Households’ Expectations and Unintended Consequences of Policy Announcements Research Brief | 34th edition – November 2020

Announcements of policy actions may influence households’ expectations about future individual and aggregate economic outcomes. We show that households have lowered their expectations with regard to the economic situation and that uncertainty about the economy increased during the initial stage of the COVID-19 pandemic. We also show that households who received information on stabilizing monetary and fiscal policy measures, surprisingly, become more pessimistic concerning their future income and GDP growth.

Stabilization policies are designed to help the economy get back on track after downturns. A carefully designed communication strategy might be important, too, as there is no clear understanding so far about whether and how households respond to policy announcements. In this research brief, we study the effects of several policy announcements on households’ expectations at the start of the COVID-19 pandemic-related recession using the new Bundesbank household expectations survey (BOP-HH).

The BOP-HH survey is conducted as a monthly online panel and is designed to inform policymakers about German households’ economic situation and sentiment as well as individuals’ expectations of future personal and economic conditions. Specifically, the survey asks respondents about their household income, labour market status and other basic sociodemographic characteristics. Expectations about future GDP growth, inflation, asset prices and personal income growth are elicited through a series of questions about the distribution and the average realization of these future variables. The structure of the survey also allows adding questions on contemporary topics in each monthly wave. For a detailed description of the survey project, see Beckmann and Schmidt (2020).

With this survey, the Deutsche Bundesbank also aims to achieve a better understanding of the effects of monetary and fiscal policy measures on households’ expectations. In this spirit, we implemented a survey experiment in April 2020, which has enabled us to study the responses of households to the announcements of several different public policies at the onset of the current recession.

COVID-19 induces disagreement, pessimism and uncertainty about future outcomes

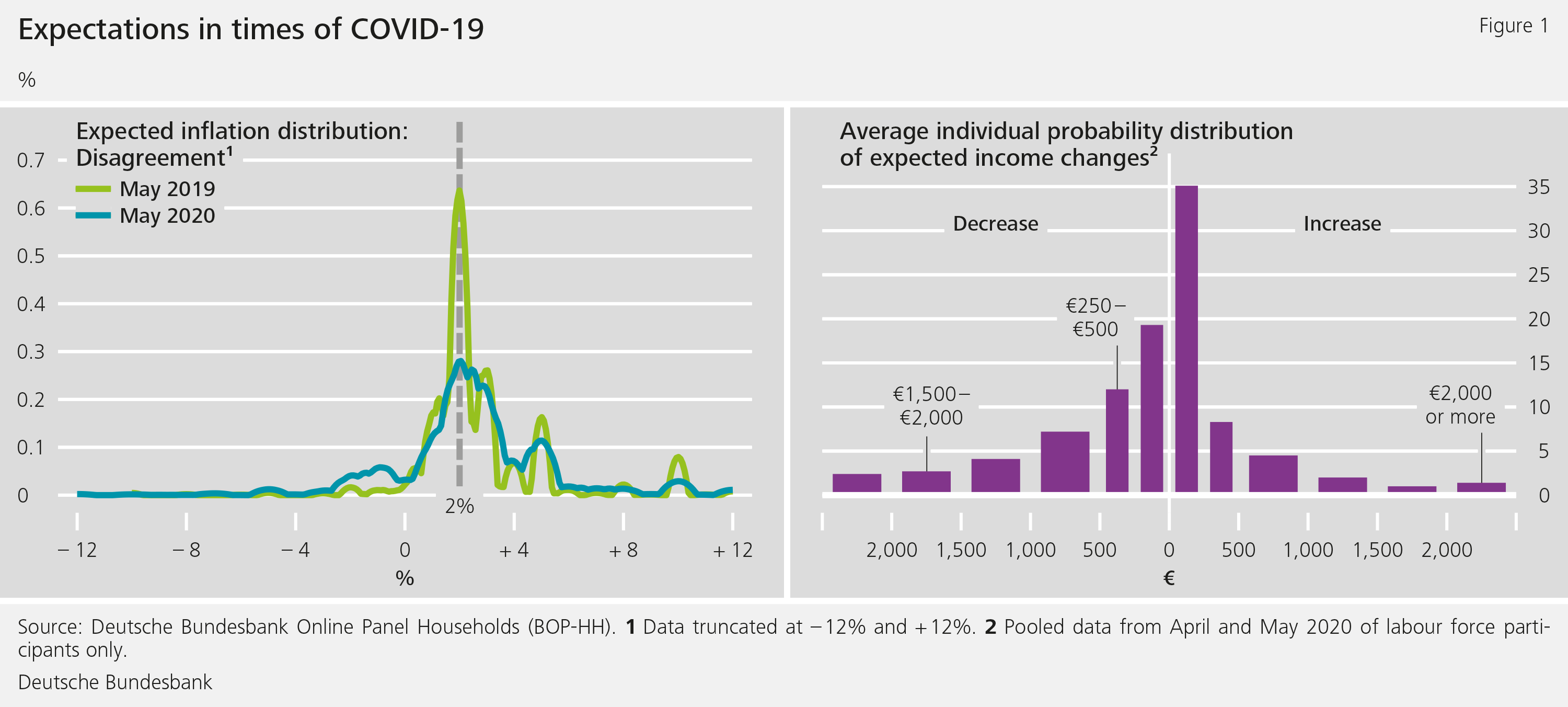

In Figure 1a, we compare the distribution of households’ expected inflation rates in May 2020 to the same distribution one year earlier. Even though there is hardly any change in average expected inflation, the differences in individual forecasts increase markedly. Not only are there more households expecting high inflation over the next 12 months, there are also more households expecting low or even negative inflation rates. This means that there has been widening disagreement between households about future inflation.

We also document that households are pessimistic about their own earnings. On average, employed participants expect their net income to fall by €115 per month over the next year. However, the average masks economically significant differences. Figure 1b shows that 19.3% expect their income to decline by less than €250, 12% expect it to decline by between €250 and €500, and 9.2% expect an even larger decline.

Expansionary policy announcements make households more pessimistic

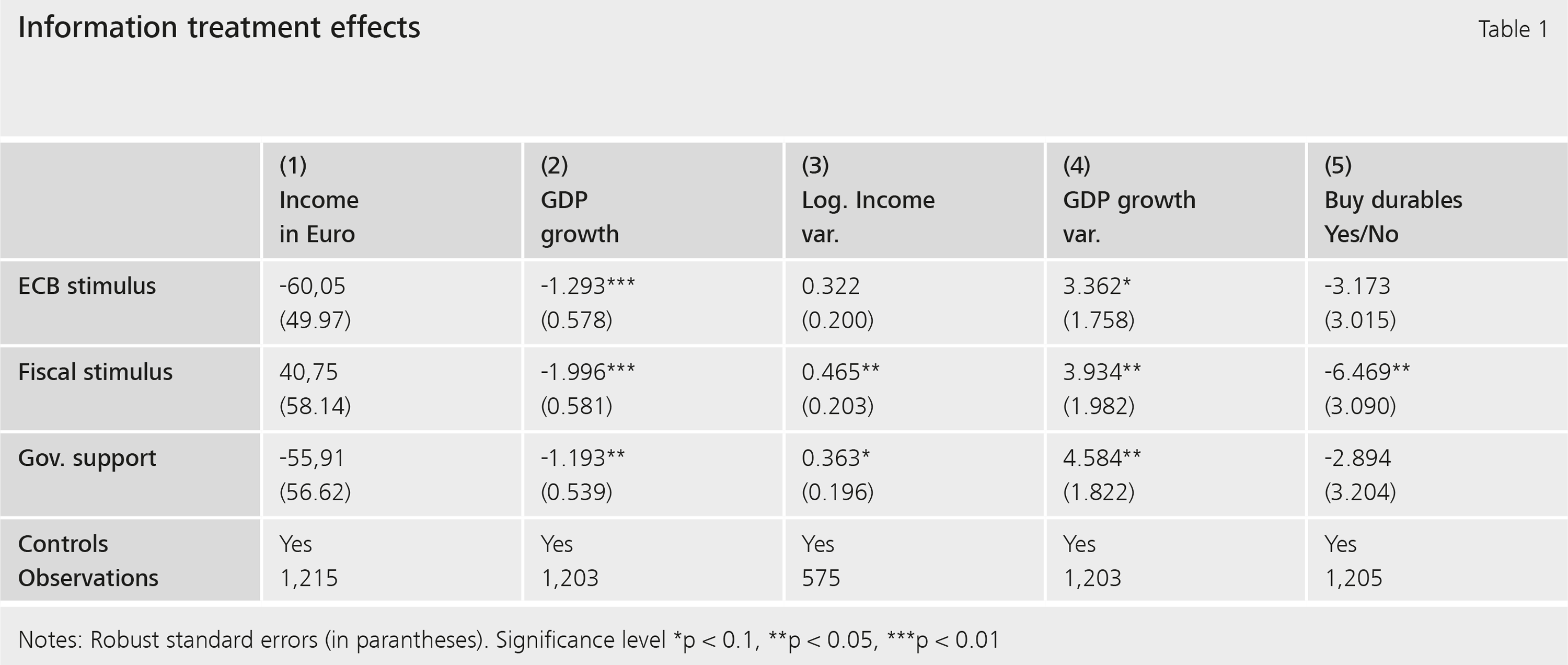

To see how individuals’ expectations respond to policy announcements geared to mitigating the economic fallout from the pandemic, we randomly divided the respondents into four groups. The first group was given economically irrelevant information about an EU action plan on human rights and democracy. This is

known as a placebo treatment. Participants in the other three groups were provided with an abridged version of the actual announcements regarding recent policy measures. Row 1 of Table 1 shows the results for the announcement by the European Central Bank (ECB) about buying bonds worth up to €750 billion. Row 2 shows the results for the announcement by the German Federal Government about the launch of a €750 billion aid package for employees, the self-employed and firms. Row 3 shows the results for the announcement by the economic affairs minister of the German federal government concerning the measures taken to counter the economic effects of the pandemic. The numbers in the columns of the table present the estimated treatment effects of the policy announcements with respect to a particular variable. Put simply, the numbers report how survey participants changed their views on the economic outcomes after receiving information on different policy actions to combat the crisis relative to those individuals who received only the placebo treatment. This setting allows us to study how various policies causally affect individuals’ outlooks.

Since the three policy measures are expansionary, they all should lead households to become more optimistic about the future. However, the experiment provides no conclusive evidence that any of the policy announcements has had significant effects on expectations about income (Column 1). Moreover, individuals who receive information about policy measures provide lower estimates of future GDP growth (Column 2). Thus, even though all three measures are designed to stimulate GDP, households who receive information about them become more pessimistic than the households who do not receive the relevant information. For example, those who were told about the fiscal stimulus (Row 2) expect GDP to grow by almost 2 percentage points less over the next year than those who were given the placebo treatment.

Moreover, households’ uncertainty also increases following receipt of information on the policy measures. We measure uncertainty by asking individuals about the probability that GDP (or the household’s future net income) will increase or decrease by a given amount. The less certain households are, the more dispersed their answers will be. We find that, for households who were told about one of the stimulus measures, there is an increase both in uncertainty about their expected income (Column 3) and in uncertainty about future GDP growth (Column 4). Column 5 shows that these negative effects on households’ assessment of the future lead them, in the case of the fiscal stimulus treatment (Row 2), to significantly lower their propensity to purchase large durable goods.

What explains these surprising effects?

One explanation could be that households were already informed about policy measures before the experiment. In the survey, we have an indication of how knowledgeable respondents are about various economic policies, and we do not observe a difference in response to the treatments in the experiment between knowledgeable and less knowledgeable individuals. Another possibility is that households do not fully understand the implications of the policy measures. However, we see the same effects following even the most simplified of the policy announcements.

Finally, it might be the case that policy announcements reveal information about the economy being in a weaker state than households believed it to be. In other words, households might think that if the ECB or the federal government announces such a policy, the situation must be worse than they had thought. This is sometimes referred to as “signalling effect” or “information effect” (see Melosi, 2017, Nakamura and Steinsson, 2018, Kerssenfischer, 2019). While we cannot provide definitive evidence that our results are driven by signalling effects, they are consistent with such a narrative. Coibion et al. (2020) find similar results in a recent survey of US households.

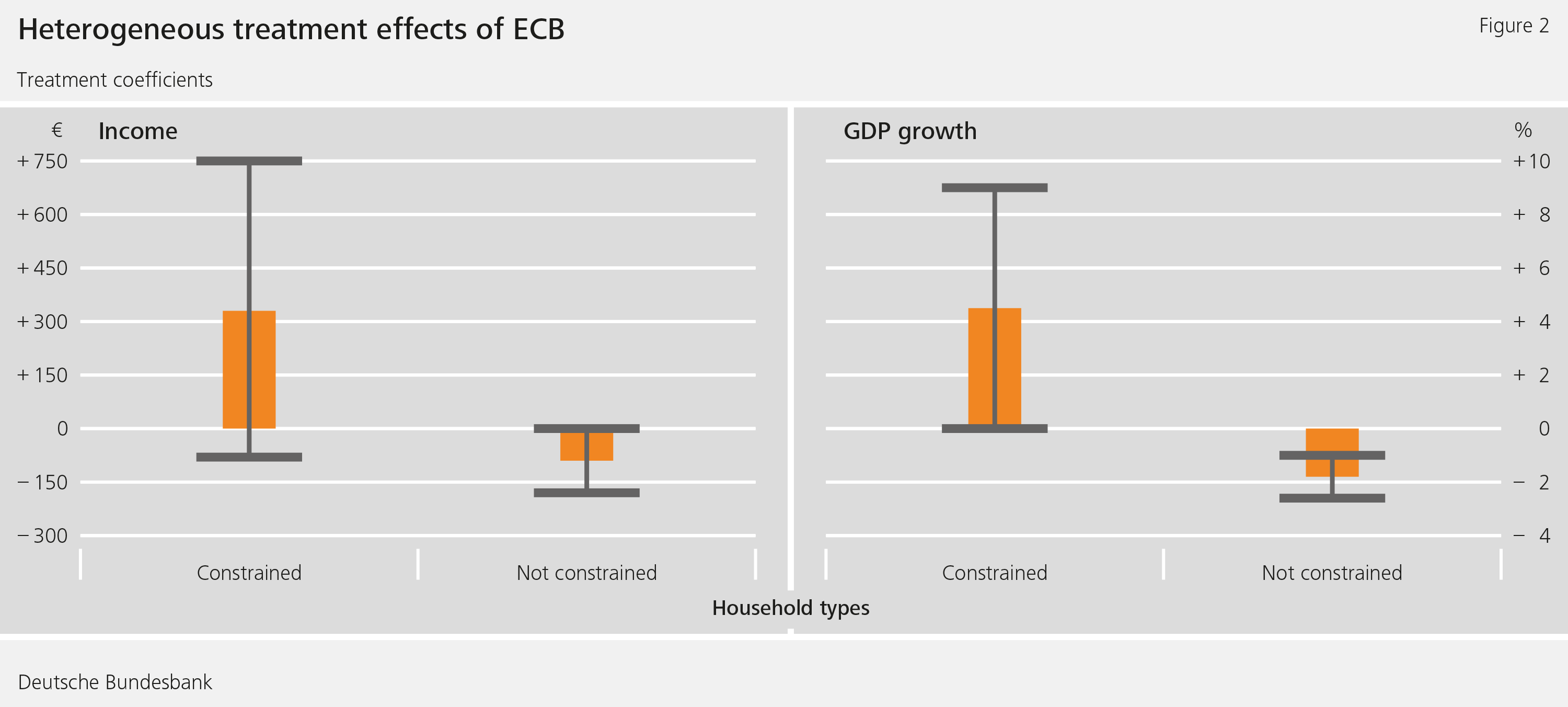

We further investigate differences in households’ response to the policy announcements. Considering credit-constrained vs. credit-unconstrained households, as measured by the self-assessed ability to obtain credit, we find that the constrained households become more optimistic about their future income and expected GDP growth. On the other hand, unconstrained households become more pessimistic about these outcomes.

In Figure 2, we show, as an example, the effects of the ECB policy announcement. Credit-constrained households, which have received information about the ECB economic stimulus, expect their future income to be, on average, €330 higher than their uninformed counterparts; see the left-hand panel of Figure 2 where the vertical line indicates the 90% significance level. In contrast, the right-hand panel shows that unconstrained households which have received the information expect their income to decline by €90 on average, comparing with those which have not received this information.

The results for expected GDP growth show a large and statistically significant positive effect of the information treatment on the credit-constrained households. On average, such households expect that the future GDP growth will be 4.5 percentage points higher when exposed to the information treatment. The policy announcement leads to a decline in the GDP growth prediction of 1.8 percentage points for the unconstrained households.

Our findings thus suggest that negative signalling effects are only present among the credit-unconstrained households, while the credit-constrained households tend to revise their expectations upwards after the policy announcements.

One possible explanation is that credit-constrained households pay more attention to the actual state of the economy, since they are more exposed to changes in the economy. Another possibility is that the households are credit-constrained because of the adverse economic conditions due to the coronavirus pandemic – and therefore already perceive the economic situation as dire. Then, any announcement of expansionary policy measures leads them to revise their expectations about the future upwards.

Conclusion

Our analysis does not necessarily suggest that households take a negative view of the proposed policy measures or their effectiveness. Rather, it suggests that announcements of large-scale interventions in uncertain times may have unexpected effects on households’ beliefs concerning future economic outcomes. Our study indicates that policy announcements need to be carefully designed and communicated.

Disclaimer |

The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Beckmann, Elisabeth and Tobias Schmidt. "Bundesbank online pilot survey on consumer expectations." Deutsche Bundesbank Technical Paper 01/2020.

- Coibion, Olivier, Gorodnichenko, Yuriy and Michael Weber. "Does Policy Communication during Covid Work?". Unpublished Manuscript. June 2020.

- Kerssenfischer, Mark. "Information effects of euro area monetary policy: New evidence from high-frequency futures data." Deutsche Bundesbank Discussion Paper No 07/2019.

- Melosi, Leonardo. "Signalling effects of monetary policy." The Review of Economic Studies 84.2 (2017): 853-884.

- Nakamura, Emi, and Jón Steinsson. "High-frequency identification of monetary non-neutrality: the information effect." The Quarterly Journal of Economics 133.3 (2018): 1283-1330.

The authors | ||

| Olga Goldfayn-Frank Research Economist, Research Centre Deutsche Bundesbank | Georgi Kocharkov Research Economist, Research Centre Deutsche Bundesbank | Michael Weber Associate Professor of Finance, University of Chicago |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein