The exchange rate regime is key for the effects of the Bundesbank’s monetary policy on European countries from 1974 to 1998 Research Brief | 54th edition – December 2022

Record inflation in the euro area has led the ECB Governing Council to start raising its key interest rates. The effects on the domestic economy and spillover effects on foreign countries may primarily depend on whether exchange rates are floating or fixed. A new empirical study shows that, during the time of the Deutschmark, the Bundesbank’s monetary policy was transmitted to a significantly greater degree to neighbouring European countries with fixed exchange rates to the Deutschmark than to those with floating exchange rates to the Deutschmark.

We are currently observing record rates of inflation in many European countries. Against this backdrop, the ECB Governing Council, alongside other major central banks, has started to raise its key interest rates. What impact could such an increase in key interest rates have on economies abroad? Are the spillover effects on foreign countries dependent on their exchange rate regimes? As the past decade was characterised by both a policy of zero interest rates as well as non-standard policy measures, our study instead looks at a historical period in which the key interest rate was used as a central instrument of monetary policy: the Bundesbank’s monetary policy from 1974 to 1998.

In our study (Cloyne, Hürtgen and Taylor, 2022), we directly compare the roles of German and US monetary policies to investigate the common hypothesis that US monetary policy has been the main driver of the global economic and financial cycle over the past decades. In addition, we compare how German and US monetary policies were transmitted to European countries with and without fixed exchange rates to the Deutschmark. By doing so, we provide new evidence for what is known as the “international trilemma”. The trilemma states that it is impossible to guarantee a fixed exchange rate, free capital movement, and an independent monetary policy at the same time. Against this theoretical background, the Bundesbank’s monetary policy should have a greater impact on countries with fixed exchange rates than those with floating exchange rates. We assess the international trilemma empirically. To analyse the effects of German monetary policy, we first create a new time series of monetary policy shocks for Germany.

A new time series of monetary policy shocks from the Bundesbank

One challenge when identifying monetary policy effects is the fact that there is mutual interaction between key interest rates and the state of the economy. To unravel this interdependency, we break the key interest rate down into a component that reflects the Bundesbank’s response to the economic situation as well as an unexplained component. The unexplained component corresponds to the monetary policy shock. In this context, it is important to bear in mind that interest rate decisions are made on the basis of real-time data that can be revised at later points in time. The information available retrospectively thus differs from the information available at the times when the central bank was required to make its decisions. To best reflect the information actually available, we examined historical sources from the Bundesbank archive. Specifically, we analysed the minutes for each of the 580 meetings of the Central Bank Council between 1974 and 1998 as well as comprehensive statistical overviews containing real-time data. The component of the key interest rate that is not explained by these real-time data represents our new measure of the monetary policy shock, which we use to investigate the effects of monetary policy in Germany and abroad. In line with other studies (Romer and Romer, 2004), we assume, for simplicity, that the Bundesbank’s reaction function to real-time data is stable throughout the entire period.

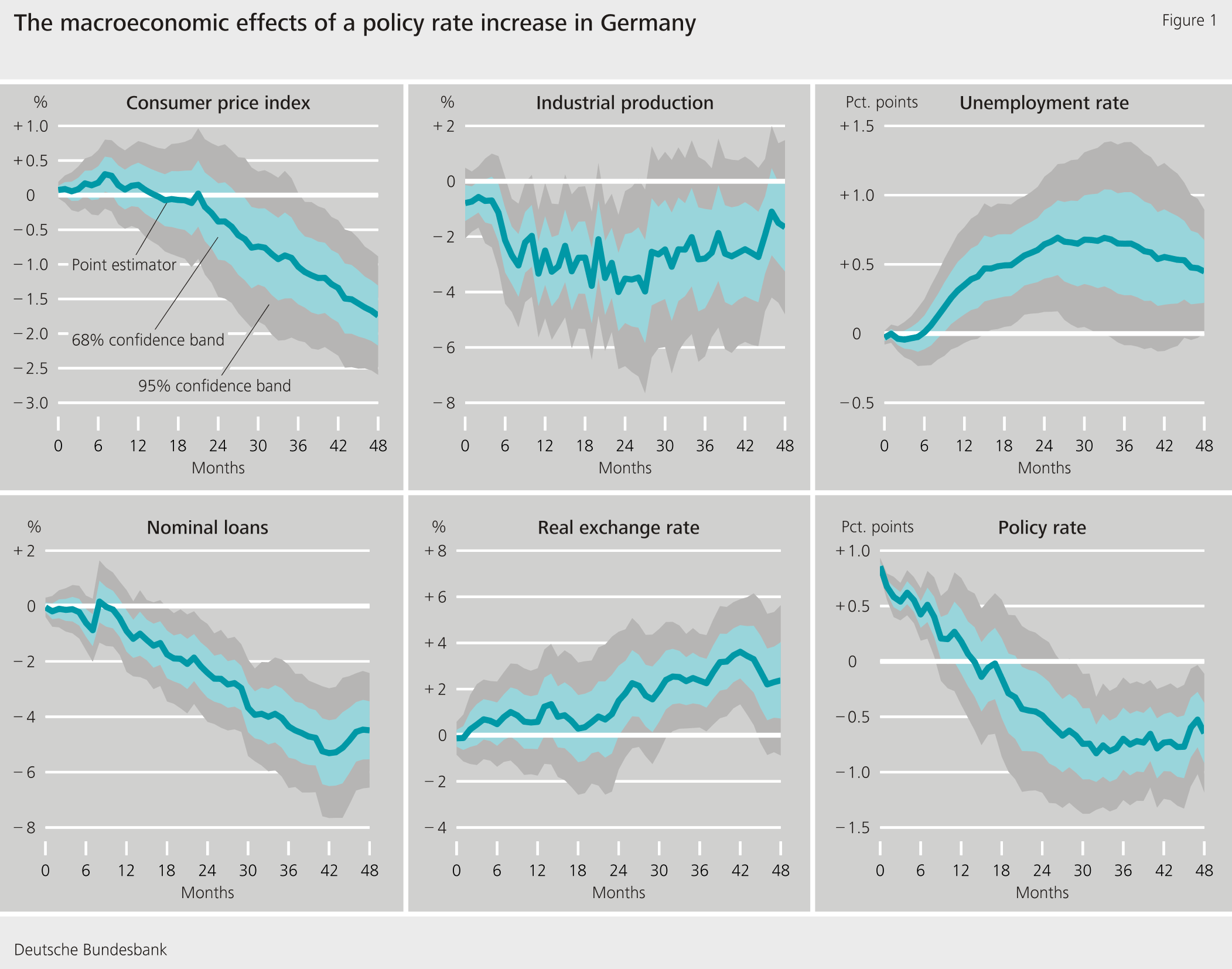

The monetary policy effects of the Bundesbank on the German economy

Following a restrictive monetary policy shock – i.e. an unexpected tightening of the Bundesbank’s monetary policy by 100 basis points – inflation in Germany falls with a lag of a few months. In addition, output declines, unemployment rises, lending decreases and the Deutschmark appreciates in both nominal and real terms (see Figure 1). Reassuringly, the monetary policy effects in Germany are comparable to those for the US and the UK. Our new results therefore not only illustrate the monetary policy effects in Germany, but also complement the sparse results of comparable studies for other countries.

The spillover effects on European countries depend on their exchange rate regimes

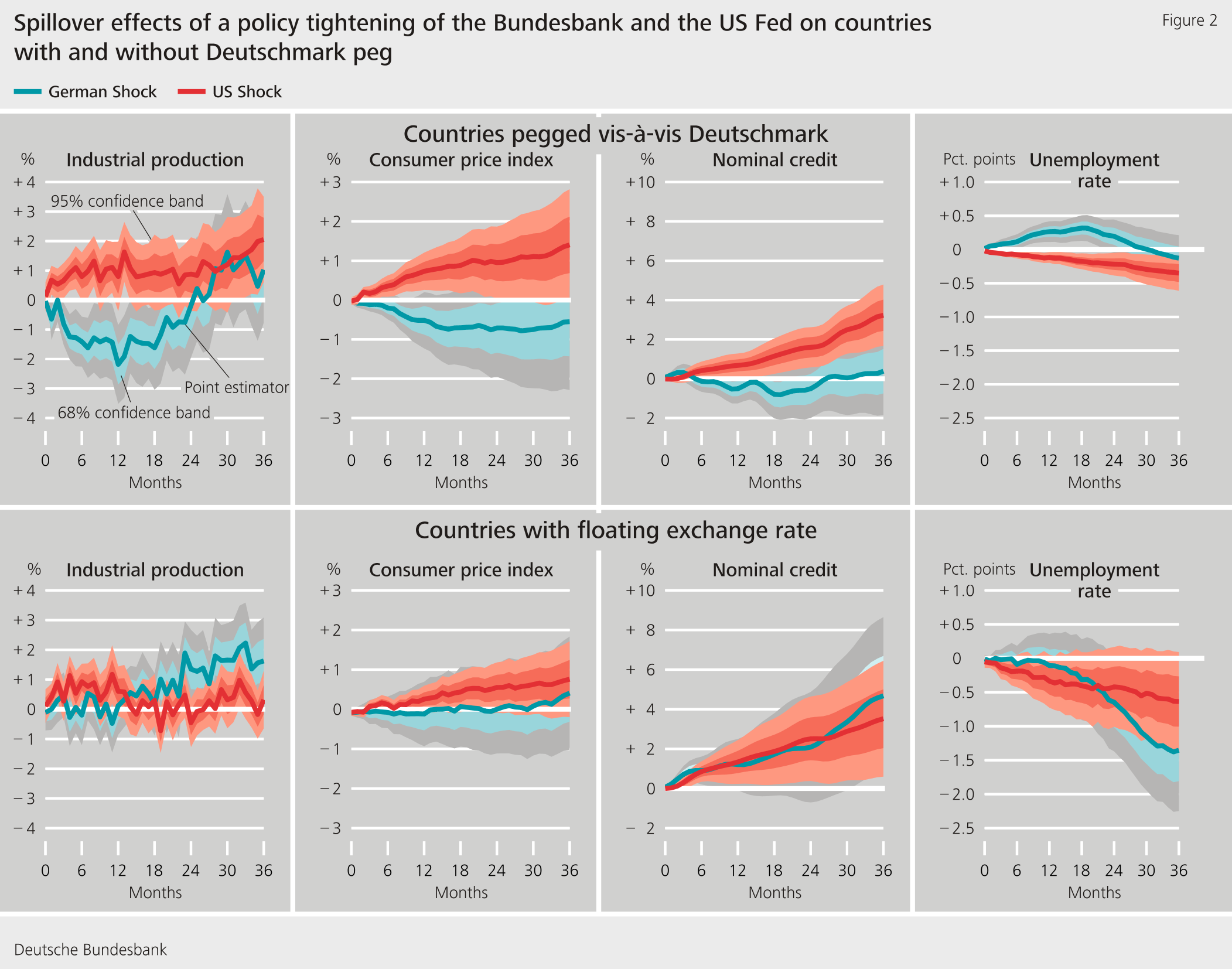

In a second step, we examine the effects of German and US monetary policy on 15 European countries. We separate the countries into those with fixed exchange rates to the Deutschmark and those with floating exchange rates to the Deutschmark, based on a classification that is common in the literature (Ilzetzki, Reinhart and Rogoff, 2019). For example, Switzerland and Norway are countries with floating exchange rates, while the currencies of France and the Netherlands were pegged to the Deutschmark. The analysis begins in April 1979, one month after the establishment of the European Monetary System, and ends in December 1998, which is when the Eurosystem began.

Our empirical results confirm the international trilemma: countries with fixed exchange rates to the Deutschmark were influenced by the Bundesbank’s monetary policy to a greater degree than those with floating exchange rates. Figure 2 shows that, as a result of an unexpected tightening of the Bundesbank’s monetary policy, industrial output fell by 2% in countries whose currencies were pegged to the Deutschmark, while those with floating exchange rates did not experience any downturns in their economies (the blue line in the top row compared with the bottom row). Prices and lending likewise fell more sharply in countries whose currencies were pegged to the Deutschmark than in those with flexible exchange rates.

Previous studies, including Miranda-Agrippino and Rey (2020), have examined the role of US monetary policy in the global economic and financial cycle. By contrast, our analysis allows to consider the effects of German and US monetary policy jointly for the first time. Compared with the spillover effects of a monetary policy shock originating from the US to other countries, the spillover effects from Germany are equally or even more significant (the blue lines compared with the red lines in Figure 2). Thus, the Bundesbank’s monetary policy also played an important role in the international economy during the period under review.

Conclusion

In our study, we show that the Bundesbank’s monetary policy during the time of the Deutschmark not only had a major impact on the domestic economy, but also had strong spillover effects on neighbouring European countries with fixed exchange rates to the Deutschmark. Our results are thus consistent with the international trilemma and illustrate that exchange rate regimes play a key role for the spillover effects of monetary policy on other countries.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

References

- Cloyne, J. S., P. M. Hürtgen, and A. M. Taylor (2022), Global monetary and financial spillovers: Evidence from a new measure of Bundesbank policy shocks, Deutsche Bundesbank Discussion Paper No 34/2022.

- Ilzetzki, E., C. M. Reinhart, and K. S. Rogoff (2019), Exchange Arrangements Entering the 21st Century: Which Anchor Will Hold?, Quarterly Journal of Economics, Vol. 134, No 2, pp. 599-646.

- Miranda-Agrippino, S. and H. Rey (2020), U.S. Monetary Policy and the Global Financial Cycle, The Review of Economic Studies, Vol. 87, No 6, pp. 2754-2776.

- Romer, C. D. and D. H. Romer (2004), A New Measure of Monetary Shocks: Derivation and Implications, American Economic Review, Vol. 94, No 4, pp. 1055-1084.

| Authors | ||

| James Cloyne Associate Professor of Economics, University of California, Davis |

Patrick Hürtgen Economist at the Bundesbank’s Research Centre |

Alan M. Taylor Distinguished Professor of Economics and Finance, University of California, Davis |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein