Lower TARGET2 payment flows due to EU sanctions against Russia Research Brief | 55th edition – February 2023

In recent years, the European Union has imposed various types of financial sanctions against Russian banks. A new study examines whether these measures have affected payment flows in TARGET2.

Russia’s annexation of the Crimean peninsula in March 2014 prompted the European Union (EU) to impose financial sanctions against Russia for the first time. In mid-2014 the EU decided to take targeted measures against both individuals and individual Russian credit institutions. Following the Russian invasion of Ukraine on 24 February 2022, the EU tightened and extended the existing sanctions.

Financial sanctions are generally aimed at restricting cross-border financial activities in a target country and exerting indirect political pressure through the associated economic costs. However, in order to achieve this objective, it is important to design sanctions correctly and implement them effectively in practice. The existing empirical literature analyses various aspects of sanctions against Russia, but often focuses only on trade patterns of goods.

A new study now examines the impact of financial sanctions on cross-border payment flows using information on individual accounts that banks maintain within the Eurosystem. We use data from the Eurosystem’s real-time gross settlement system, TARGET2. The dataset contains information on the originator and beneficiary of a euro payment, including the accounts of the direct TARGET2 participants, as well as the date and value of the transaction. This allows the identification of payments in TARGET2 initiated by a Russian bank or intended for a Russian bank, each of which is settled via a correspondent bank in the EU.

This approach identifies the impact of sanctions more clearly than the existing literature. First, the EU has imposed restrictive measures on only a few selected banks in Russia. We can therefore distinguish between sanctioned and non-sanctioned banks in a country that is the target of sanctions. Second, sanctions have been modified over time so that we can analyse the impact of various types of financial constraints. Third, data are available on a daily basis, which allows for a greater degree of differentiation in the analysis. Fourth, we are also able to compare the impact of the financial sanctions imposed on Russian banks in 2014 following the Russian annexation of Crimea and in 2022 following the Russian invasion of Ukraine. The study uses a differences-in-differences estimator to evaluate the effect of the sanctions. It illustrates how the Bundesbank can use available microdata to investigate current issues in a timely manner.

Financial sanctions in practice

The study distinguishes between three different types of financial sanctions against Russian banks: Capital market sanctions, the SWIFT exclusion and prohibitions on disposal.

At the cut-off date of the analysis, nine Russian banks were subject to capital market sanctions. This is accompanied by a ban on EU market participants from buying, selling, providing or otherwise acting on transferable securities and money market instruments issued by sanctioned institutions, securities or ancillary services. As a result, these Russian banks in the EU are no longer able to refinance themselves through capital market instruments.

The SWIFT exclusion prohibits the exchange of financial data for payments in SWIFT. However, the affected Russian institutions can continue to make international credit transfers either via alternative payment systems, such as the Chinese Cross-border Interbank Payment System (CIPS), or via other secure communication channels, such as secure fax lines.

A prohibition on disposal of funds and economic resources freezes all funds and economic resources owned or held by natural or legal persons, entities or organizations associated with the sanctioned institutions. No funds or economic resources may be made available directly or indirectly to those affected.

Probably lower payment flows in TARGET2 due to sanctions

The analysis suggests that, in TARGET2, payments flows for both non-sanctioned and sanctioned Russian banks decline overall. For sanctioned banks, however, this effect is considerably stronger.

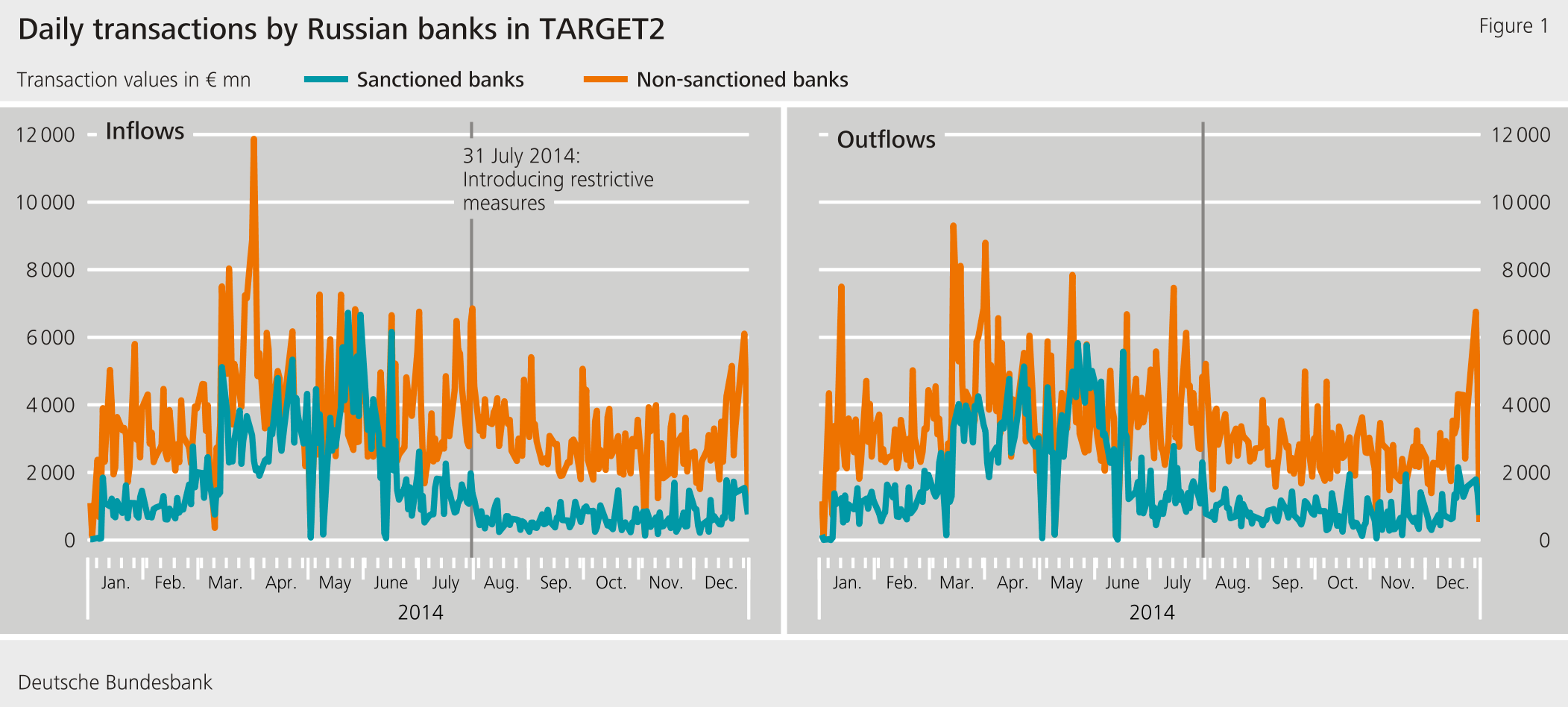

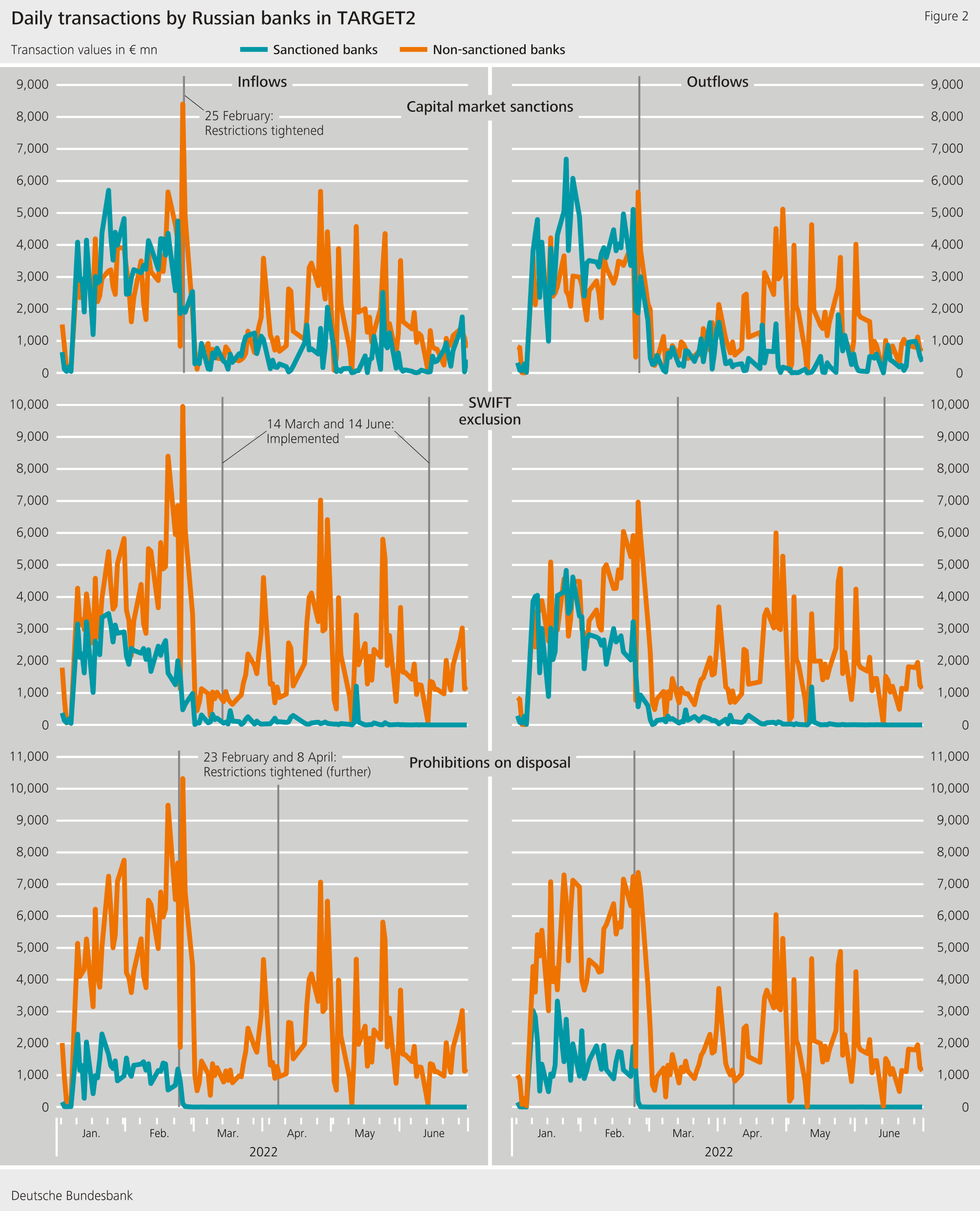

For 2014 and for January to June 2022, charts 1 and 2 illustrate the daily aggregate inflows and outflows in TARGET2 via the accounts of Russian banks, broken down by sanctioned and non-sanctioned entities. Russian banks affected by capital market sanctions made fewer payments in TARGET2 before the sanctions were implemented. The difference from non-sanctioned Russian banks becomes then even greater. In addition, business activity in TARGET2 almost completely dried up as soon as a bank was excluded from SWIFT or was subject to a prohibition on disposal of funds.

Empirical estimates show that financial sanctions reduced inflows and outflows from bank accounts of sanctioned Russian banks compared with accounts of non-sanctioned Russian banks. The measures had a stronger impact in 2022 than in 2014. This is due to stricter measures (SWIFT exclusion and prohibitions on disposal) which were implemented in 2022. The SWIFT exclusion appears to have the strongest impact on payment flows in TARGET2.

When interpreting the results, it should be noted that TARGET2 represents only a part of international payment transactions. Even after a SWIFT exclusion, Russian banks can continue to make international payments via alternative communication channels or other payment systems, such as the Chinese CIPS. Furthermore, we do not investigate any evasions and therefore cannot completely rule them out.

Conclusion

Our results suggest that financial sanctions reduce payment flows in TARGET2, with the SWIFT exclusion having the greatest impact. This effect is stronger in 2022 than in 2014. However, the analysis of evasion is not part of this analysis.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

References

Drott C., S. Goldbach und V. Nitsch (2022): “The Effects of Sanctions on Russian Banks in TARGET2 Transactions Data”, Deutsche Bundesbank Discussion Paper No 38/2022.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein