Transmission of interest rate hikes depends on the level of central bank reserves held by banks Research Brief | 61st edition – October 2023

Banks with substantial central bank reserves are earning income from their reserve holdings in the European Central Bank’s (ECB) recent rate hiking cycle. This could make their credit supply less sensitive to the monetary policy tightening compared to other banks. This hypothesis is examined in a new study (Fricke, Greppmair, Paludkiewicz, 2023) using the new AnaCredit dataset – a credit register harmonised across the euro area.

Novel situation: Interest rate hikes in an environment with large central bank reserves

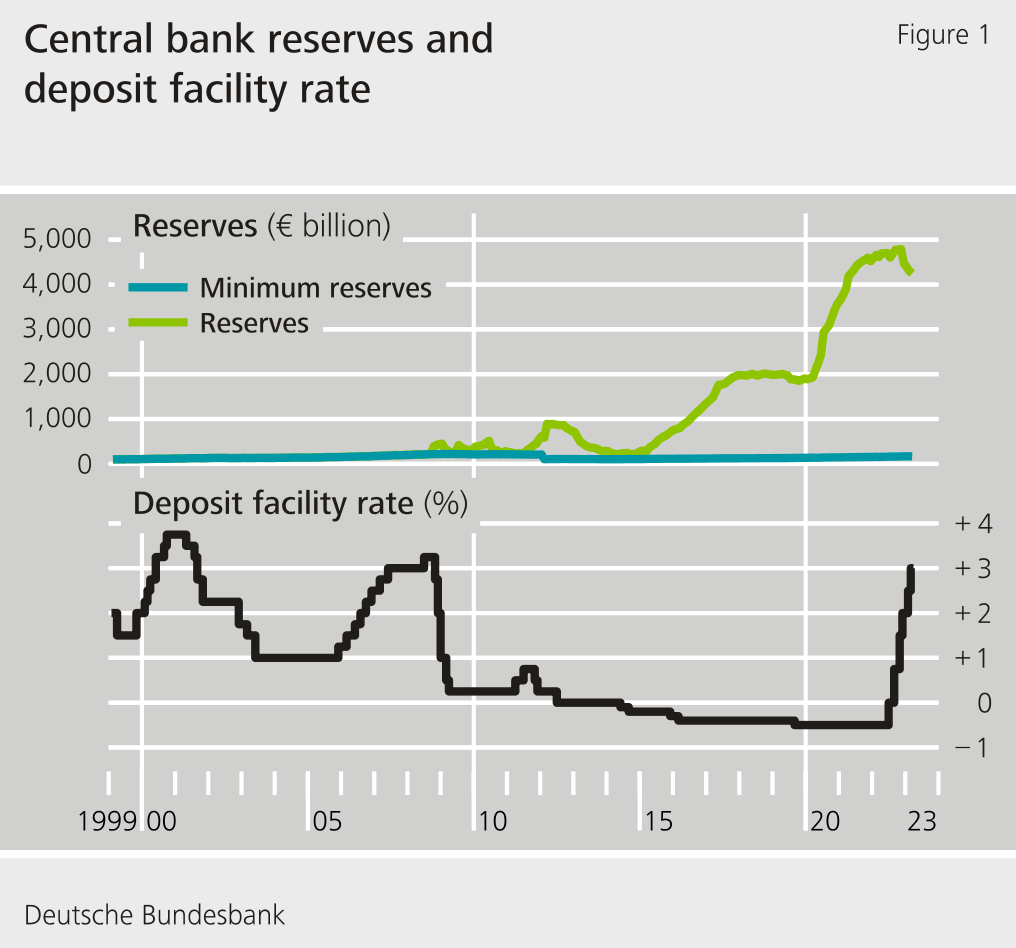

Since the second half of 2022, the Eurosystem has increased key interest rates significantly to curb inflation. The deposit facility rate, i.e. the interest rate banks receive when they hold deposits (reserves) with the central bank overnight, is shown in Figure 1 (black line). When this rate became negative in 2014, banks had to pay interest on their reserves. When this rate turned positive in September 2022, banks once again earned interest income from their reserve holdings. Compared with previous tightening cycles, it is striking that banks are holding substantial reserves with the Eurosystem in the current cycle. In June 2022, that is before the onset of the tightening cycle, total reserves held by euro area banks amounted to €4.7 trillion (see the green line in Figure 1), or 12.3 percent of their total assets. In 2008, this figure was only €0.1 trillion, or 0.75 percent of their total assets. This increase was driven, in particular, by non-standard monetary policy measures, such as the asset purchase programmes in the context of quantitative easing.

Central bank reserves are special in that they are the safest and most liquid assets available. Central banks largely determine the aggregate level of reserves, and unlike other assets, central bank reserves can only be held by banks - the traditional counterparties of central banks.

What impact could reserves have on bank lending?

In conjunction with the unprecedentedly large reserve holdings, the interest rate hikes mean that banks with substantial reserves are earning considerable interest income from their reserve holdings for the first time in the history of the Eurosystem. Taken in isolation, this could affect the balance sheet channel of monetary policy transmission, one of the most standard transmission channels of monetary policy. In this context, monetary policy affects banks’ lending decisions via their net worth. Due to banks’ maturity transformation interest rate increases (in an environment without substantial reserves) typically affect the market value of banks’ assets more strongly than their liabilities, thus reducing banks’ net worth. This can dampen their credit supply, in particular for banks with low capital ratios. In an environment with substantial reserves, however, the revaluation of bank assets could have a less significant impact on banks with a higher reserve ratio, as central bank reserves are, by nature, short-term assets. In addition, the cost of funding via liability-side counterparts rises less sharply if the interest rate increases are not fully passed on to bank depositors. Banks with higher reserve ratios, then earn additional interest income from holding reserves. When viewed in isolation, both effects could lead to a situation where large reserves may dampen the negative impact of monetary policy tightening on banks’ net worth and thus on lending. Moreover, the effect should be stronger for banks with low capital ratios, as balance sheet restrictions are more binding for these banks.

Empirical evaluation of over 40 million loans confirms differences in transmission depending on the size of banks’ reserves

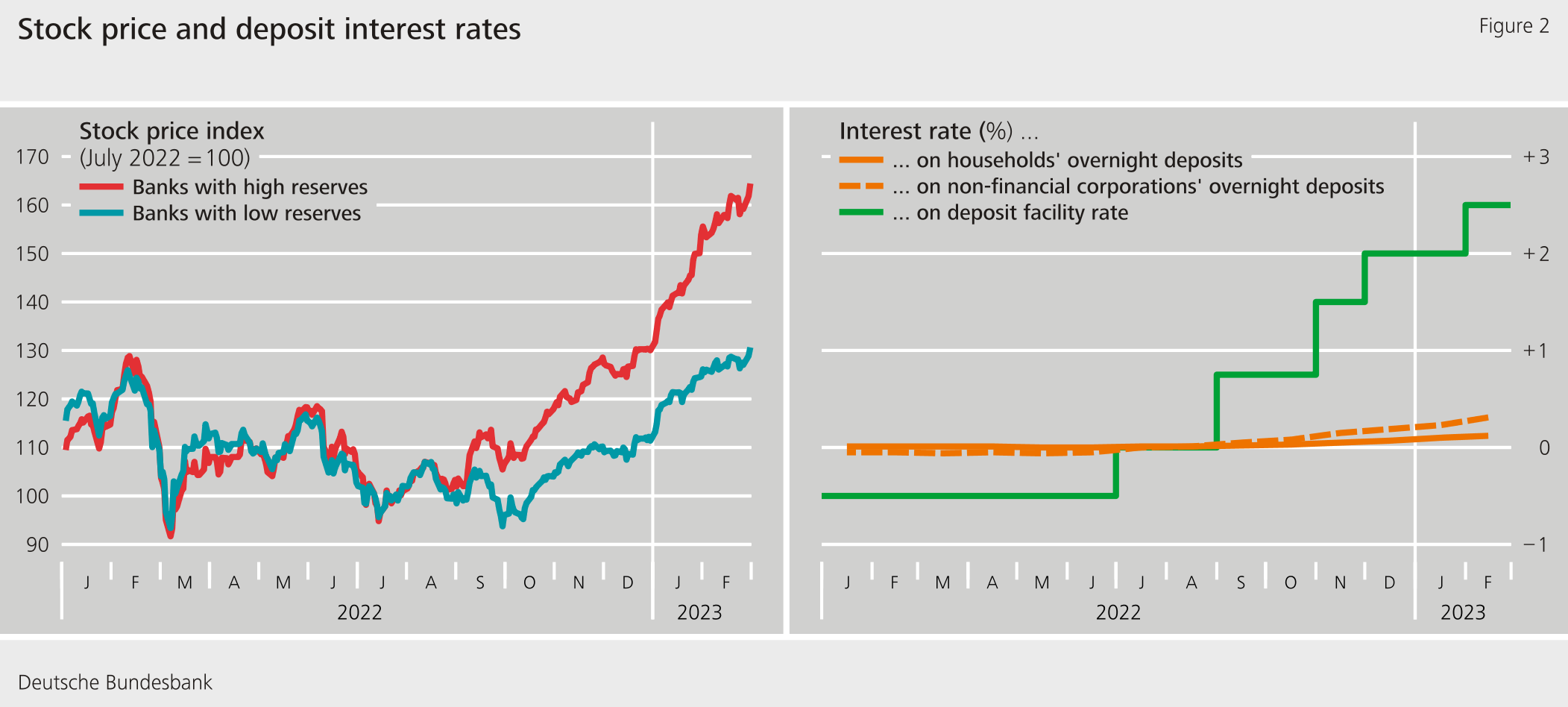

A new study (Fricke, Greppmair, Paludkiewicz, 2023) provides empirical evidence in line with this mechanism. First, the study documents that banks with higher reserves experience an increase in net worth. The left-hand chart in Figure 2 shows developments in stock prices of listed banks as a proxy for net worth, distinguishing between banks with high reserves (red line) and banks with low reserves (blue line). It can be seen that the stocks of banks with substantial reserves had significantly higher returns after the first interest rate hike in July 2022. In addition, it is evident that banks hardly passed on the interest rate hikes to their depositors. This is relevant because deposits are the most important source of funding for banks and thus the main liability counterpart to reserves. The development of the average bank interest rates on households’ and non-financial corporations’ overnight deposits is shown in the right-hand chart of Figure 2 (orange lines), along with the deposit facility rate (green line). While the deposit facility rate increased significantly, interest rates on overnight deposits increased only slightly.

Consequently, the positive effect on banks’ net worth should, all other things being equal, work against potential lending restrictions. More than 40 million loans granted by banks to non-financial corporations throughout the euro area have been analysed on the basis of the AnaCredit dataset. An econometric estimate can be employed, inter alia, to separate the credit supply (the subject of the study) from credit demand. The central finding is that the credit supply of banks with higher reserves reacts less strongly to interest rate hikes than the credit supply of other banks. This effect is also economically relevant. The effect is more pronounced among smaller banks and banks with lower equity ratios, reaching mainly smaller enterprises and enterprises with higher credit quality.

Conclusion

Banks with high reserves recorded an increase in net worth in the wake of the ECB’s recent tightening cycle. For these banks credit supply is less sensitive to the monetary policy tightening compared to other banks, especially for banks with low capital ratios. Monetary policymakers should take these findings into account.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

References

- D. Fricke, S. Greppmair, K. Paludkiewicz (2023), Excess Reserves and Monetary Policy Tightening, available on SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4432543

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein