Rent or buy? How equity requirements for households influence decisions on home financing Research Brief | 60th edition – August 2023

Some households contribute only a small amount of equity when buying property financed by a loan. If they then default on the loan, lenders may incur losses. Should the problem affect a large number of lenders, this could potentially jeopardise financial stability. Minimum requirements for the own funds households need to provide can limit losses that may arise. However, this would mean that some households can no longer obtain loans in the desired amount. A Bundesbank study shows that a large proportion of the households interested in buying which would be affected by this are then willing to buy a cheaper property or to save more in order to buy at a later date. The impact on homeownership is therefore likely to be smaller in the medium than in the short term.

The smaller the share of own funds a borrower provides when taking out a housing loan, the higher the lender’s loss in the event of a default. If households generally provide only a small amount of equity – that is, if in this respect lending standards are loose in the financial system as a whole – and many loans default at the same time, the resulting losses can affect numerous lenders and thus jeopardise financial stability. Supervisors can reduce the risks to financial stability stemming from loosening lending standards by setting minimum standards for the equity borrowers need to contribute when taking out a housing loan (Bundesbank 2015). In Germany, the Federal Financial Supervisory Authority (BaFin) has the authority to set such minimum standards since 2017. It has not yet made use of this option.

Previous research on the topic and the experiences of other countries show that these kinds of minimum requirements can reduce growth in house prices and housing loans and help to cool overheating in real estate markets (Alam et al. 2019). However, the requirements imply that buyers who have only a small amount of equity may no longer be able to fully satisfy their wishes, at least in the short term. Households with low income or little wealth are particularly affected (Acolín et al. 2016). In response to the requirements, these households tend to move to other residential areas (Tzur-Ilan 2017), for example, or to buy smaller properties (Araujo et al. 2020). We therefore examined how German households would act in the event of minimum requirements – irrespective of whether these stem from the banks themselves or are imposed by supervisors because of risks to financial stability (Bundesbank 2022).

Not all households want to become homeowners and households wishing to buy adjust their behaviour

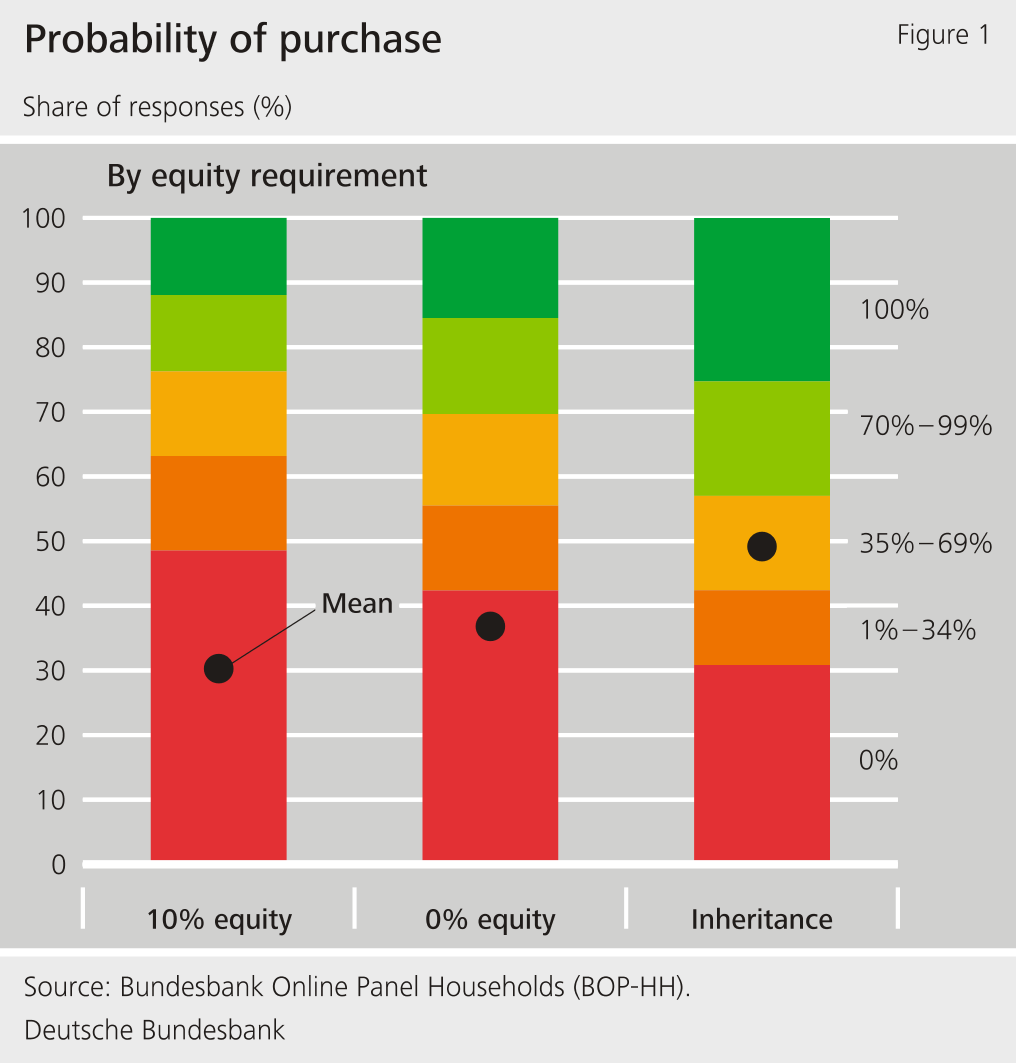

As part of the Bundesbank Online Panel Households (BOP-HH), in February 2022 we asked more than 4,000 households in Germany about their willingness to buy a property. In line with a study by Fuster and Zafar (2016), we initially gave two different figures for the minimum amount of equity (10% and 0%) that households would have to provide. Additionally, in both cases households also have to use their own funds to cover transaction costs associated with the purchase coming to 10% of the purchase price. In a third hypothetical scenario, households were told to assume that they receive an inheritance which exactly covers the transaction costs and the required equity. In other words, a purchase could be made without any financial reserves in the third scenario. In all three cases, however, households would have to service the regular loan instalments from their income. When interpreting the results, it should be noted that the survey was conducted prior to the turn of the cycle in the real estate market and, above all, before the sharp rise in interest rates on real estate loans in 2022. As a result, affordability problems because of higher interest rates are likely to have played a smaller role in households’ intention to buy at the time of the survey.

In case of a minimum equity requirement of 10%, households indicated an average purchase probability of 30%. Figure 1 shows that there is a strong concentration of households indicating either 0% or 100%. In this scenario, 48% definitely do not want to buy and 12% definitely do. If the lender does not require any equity, the average probability increases to 37%. The hypothetical inheritance covers not only the minimum required equity but also the transaction costs associated with the purchase, making it possible to buy a property without recourse to financial reserves. In this case, the average probability of purchase rises to just under 50%. At the same time, though, we still see a great deal of heterogeneity. For example, even in the inheritance scenario, more than 30% of households indicate a 0% probability of buying a property. These results show that higher equity requirements reduce the probability of purchase, but individual preferences or circumstances also play a decisive role.

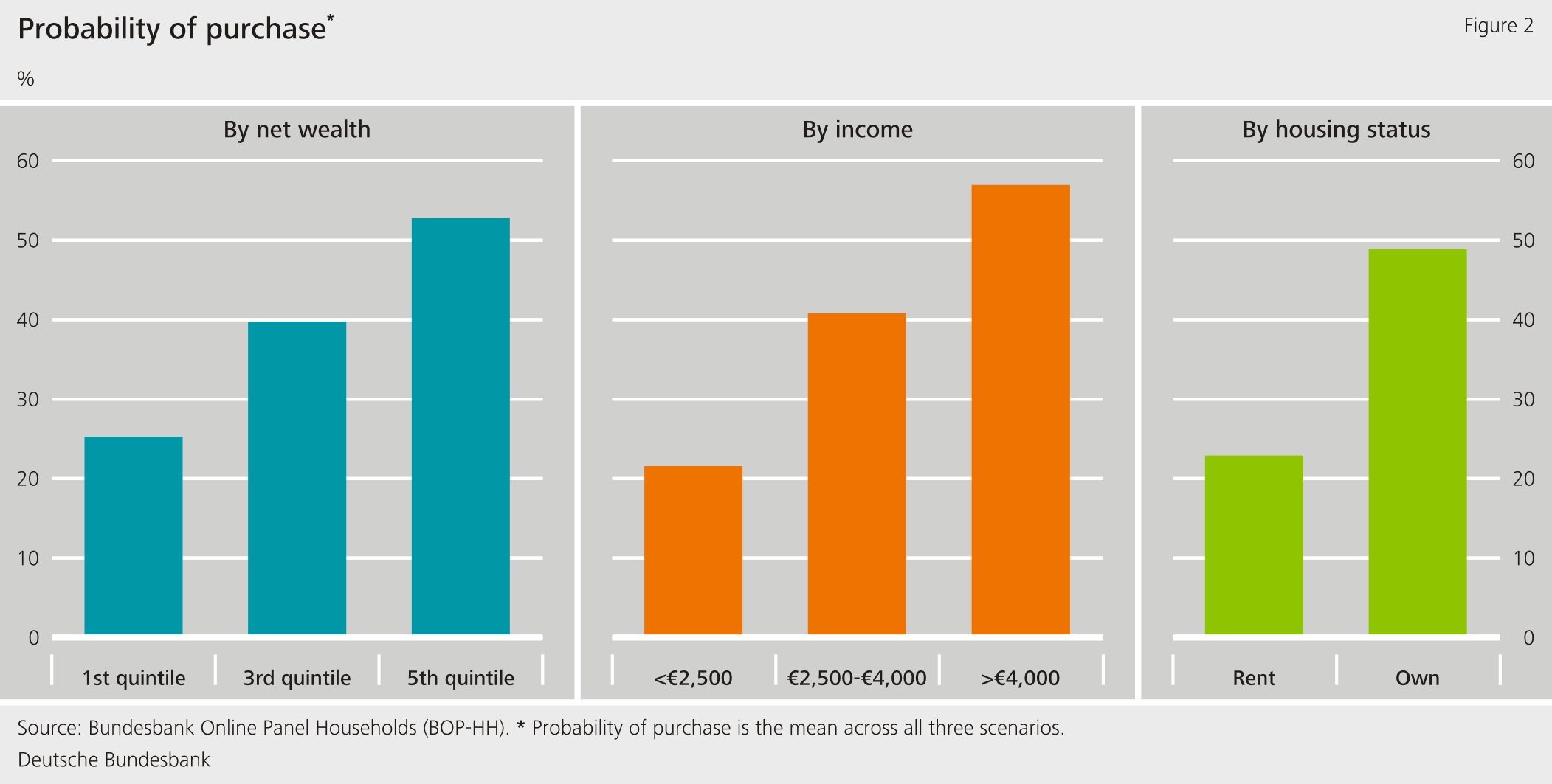

Households with little wealth, low income or renters generally indicate lower probabilities of buying (see Figure 2). This illustrates how crucial the financial situation of households is when making a decision to buy. Furthermore, we can show in detailed analyses that these groups’ purchasing probability responds much more strongly to changes in equity requirements.

Minimum equity requirements for borrowers lead to adjustments by households and reduce financial stability risks

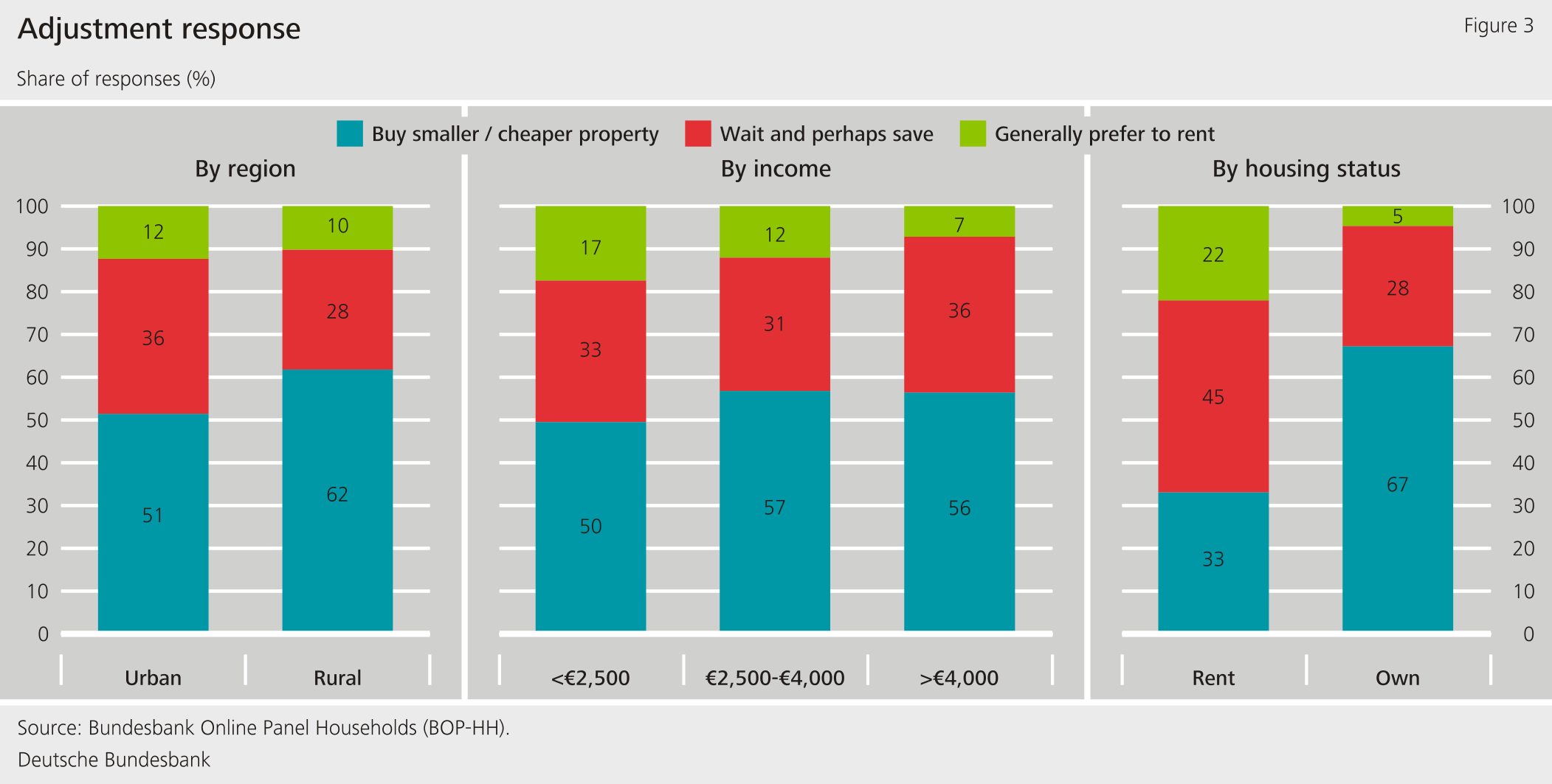

Minimum requirements need not preclude households from buying immediately or later on, however. A little over half of the respondents stated that they would reduce the amount of living space they sought or move to a cheaper area if faced with binding minimum requirements. One third would prefer to continue renting and save money for the time being. Only a little under 12% would generally prefer to rent, setting aside their intentions to buy. When subject to binding equity requirements, there is a tendency among households with greater wealth, higher income, homeowners or households in rural areas to immediately buy smaller or cheaper properties rather than saving and buying later (see Figure 3).

Above all, the higher equity and consequently lower debt of households reduce lenders’ losses in the event of default. In the survey, however, households were also asked to estimate the likelihood that they will be unable to service their debts over the next three months. Financially constrained households (financial assets of less than €50,000, more than €50,000 in debt, and monthly income below €4,000) indicate a lower probability of buying, but a higher probability of default (see Table 1). This is because such households are less likely to have the required equity, have less income and are therefore more financially vulnerable. As a result, minimum requirements could additionally help to reduce the probability of default of issued loans.

| Table 1: Self-estimated probability of purchase and default | ||

| Probability of purchase | Probability of default | |

| Constrained | 38% | 5% |

| Unconstrained | 49% | 1% |

Conclusion

Our analyses shed light on various effects of minimum equity requirements for borrowers, which have to be taken into account when weighing up costs and benefits of such requirements. On the one hand, higher requirements can reduce financial stability risks in a targeted way. On the other, they may prevent households from becoming homeowners. However, many households are willing to adjust their plans if they are affected by equity requirements. If this willingness to adjust is not taken into account, the negative impact of equity requirements on homeownership is overestimated, especially in the medium term.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

References

- Acolín, Arthur; Jesse Bricker, Paul Calem and Susan Wächter (2016). Borrowing Constraints and Homeownership, American Economic Review: Papers & Proceedings, 106(5).

- Alam, Zohair, Adrian Alter, Jesse Eiseman, Gaston Gelos, Heedon Kang, Machiko Narita, Erlend Nier and Naixi Wang (2019). Digging Deeper – Evidence on the Effects of Macroprudential Policies from a New Database, IMF Working Paper No. 2019/066.

- Araujo, Douglas Kiarelly Godoy, Joao Barata Ribeiro Blanco Barroso and Rodrigo Barbone Gonzalez (2020). Loan-to-value policy and housing finance: Effects on constrained borrowers, Journal of Financial Intermediation 42.

- Deutsche Bundesbank (2015). Financial Stability Review, pp. 79 ff.

- Deutsche Bundesbank (2022). Financial Stability Review, pp. 40 ff.

- Fuster, Andreas and Basit Zafar (2016). To Buy or Not to Buy: Consumer Constraints in the Housing Market, American Economic Review: Papers & Proceedings, 106(5).

- Tzur-Ilan, Nitzan (2017). The Effect of Credit Constraints on Housing Choices: The Case of LTV limit, Bank of Israel Working Papers 2017.03.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein