Negative interest rate policy led to negative interest rates on corporate deposits and higher fees Research Brief | 56th edition – March 2023

The Eurosystem’s negative interest rate policy (NIRP) incentivised banks to also charge their customers negative deposit rates. My analysis shows that German banks did actually charge negative interest rates on corporate deposits at times. However, the banks that did so were primarily those which relied heavily on household deposits as a source of funding. These banks were very reluctant to apply negative interest rates to household deposits as well, and thus probably faced particularly high margin pressure. It was primarily these banks that also charged higher fees in order to ease this pressure.

Against the backdrop of low inflation, the ECB Governing Council decided in June 2014 to lower the interest rate on the deposit facility from 0% to -0.10%. In the following years, the rate was reduced further to -0.50%. In mid-2022, the Governing Council finally ended the period of negative interest rates in view of the marked rise in inflation. My analysis examines German banks’ response during the negative interest rate policy (NIRP) period via their deposit rates.

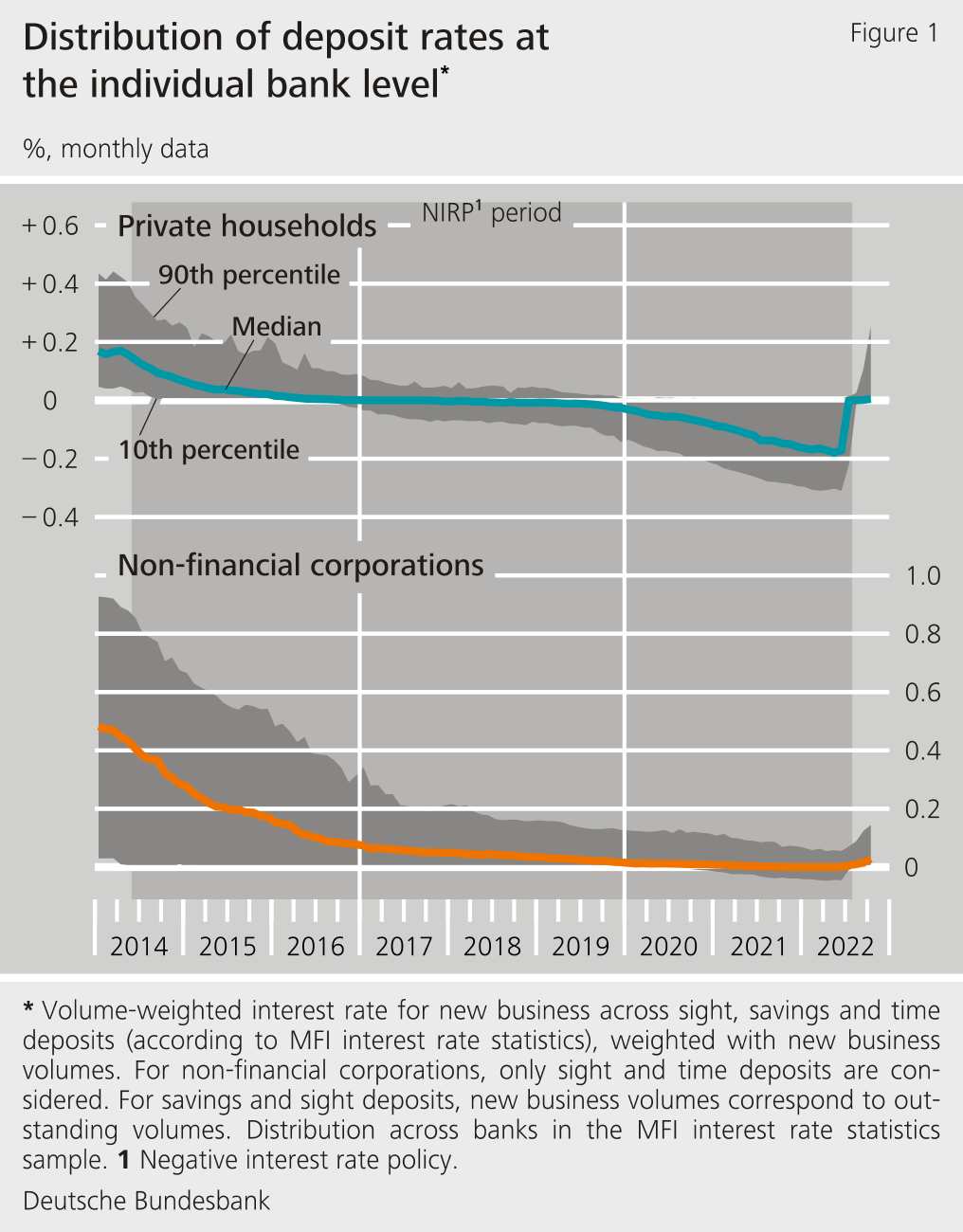

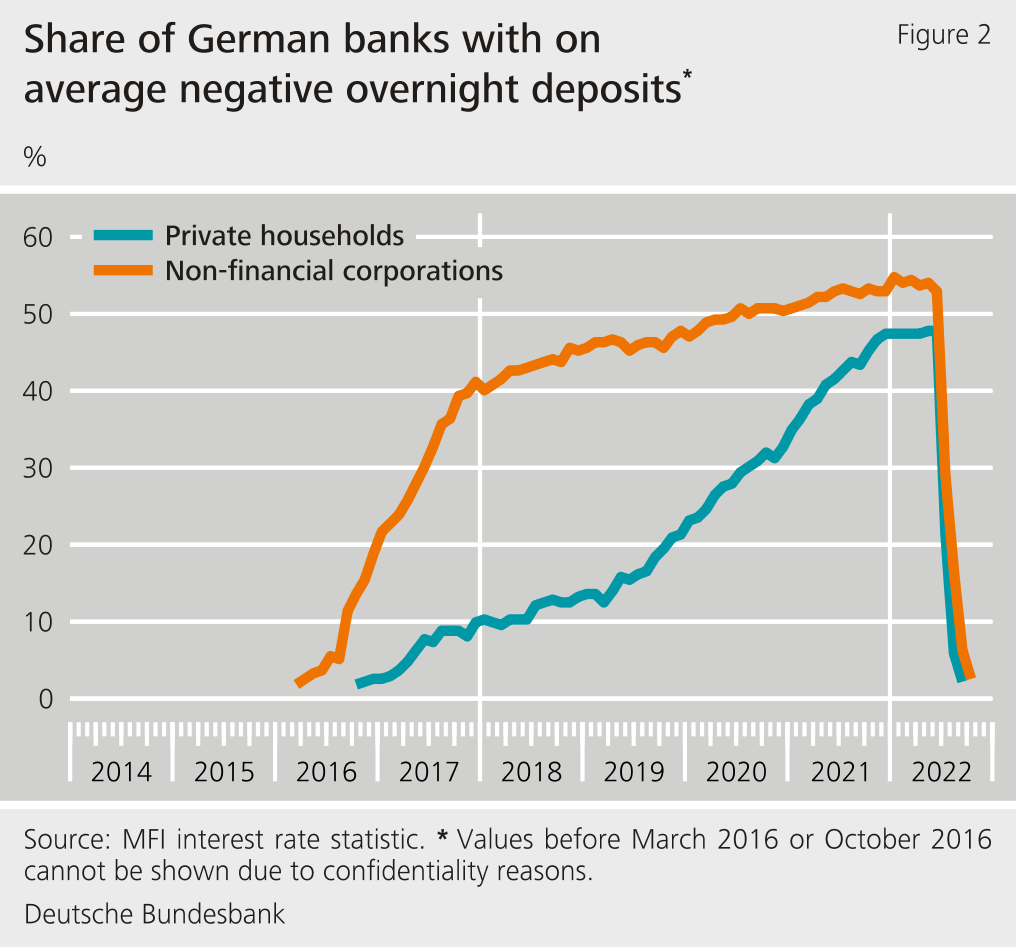

German banks’ deposit rates mostly hovered around zero during the NIRP period (Figure 1). This was especially true of deposit rates for households. At the same time, lending rates declined in line with general interest rate developments. Thus, the interest margin on banks’ lending and deposit business, i.e. the difference between the lending rate and the deposit rate, narrowed. There are different ways in which banks can respond to the pressure this places on their profitability. One option is to charge negative interest rates on customer deposits. Banks in Germany did also actually charge negative interest rates on deposits, especially on corporates’ overnight deposits (see Figure 2). Overnight deposits are deposits that are available at any time. Banks can also try to generate more income from fees and commissions. This analysis examines both options independently of one another and raises the question as to which characteristics are shown by the banks that chose one of these two options.

In order to answer this question, I combine bank-specific data from several microdatasets. The first step is to analyse which bank characteristics increase the likelihood of an institution charging negative deposit rates. The second step is to use a panel model to estimate which bank characteristics led to higher fees and commissions.

Which banks charged corporates negative deposit rates?

First, I investigate which bank characteristics increase the likelihood of a bank in Germany charging negative interest rates on corporate deposits. My results show that negative interest rates were passed through particularly strongly to corporates by banks funded by a large share of household deposits (Michaelis, 2022), giving rise to the hypothesis that these banks faced greater pressure on their margins. This could be due to the fact that banks found it more difficult to charge negative interest on household deposits, and were therefore more reluctant to do so. Negative corporate deposit rates are one way in which they may have attempted to mitigate this pressure on interest margins.

By contrast, a higher share of excess liquidity had only a limited impact on the likelihood of a bank charging negative interest rates on corporate deposits. This is consistent with the fact that the costs of holding excess liquidity were comparatively low compared with the costs of shrinking interest margins, for example. “Excess liquidity” denotes banks’ predominantly short-term credit balances on their central bank accounts in excess of their required reserves. Viewed in isolation, higher levels of excess liquidity reduced banks’ net interest income because the latter was subject to a negative interest rate during the NIRP period.

Which banks increased their fees?

Besides applying negative interest rates to deposits, there are other instruments, such as higher fees and commissions, which banks can use to alleviate the pressure that a declining interest margin exerts on their profitability. My results suggest that banks increased their fees and commissions especially if they were increasingly dependent on household deposits for funding. Expressed in figures, banks’ net commission income per euro of household deposits went up by around 0.08 cent during the NIRP period compared with the previous period. This increase may seem small, but is equivalent to around 16% of the commission margin. By contrast, the level of excess liquidity did not affect the commission margin.

This suggests that banks changed their business model somewhat during the period of negative interest rates, generating higher fees and commissions from household deposits in deposit business, for example. However, they may also have used business with households to sell other banking services in order to generate commission.

Conclusion

In summary, it appears that banks were generally reluctant to charge negative interest rates on household deposits. The findings show that banks for which these household deposits were an important source of funding mainly followed two paths: they applied negative interest rates to corporate deposits, and they increased their commission margin.

My results are consistent with the empirical literature, which likewise confirms that banks that increasingly obtained funding via traditional customer deposits were more exposed to the difficulties of the NIRP period. This is because the interest margins of these banks probably came under more pressure. It is not surprising, then, that there was a stronger tendency among these banks to apply negative interest rates to corporate deposits and generate higher commission surpluses.

In the wake of the ongoing normalisation of monetary policy, German banks are likely to abolish negative interest rates on their customer deposits over time. Figures 1 and 2 show that negative deposit rates have already declined significantly in recent months. The main reason for this is likely to have stemmed from competitive pressure, first of all. This pressure arises from alternative forms of investments for bank customers, for example from rising yields on risk-free securities and bonds. By contrast, the effect via the interest margin may be less relevant at present. It increases over time, as banks tend to raise lending rates faster than deposit rates during periods of monetary policy tightening (Andries and Billon, 2016). In other words, tightening and easing periods have an asymmetric effect on banks’ interest rate pass-through because banks try to maximise their interest margin. Moreover, the previous compression of the interest margin in the context of the low interest rate environment should tend to amplify this effect further. Current developments therefore suggest that the effect on deposit rates via the interest margin is currently likely to be less relevant.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

References

- Andries, N. and S. Billon (2016), Retail bank interest rate pass-through in the euro area: An empirical survey, Economic Systems 40 (1), 170-194.

- Michaelis, H. (2022), Going below zero – How do banks react?, Deutsche Bundesbank Discussion Paper No 33/2022.

| Author |

© Vero Bielinski

Economist at the Deutsche Bundesbank, Directorate General Economics |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein