Banks’ internal credit risk models: incentives for implementation and impact on risk management Research Brief | 59th edition – July 2023

Internal risk models play an important role in ensuring capital adequacy at banks. Banking supervisors keep a particularly close eye on them, as banks have some degrees of freedom when it comes to model design. A new study examines the incentives for banks to implement internal risk models, analyses their impact on risk management and explains possible consequences of a new regulatory proposal regarding application of such models.

One of the key tasks of banking supervision is to make sure that banks hold adequate equity capital. The minimum capital requirements for a given bank depend on that bank’s individual risk exposures. Banks can choose between two ways of determining their minimum capital requirements for credit risk: the standardised approach and the internal ratings-based approach (IRBA). As the name suggests, the standardised approach is the less complex of the two, and it is often the method used by smaller banks.

By contrast, the IRBA allows banks to design their own risk model. Those models are reviewed by supervisors and approved for use in calculating minimum capital requirements. From a supervisory perspective, this should enable banks to better understand their own risk exposures and thus improve their risk management. But it also provides banks with some discretion when it comes to model design. Some studies suggest that banks may, in some cases, exploit that fact to reduce their capital requirements (Vallascas and Hagendorff, 2013; Mariathasan and Merrouche, 2014). Over time, supervisory authorities have taken steps to restrict the scope afforded to banks in this regard.

New partial use philosophy leading to a paradigm shift

Cases where banks calculate their capital requirements for credit risk using the IRBA have, up to now, been governed by two basic principles in Europe: banks are permitted to adopt a phased IRBA implementation and are required to apply the IRBA for all exposures subject to credit risk within a set period of time. However, the new partial use philosophy put forward by the Basel Committee on Banking Supervision (BCBS) is now initiating a paradigm shift to some extent, in that it envisages permitting banks a permanent partial use of the IRBA, for only some of their exposures.

Our analysis identifies possible implications of this new partial use philosophy. We examine, first, the trade-off for banks between the costs of implementing the IRBA, the so-called rollout, and a possible associated reduction in capital requirements as a result of lower risk-weighted assets (RWAs). Second, we analyse whether banks’ risk management improves as rollout progresses. Analysing IRBA implementation is important, as hesitant rollouts with little progress over time may point to opportunistic behaviour by banks and can also ultimately lead to insufficient bank capital.

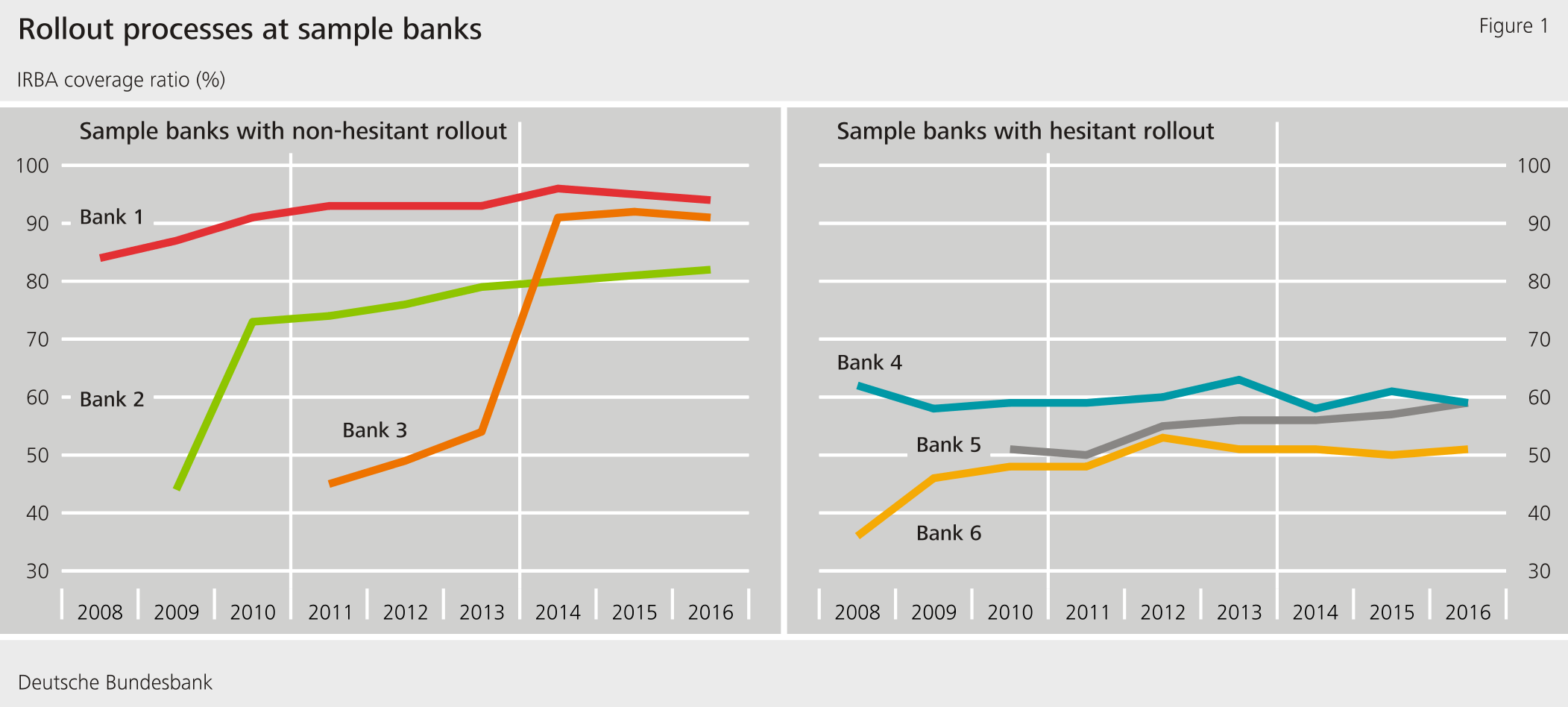

For our empirical analysis, we use a comprehensive dataset covering around 350 European banks. We study the period from 2007 onwards, as most countries introduced the IRBA under Basel II in 2007 and, accordingly, many banks embarked on implementation in the years following that. Looking at banks’ annual reports, we extract their IRBA coverage ratios, expressing the percentage of their credit risk exposures for which they already use the IRB methodology.

Significant discrepancy between banks in terms of speed of IRBA implementation

Based on our dataset, we observe that banks exhibit highly heterogeneous progress over time in rolling out the IRBA. Some banks already start out with a very high IRBA coverage ratio or show significant progress within a few years (see left-hand panel of Figure 1), whilst others are hesitant to roll out (see right-hand panel of Figure 1). When comparing similar banks with different rollout behaviour, we find that the annual increases in the costs associated with adopting the IRBA are smaller for banks with a hesitant rollout than for those progressing at a faster pace. Accordingly, banks that heavily gear their behaviour towards cost considerations might have an incentive to roll out the IRBA slowly.

First IRBA implementation steps bring the biggest reductions in RWAs

Moreover, we observe that the first steps of the IRBA implementation process produce the most substantial RWA reductions for banks. Subsequent implementation steps often entail only a small reduction in RWAs compared with the standardised approach or even no reduction at all. One explanation could be that banks first apply the IRBA to those exposures that promise the largest RWA reductions and corresponding savings in terms of capital requirements. This leads us to the conclusion that, as rollout progresses, the incentive to bear the costs of fully implementing the IRBA will diminish.

Banks’ risk management improves as rollout progresses

Furthermore, the results of our analysis suggest that banks’ risk management, as measured by loan portfolio quality and credit risk prediction accuracy, improves as rollout progresses. This also corresponds to the original intention of supervisors, namely that adopting the IRBA would allow banks to better assess their own risk exposures. Given that the positive effects of a progressing rollout are limited to the part of banks’ portfolios to which the IRBA is applied, the novel partial use philosophy could lessen these effects as compared to a full rollout. At the same time, however, there is also less of an entry barrier for banks that have so far been using only the standardised approach. It is to be assumed that these banks would see improvements in their risk management.

Conclusion

In our analysis, we examine how banks roll out internal risk models and the possible effects that the new partial use philosophy might have. There are clear differences between individual banks when it comes to rolling out internal credit risk models. Banks pursuing a hesitant IRBA rollout approach exhibit lower cost growth rates. Furthermore, the greatest RWA reductions coincide with the first implementation steps. At the same time, we observe that banks’ risk management improves as rollout progresses.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

References

- Mariathasan, M. and O. Merrouche (2014). The manipulation of Basel risk weights. Journal of Financial Intermediation 23, pp. 300-321.

- Vallascas, F. and J. Hagendorff (2013). The risk sensitivity of capital requirements: Evidence from an international sample of large banks. Review of Finance 17, pp. 1947-1988.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein