can wage hikes in Germany contribute to a reduction in global trade imbalances? A new study answers this question. Applying a general equilibrium model, it shows that, although wage hikes in Germany reduce the country’s trade surplus, the quantitative effects are relatively small and depend on the European Central Bank’s monetary policy response.

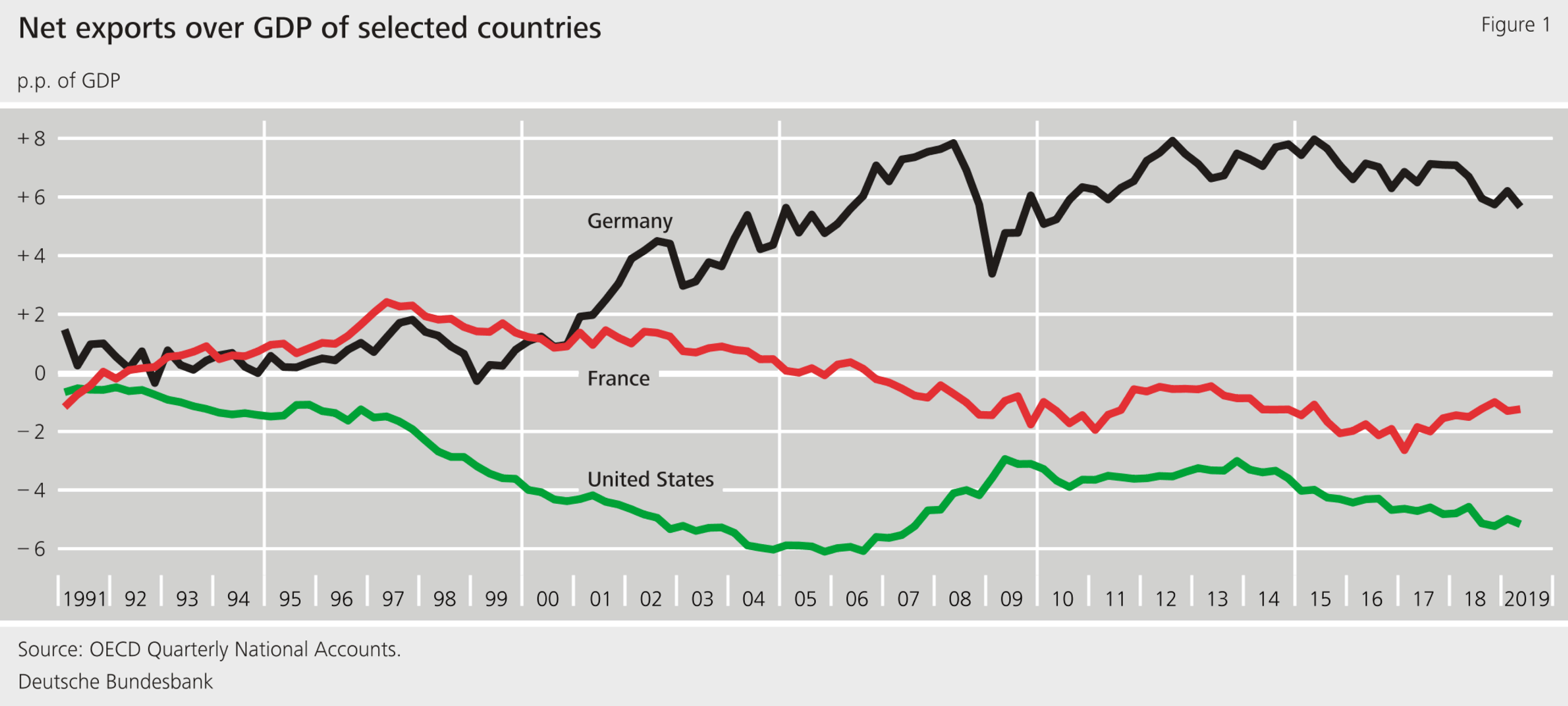

Germany has been running considerable export surpluses for years, and net exports last year came to 6% of gross domestic product (GDP). Other countries such as, for instance, France have seen their trade balances flip back and forth between positive and negative territory for a long time or, like the United States, have been running sustained deficits (see Figure 1).

Surpluses and deficits are not inherently bad. Fast-growing countries generally report high investment ratios. They therefore import more and borrow from surplus countries in order to cover the attendant deficit. Trade balances are the key driver of the current account balance; therefore, if they become excessively large, they pose risks not only for the country’s macroeconomic stability but to the global economy as a whole. According to the International Monetary Fund (IMF, 2018), measured in terms of medium-term trends and a “desirable” policy, between 35% and 45% of global surpluses and deficits are currently deemed excessive. In the IMF’s estimation, this also includes Germany’s current account surplus.

In the economic policy debate, proposals have been put forward to reduce Germany’s trade surplus and thus contribute in part to global rebalancing (see also European Commission, 2013; IMF, 2013; European Central Bank, 2019). In that vein, the IMF (2019) argues that a relative acceleration in German wage growth and the attendant changes in international goods prices could cause international price competitiveness and, hence, the trade balance to adjust.

Analysis for Germany within the euro area and within the group of its other main trading partners

In a new study (Hoffmann et al., 2020), we examine the claim that international trade imbalances can be reduced by higher wages. In order to analyse the effects of a wage hike in Germany on international trade flows and the path of inflation and GDP, we develop and estimate a general equilibrium model which reflects Germany and its trading partners within and outside the euro area. Our multi-country model contains exogenous shocks. Those shocks impact on consumer preferences, technology and policy variables, such as the central bank policy rate or tax revenue, and can thus alter supply and demand conditions on the labour, goods and financial markets over time. We model a higher rate of wage growth in Germany via a temporary exogenous wage mark-up. Examples of such exogenous changes to wages include gains in unions’ bargaining power but also other wage-setting factors which are not modelled explicitly. We estimate the importance of these and other supply and demand-side shocks for the 1995 to 2017 period. This allows us to analyse the role of wage growth in Germany’s trade balance (defined as net exports over GDP) over the past two decades and examine how a wage hike in Germany impacts on international trade balances (see also Bettendorf and León-Ledesma, 2019).

Impact of wages on Germany’s trade balance from a historical perspective

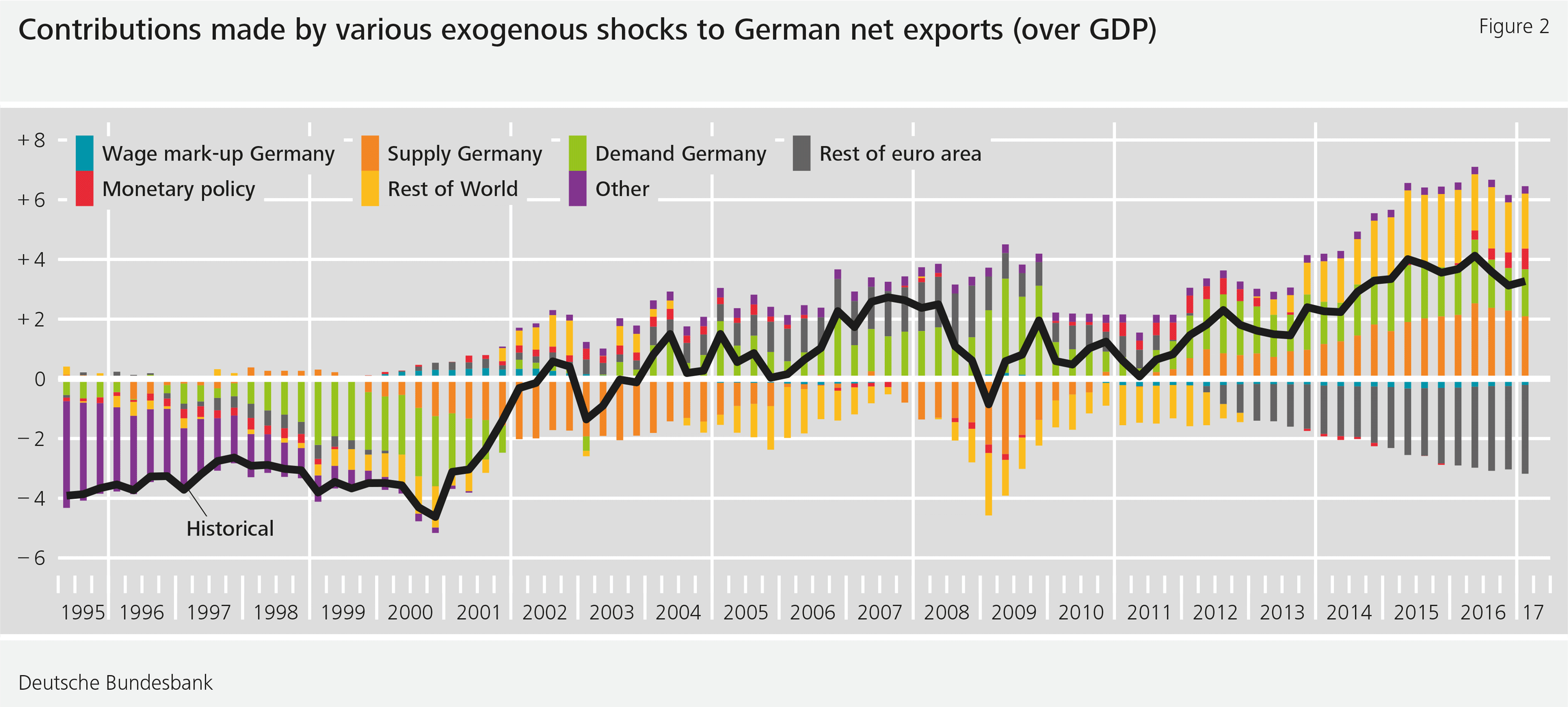

Our analysis shows that, over the past two decades, unexpected wage hikes in Germany have made only a marginal contribution to a change in the trade balance. Figure 2 illustrates this development over time: the black line shows Germany’s trade balance (in deviation from its mean). The variously coloured bars illustrate the various contributions made by (international) demand and supply shocks, unexpected changes in Eurosystem monetary policy and wage shocks to the trade balance.

Figure 2 shows that, looking at German net exports over the past 20 years, domestic and foreign supply and demand shocks were key determinants of the trade balance. The contribution to Germany’s trade balance by domestic wage shocks has gained in importance in the past few years but is comparatively small (see also Deutsche Bundesbank, 2019).

Impact of a wage hike hinges on the monetary policy stance

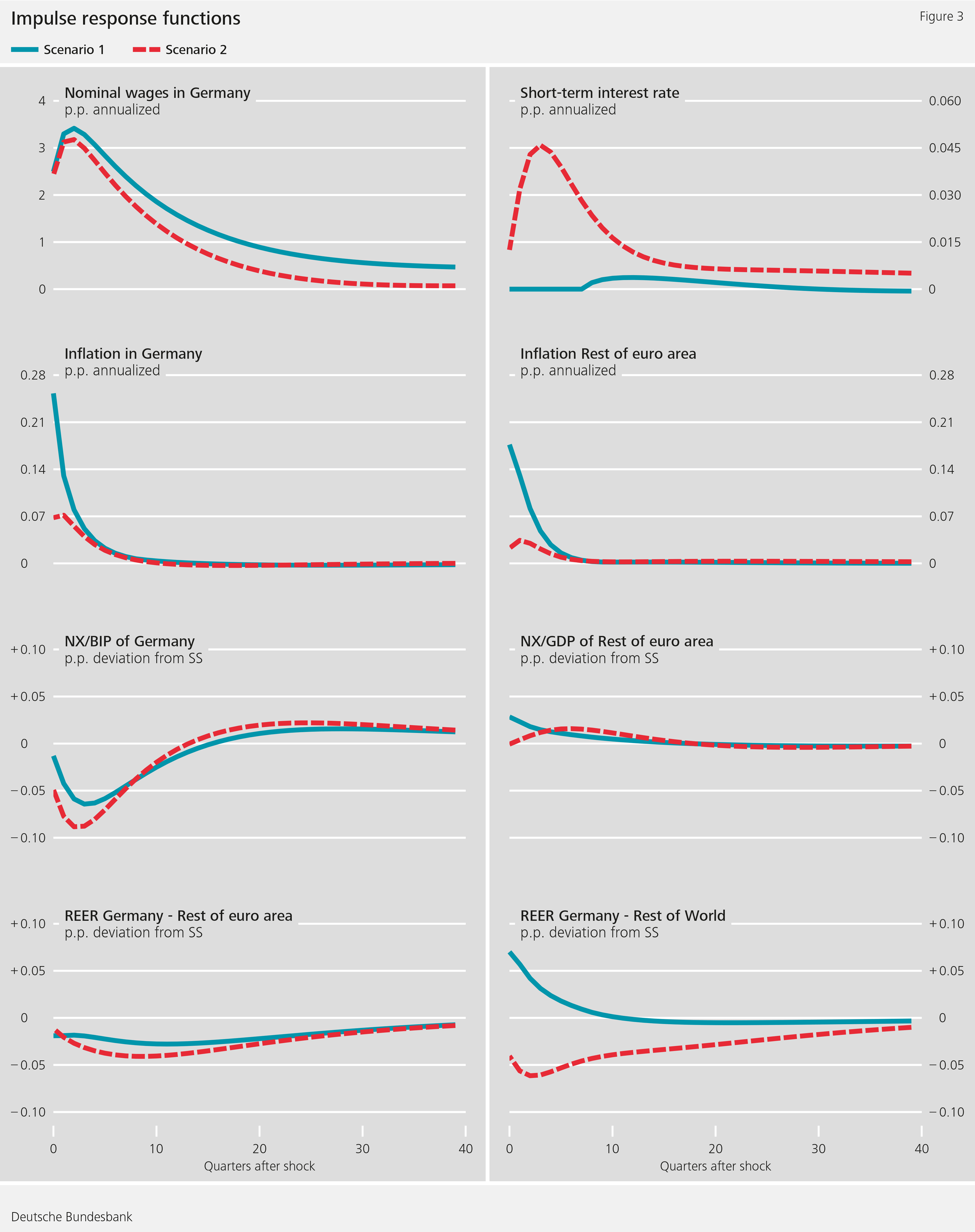

The historically smaller importance of wage shocks for Germany’s trade balance does not mean, however, that a wage hike in Germany cannot make a contribution to offsetting international trade imbalances. Our study incorporates the stance of monetary policy in the euro area as a key aspect. We focus on the impact of higher wages in Germany in an environment in which interest rates have remained unchanged over a period of eight quarters (scenario 1 in Figure 3). This we compare with a counterfactual situation in which an immediate monetary policy response in the euro area is possible (see scenario 2 in Figure 3).

Following an unexpected wage hike in Germany, Germany’s trade balance (NX/GDP) deteriorates, whereas the rest of the euro area sees trade surpluses. Specifically, the unexpected wage hike increases German firms’ labour costs, which is associated with heightened price pressure and thus higher inflation. If the European Central Bank responds to the wage hike in Germany by increasing interest rates (scenario 2 in Figure 3), the higher inflation is associated with an appreciation of Germany’s real exchange rate against its euro area and non-euro area trading partners. This makes foreign goods more competitive, enabling international trade flows to be adjusted.

The direct impact on Germany’s overall trade balance is weaker, if European monetary policymakers respond to the higher inflation not by increasing interest rates but by keeping the policy rate constant (scenario 1). Because the real exchange rate against non-euro area trading partners would depreciate, such an accommodative European monetary policy would lead to a relatively smaller decline in trade surpluses for Germany and the euro area as a whole.

Conclusion

Our study shows that wage hikes in Germany can cause international trade imbalances to adjust. The strength of this effect depends, however, on the monetary policy stance in the euro area. Even if the Eurosystem did not respond to higher wage pressure in Germany by raising interest rates, the impact on the adjustment of the international trade balance would not be great. In short, higher wages in Germany are not a very effective instrument with which to counteract global imbalances.

Disclaimer |

The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Bettendorf, T. and M. León-Ledesma (2019): „German wage moderation and European imbalances: Feeding the global VAR with theory,“ Journal of Money, Credit and Banking, Vol. 51(2-3), pp. 617-653.

- Deutsche Bundesbank (2019): Monatsbericht, März 2019.

- Europäische Zentralbank (2019): „20 years of European Economic and Monetary Union,” Conference proceedings, 17-19 June 2019, Sintra, Portugal.

- Europäische Kommission (2013): „Macroeconomic Imbalances - Germany 2014,” European Economy occasional paper no.174, European Commission.

- Hoffmann, M., M. Kliem, M.U. Krause, S. Moyen und R. Sauer (2020): „Rebalancing the Euro Area: Is Wage Adjustment in Germany the Answer?,“ Bundesbank Discussion Paper 17/2020.

- IWF (2013): „Germany: 2013 Article IV Consultation,“ IMF Country Report No. 13/255, International Monetary Fund.

- IWF (2018): „External Sector Report: Tackling Global Imbalances amid Rising Trade Tensions,” International Monetary Fund.

- IWF (2019): „External Sector Report: The Dynamics of External Adjustment,” International Monetary Fund.

The authors | ||

| Mathias Hoffmann Research Economist, Research Centre, Deutsche Bundesbank | Martin Kliem Research Economist, Research Centre, Deutsche Bundesbank | Stephane Moyen Research Economist, Research Centre, Deutsche Bundesbank |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein