How internationally coordinated carbon pricing would affect the economy and welfare Research Brief | 49th edition – June 2022

Climate change is a global challenge that requires international policy coordination. This conclusion is also borne out in a recent study on the macroeconomics implications of carbon pricing. Several different scenarios are considered – different regions introduce carbon pricing schemes unilaterally or in cooperation, and in the presence or absence of border adjustment schemes.

The Paris Climate Agreement back in December 2015 saw many countries agree to pursue ambitious climate targets. A variety of policy measures are currently on the agenda in an effort to achieve these objectives. These include the introduction of a carbon price and a border adjustment mechanism to limit “carbon leakage” – i.e. the relocation of carbon-intensive production of “dirty” goods to regions without a carbon price. In addition, international cooperation in climate policy is an aspiration. For example, the idea of regions getting together to form a “climate club” as described in Nordhaus (2015), i.e. with a common carbon price and a border adjustment mechanism. But how suitable are these measures?

The model

Our study (Ernst et al., 2022) uses the environmental multi-sectoral (EMuSe) model developed at the Bundesbank to outline the economic effects of these policy measures. EMuSe is a three-region macroeconomic model with a multi-sector production structure. In addition to key economic variables, it also contains climate-related variables such as carbon emissions. The regions roughly represent Europe, North America (with Australia), and the rest of the world. On the production side, we model 11 economic sectors. These vary in terms of their size, their use of capital, labour and intermediate inputs, and their emission intensities during production. Firms are able to invest in emissions abatement technologies and do so depending on the carbon price and abatement costs. As a result of the high global carbon emissions, climate change and physical losses cause economic damage that reduces productivity.

Simulations of various climate policy measures

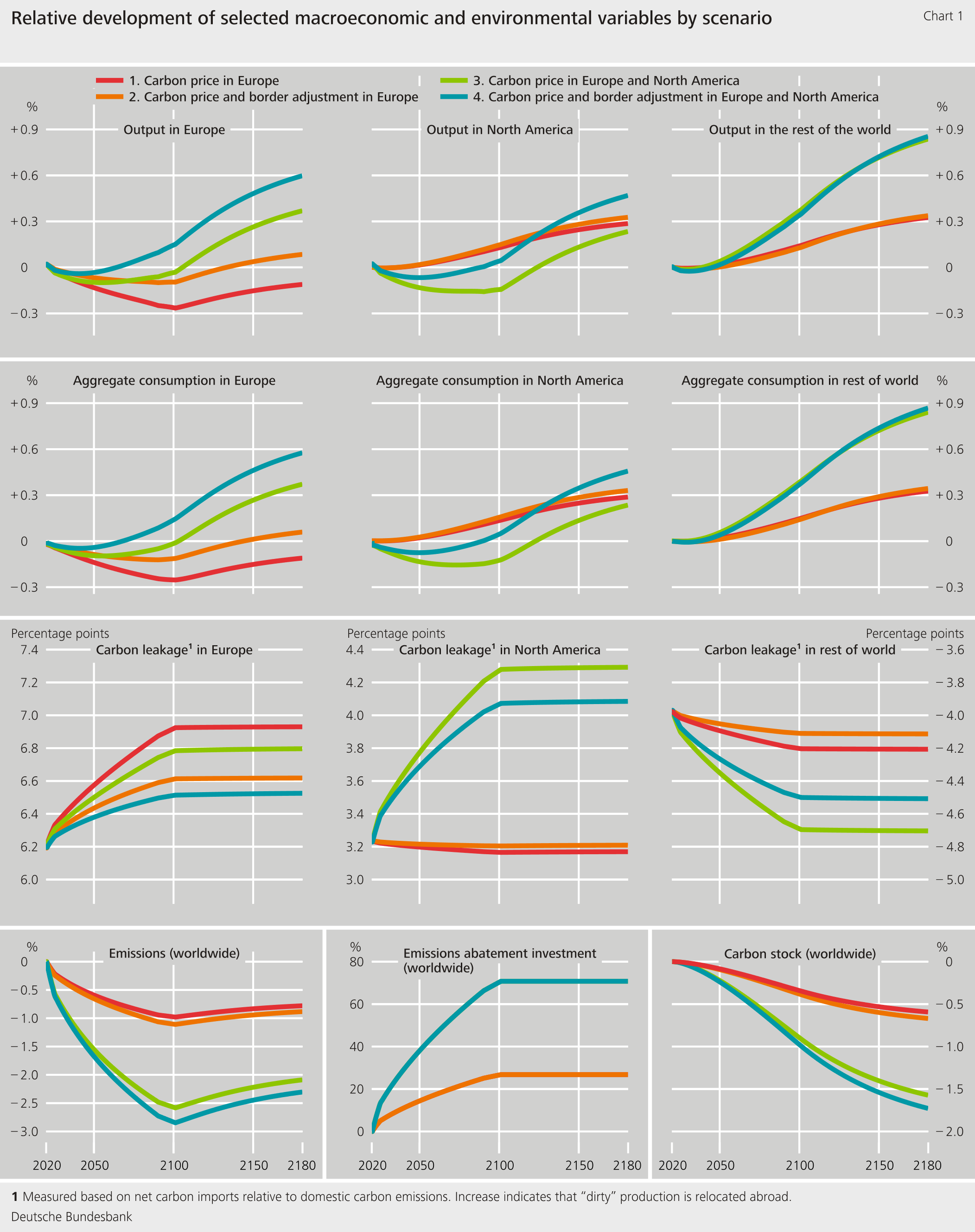

We simulate five policy scenarios under discussion:

- Only Europe imposes a carbon price.

- Only Europe imposes a carbon price and border adjustment taxation on imports against North America and the rest of the world.

- Europe and North America impose a carbon price.

- Europe and North America impose a carbon price and border adjustment taxation against the rest of the world (climate club scenario as in Nordhaus (2015)).

- All regions impose a carbon price (global carbon pricing).

Based on NGFS (2021), our simulations assume that the carbon price in the respective region will increase 13-fold by 2100 and remain constant thereafter. Border adjustment taxes are levied at the domestic carbon price on the estimated emissions content of imports; exports are not exempted. We disregard practical and political challenges surrounding the implementation of the policy scenarios under consideration.

Short-term losses and potential long-term gains of carbon pricing

Chart 1 shows the effects on selected variables in the three regions in scenarios 1 to 4 (relative deviation from the initial steady state). The effects of scenario 5 match those of scenario 4 in qualitative terms. They are, however, significantly larger and are omitted here in order to improve the clarity of the remaining scenarios.

Regions that impose a carbon price suffer macroeconomic losses initially and catch up again over time. These losses arise because production costs increase and products become more expensive relative to those of the other regions. Higher prices reduce demand and income, causing consumption to fall. At the same time, emissions decline as a result of the increased carbon price. As a consequence, the economic damage diminishes, boosting productivity. Other regions without a carbon price benefit directly from positive trade effects (and indirectly from falling emissions), while some of the carbon emissions saved domestically are relocated abroad (carbon leakage).

The border adjustment mechanism changes these trade effects only marginally, given that the resulting relative price increase for foreign goods is rather small (see scenarios 2 or 4). Hence, the border adjustment mechanism does only little to prevent carbon leakage. If, however, domestic exports abroad were exempted from the carbon levy or a much larger tax rate was chosen, this effect could be greater in size. Scenarios in which North America joins Europe in imposing carbon pricing indicate a significantly stronger decline in global emissions (scenarios 3 and 4). Then losses fall worldwide and the catch-up process starts sooner. In addition, a higher long-term level of production is achieved.

Redistribution across regions could enable a global carbon price

The analysis shows that there is an economic incentive to not participate in carbon pricing. This is because positive trade effects are then created and initial macroeconomic losses are avoided. Welfare losses from carbon pricing would be very high, in particular in the rest of the world where per capita gross domestic product is low in relative terms. The model can be used to identify an equilibrium in which all regions benefit over time from a global carbon pricing regime. To this end, the wealthier regions will have to surrender some of their welfare gains from the global carbon price – for example, by means of direct transfers or carbon price discrimination. However, given the nature of model analyses of this kind, the quantification – of welfare functions, in particular – is highly uncertain.

Conclusion

Our model simulations show that, in terms of both environmental policy and the economy, the positive effects of carbon pricing increase with the number of regions that participate. Border adjustment taxation levied on imports (alone) can only prevent negative trade effects to a limited extent. Hence, it reduces carbon leakage only moderately. The incentive to participate in carbon pricing is low, especially for poorer regions. For wealthier regions, it may be advantageous to compensate poorer regions for participating.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

References

- Ernst, A., N. Hinterlang, A. Mahle and N. Stähler (2022). Carbon pricing, border adjustment and climate clubs: An assessment with EMuSE. Discussion Paper, Deutsche Bundesbank, 25/2022.

- NGFS (2021). NGFS climate scenarios for central banks and supervisors. Technical Report June 2021, Network of Central Banks and Supervisors for Greening the Financial System.

- Nordhaus, W. (2015). Climate Clubs: Overcoming Free-Riding in International Climate Policy. American Economic Review 105 (4), 1339-1370.

| Authors |

Anne Ernst Natascha Hinterlang Alexander Mahle Nikolai Stähler |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein