TARGET Services

Promoting the smooth operation of payment systems is one of the basic tasks shared by the European System of Central Banks (see Articles 3 and 22 of the Statute of the European System of Central Banks and of the European Central Bank (Statute of the ESCB)) and the Deutsche Bundesbank. Section 3 of the Bundesbank Act (Gesetz über die Deutsche Bundesbank, BBankG) stipulates that the Bundesbank “shall arrange for the execution of domestic and cross-border payments and shall contribute to the stability of payment and clearing systems”.

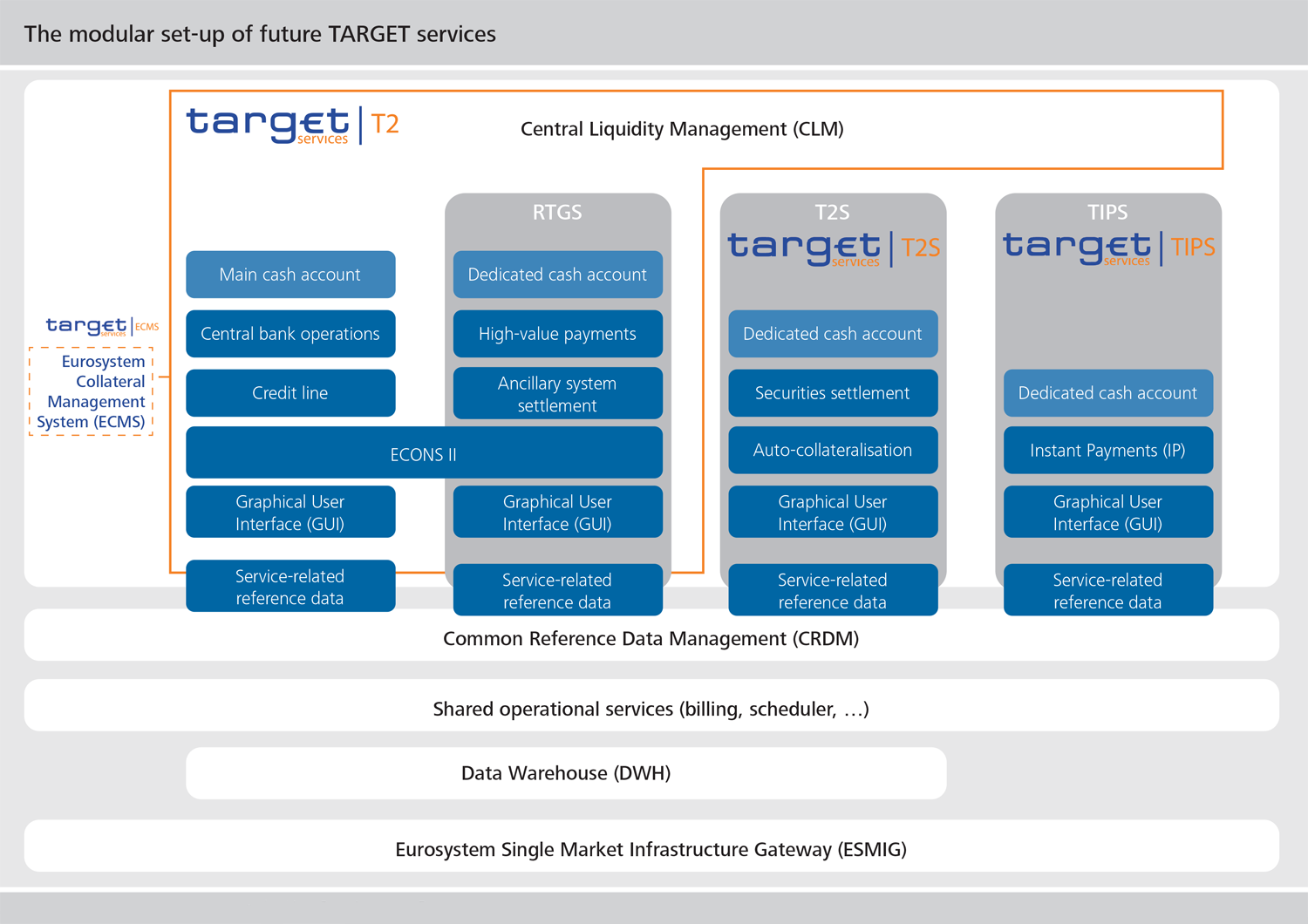

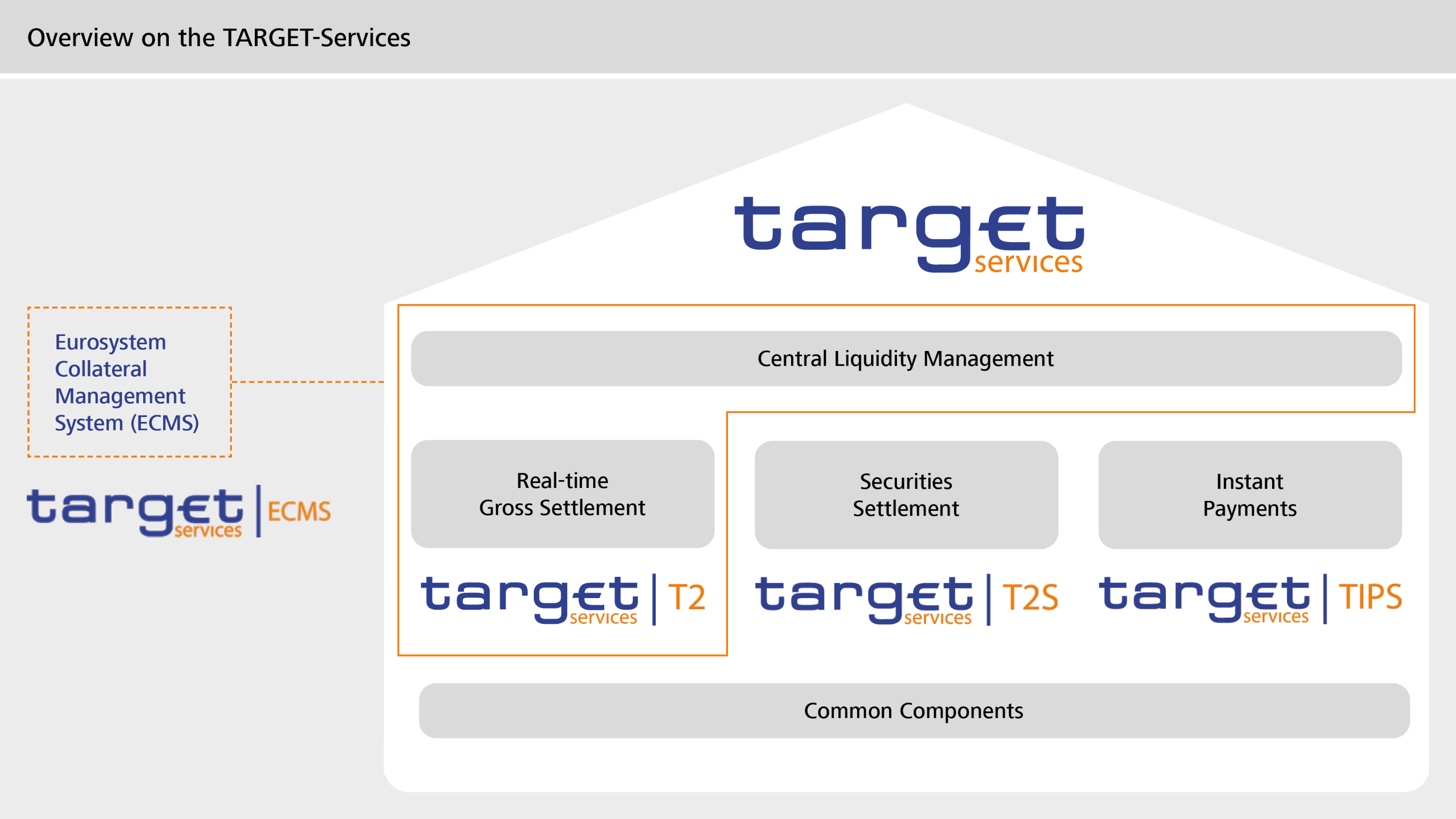

Moreover, the market infrastructures made available by the Eurosystem aim to further increase the integration of the European financial market. TARGET Services, also referred to all together as the TARGET family, serve this purpose. These services include T2 for the settlement of high-value and individual payments as well as the settlement of monetary policy operations, T2S (TARGET2-Securities) for securities settlement, and TIPS (TARGET Instant Payment Settlement) for the settlement of real-time transfers in retail payments. In future, TARGET Services will be complemented by the Eurosystem Collateral Management System (ECMS).

TARGET Services facilitate interaction between services. In this context, the Central Liquidity Management (CLM) module acts as a hub for the needs-based allocation of liquidity to the individual services. At the same time, all TARGET Services use the new ISO 20022 standard for communication, which has also been the global standard in correspondent banking since March 2023.