Bundesbank posts distributable profit of €5.9 billion in 2019

The Bundesbank posted a profit of €5.8 billion for the 2019 financial year. Following adjustment of the reserves, the Bank registered its highest distributable profit since 2008, at €5.9 billion, up from the previous year’s €2.4 billion. The Bundesbank has transferred the profit in full to the Federal Ministry of Finance. “Lower risk provisioning is the main reason for this strong rise in the profit for the year,” Bundesbank President Jens Weidmann explained at the press conference presenting the Bank’s annual accounts in Frankfurt am Main.

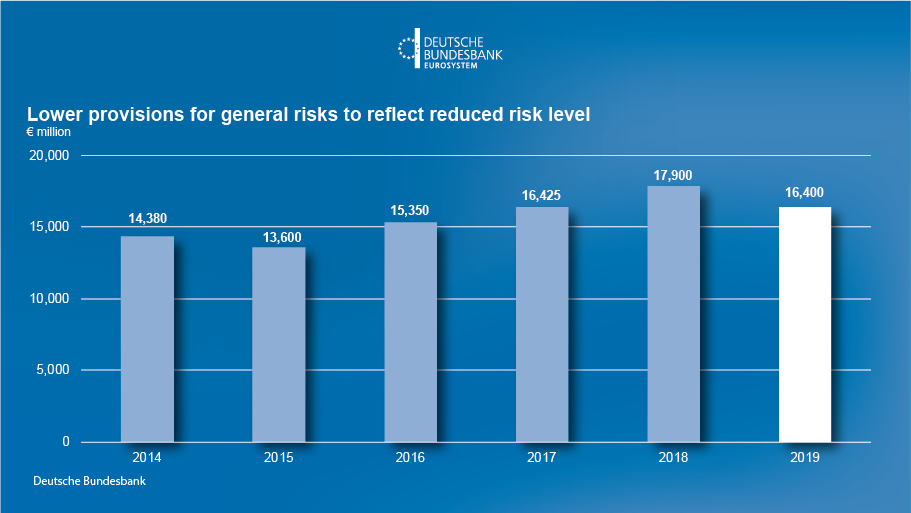

Having gradually stepped up its provisions for general risks between 2016 and 2018, the Bundesbank was now able to lower its provisioning levels by €1.5 billion to €16.4 billion. Lower interest rate risk and a drop in default risk made this reduction possible, Mr Weidmann said, acknowledging the role played by the variable remuneration on the new series of targeted longer-term refinancing operations and the maturing of assets purchased under the securities markets programme (SMP).

Interest income still high

As outlined in its Annual Report, the Bundesbank once again recorded high interest income from the negative remuneration of the balances held by credit institutions and other domestic and foreign depositors and from its securities holdings. Net interest income, however, was down slightly in 2019, mainly due to lower interest income from SMP assets on account of securities in the SMP portfolio reaching maturity. Net interest income – the most important component of the Bank’s profit – contracted from €4.9 billion to €4.6 billion.

Total assets down slightly – second-highest level in the Bank’s history

The Bundesbank’s total assets shrank slightly on the year to close the 2019 financial year at €1.78 trillion. “This means that the Bank still had the second-highest volume of total assets in its history at the end of 2019,” Johannes Beermann, the Executive Board member responsible for accounting and controlling, said at Friday’s press conference. Total assets reached their record level of €1.84 trillion at year-end 2018.

On the assets side, this decline in total assets was mainly driven by return flows of liquidity to other European countries. These flows reduced the TARGET2 claims on the ECB by €71 billion to €895 billion, after the previous year had seen this item increase by €59 billion to €966 billion. The main decline on the liabilities side was registered by the euro balances of domestic and foreign depositors, which shrank by €137 billion to €272 billion due, in particular, to a reduction in assets held by foreign central and commercial banks.

Uncertainties for the German economy

Mr Weidmann also used Friday’s press conference to discuss Germany’s economy. Last year had seen trade tensions unsettle the financial markets, he reported, and considerable uncertainties were still at play for the German economy, such as those affecting global trade. The spread of the coronavirus was an additional economic risk for Germany in the short run. “Based on the current information, I am expecting this risk to actually materialise to a degree,” he explained, adding that, as things stand today, it was almost impossible to gauge the effect reliably.

Central banks as catalysts for greening the financial system

Another talking point was the review of the ECB Governing Council’s monetary policy strategy. For Mr Weidmann, the key question is how the Governing Council can best deliver on its mandate, “which is to safeguard stable prices for people in the euro area”. It was clear, he reasoned, that the strategy should not be tailored to the consequences faced today. After all, it needs to provide long-term guidance. The strategy review will also address the role that central banks can play when it comes to climate action, he continued, stressing that “central banks can and should do more about climate change than they have up to now”. They need to factor climate-related financial risks into their risk management. It might be worth investigating how central banks could be catalysts for greening the financial system, in Mr Weidmann’s view, though preferential purchases of green bonds as a monetary policy tool were not the answer.