The effectiveness of green collateral policy as an instrument of climate policy Research Brief | 57th edition – April 2023

The debate surrounding climate change mitigation measures has lately also extended to central bank instruments. One of the points under discussion is the preferential treatment of green bonds in central bank monetary policy operations. This would improve the financing conditions of firms with low emissions and thus create an incentive for green investment. Using a novel model, we analyse the climate policy and macroeconomic implications of a green-tilted collateral policy and are able to identify only minor effects on green investment.

Mitigating anthropogenic climate change is one of the greatest challenges facing economic policy over the coming decades. Owing to the inadequate fiscal measures (such as carbon pricing) currently being taken to address climate change (IPCC Report, 2021), there have recently been calls on investors in general and central banks in particular to proactively combat climate change. Since its 2021 strategy review, the European Central Bank (ECB) has included climate objectives in its monetary policy, provided this does not conflict with the primary mandate of price stability (ECB, 2021). In our study (Giovanardi et al., 2022), we investigate whether the preferential treatment of green bonds in the collateral framework can be a suitable environmental policy instrument.

We develop a dynamic stochastic general equilibrium model in which firms finance their activities by issuing equity or by issuing debt in the form of corporate bonds. They thus decide on their funding structure. The bonds are held by banks which, in turn, can post them to the central bank as collateral for short-term loans. Since bonds carry default risk, central banks accept corporate bonds as collateral only subject to a haircut. For a bank, the lower the central bank haircut, the more valuable a bond is. As banks are competitive, firms issuing bonds with small haircuts can obtain cheaper funding.

In our model, there are two types of firms that issue bonds: conventional and green. Conventional firms generate greenhouse gas emissions during the production process, which give rise to macroeconomic costs given their contribution to global warming. However, these costs are not borne by firms but by the general public. Emissions are therefore a negative externality. By contrast, green firms do not emit greenhouse gases in their production process.

If the central bank applies a smaller haircut to bonds issued by green firms than to those issued by comparable conventional firms, green bonds become more appealing from the banks’ perspective, given their increased collateral value. Banks thus increase demand for them. Green firms change their capital structure, issue more bonds and increase their investment. The aggregate share of green investment in the economy rises, implying that greenhouse gas emissions fall. However, the leverage ratio of green firms also increases, which ultimately leads to rising default risk for green bonds.

This undesirable side effect on debt sustainability does not occur in the case of a carbon tax, as this only affects the attractiveness of investment in physical capital, but does not increase the attractiveness of bonds relative to equity financing. As a result, in our model framework, a carbon tax leads to a much better result in macroeconomic terms than a green collateral policy. As soon as emissions are priced to maximise welfare, there is no argument in our model in favour of a green-tilted collateral policy.

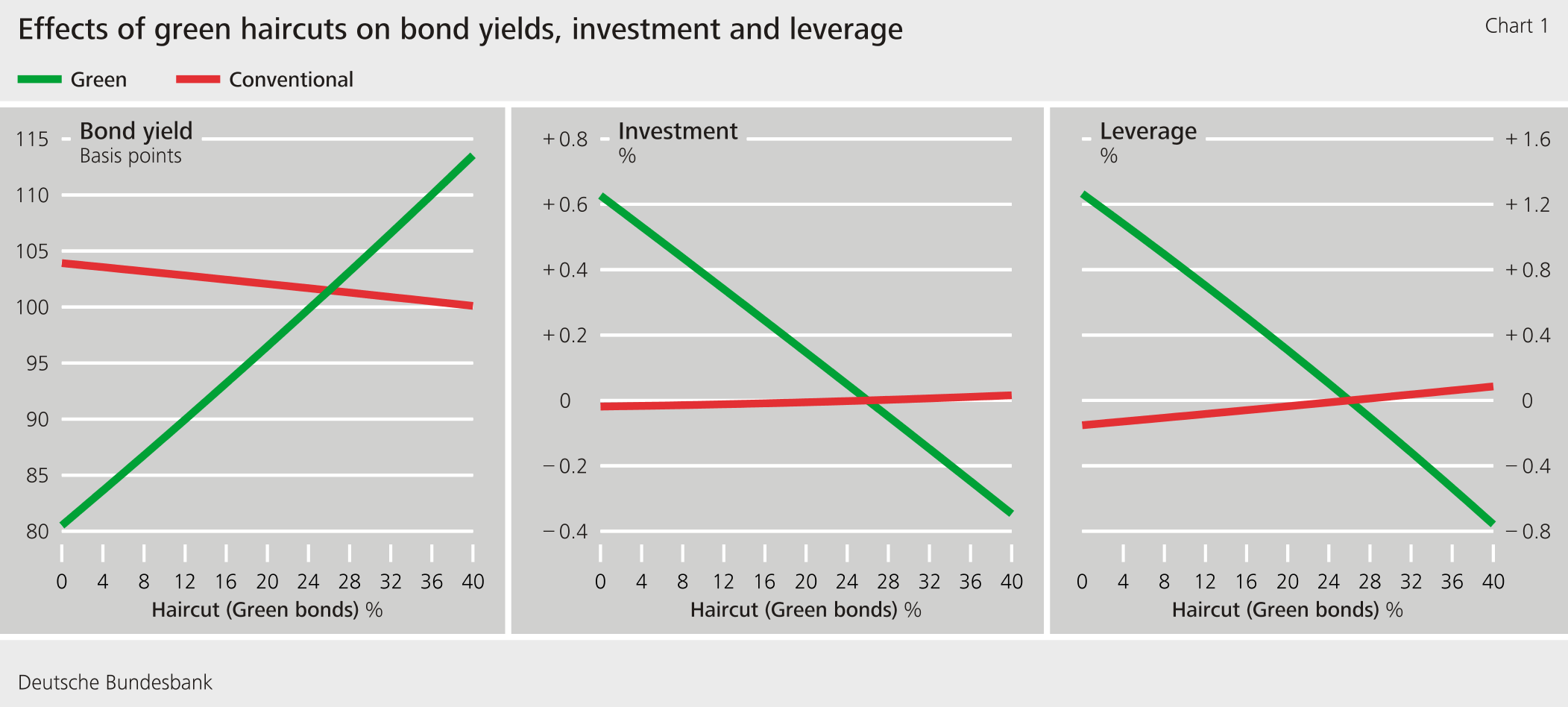

In qualitative terms, these results are unsurprising. We therefore use our model to make a quantitative estimate of the size of these effects. Our quantitative analysis is based on euro area data from 2010 – 2019, the results are shown in Figure 1.

Starting from a haircut of 26% on corporate bonds with a residual maturity of five years and a BBB rating (green line), the yield on green bonds would fall by around 20 basis points if the haircut were reduced to zero (Figure 1, left). As a result of this reduction in financing costs, green firms issue more bonds. In the model, green investment increases only by around 0.6% if the relevant haircut drops to zero (Figure 1, middle). Thus, not all proceeds from issuing bonds are invested. Some of the proceeds are used to increase dividends, meaning that the relevant firms’ leverage ratio rises and debt sustainability decreases (Figure 1, right). This is consistent with the empirical literature, such as Grosse-Rueschkamp et al. (2019), Todorov (2020), Macaire and Naef (2022), Eliet-Doilet and Maino (2022) and Chen et al. (2022).

Since the positive effect on green investment outweighs the negative effect on debt sustainability, green-tilted collateral policy can indeed have a welfare-enhancing effect in our model. However, two points must be considered. First, imprecise calibration of the haircuts may lead to welfare losses, for example if conventional bonds have such a large haircut that the total amount of collateral becomes too low. Second, the impact of a green collateral policy on the share of green investment is fairly small. As the difference between green and conventional bond yields under the welfare-maximising collateral policy is only 18 basis points, the increase in green investment is smaller than required from an environmental policy perspective – by a factor of around 100. It is impossible to induce the necessary share of green investment through preferential collateral treatment of green, as the haircuts on green bonds cannot be smaller than zero and those on conventional bonds cannot be greater than 100%.

Our macroeconomic analysis abstracts from bonds whose payment structure is directly dependent on emissions (sustainability-linked bonds). This may affect the quantitative conclusions about the expected effects, but the qualitative conclusions of our analysis remain unaffected. Furthermore, the mechanisms discussed here are also applicable to asset purchase programmes and banks’ capital requirements because in these cases, too, monetary policy and regulatory instruments influence demand for corporate bonds and loans. Finally, the analysis focuses to medium-term effects and does not explicitly discuss implications for the primary mandate of price stability.

Conclusion

Under certain assumptions, the preferential treatment of green bonds in the central bank’s collateral portfolio has a welfare-enhancing effect. However, owing to undesirable side effects on the leverage ratio of green firms, this policy is a qualitatively and quantitatively imperfect substitute for carbon taxation. If the current collateral framework underestimates transition risks and physical risks of conventional firms, the haircuts on those firms’ bonds should of course be increased. In that case, however, the relative preferential treatment of green bonds would be a risk management instrument of the central bank intended to prevent climate change from having negative effects on monetary policy operations.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

References

- ECB press release (2021). ECB presents action plan to include climate change considerations in its monetary policy strategy.

- Eliet-Doillet A. and Maino A. (2022). Can Unconventional Monetary Policy Contribute to Climate Action? Unpublished manuscript.

- Chen H., Chen Z., He Z., Liu J. and Xie R. (2022). Pledgeability and Asset Prices: Evidence from the Chinese Corporate Bond Markets. Journal of Finance, forthcoming.

- Giovanardi F., Kaldorf M., Radke L. and Wicknig F. (2022). The Preferential Treatment of Green Bonds. Deutsche Bundesbank Discussion Paper No 51/2022.

- Grosse-Rueschkamp B., Steffen S. and Streitz D. (2019). A Capital Structure Channel of Monetary Policy. Journal of Financial Economics 133, 357-378.

- IPCC (2021). Summary for Policymakers. In Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press.

- Macaire C. and Naef A. (2021). Greening Monetary Policy: Evidence from China. Climate Policy 1-12.

- Todorov, K. (2019). Quantify the Quantitative Easing: Impact on Bonds and Corporate Debt Issuance. Journal of Financial Economics 135(2), 340-358.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein