Bundesbank discussion paper explores inflation expectations in the euro area

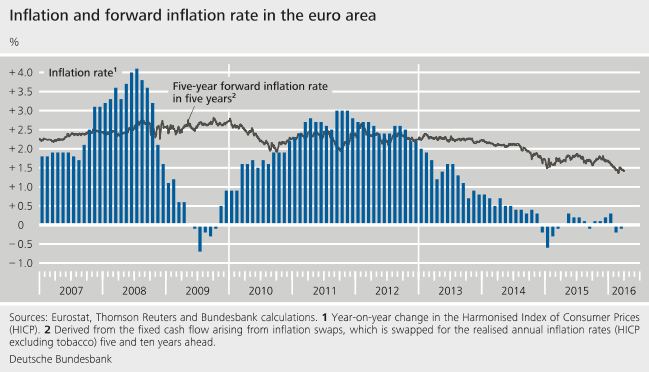

Since the end of 2014 inflation rates in the euro area have been hovering around the zero mark, which is less than the Eurosystem's medium-term target figure of "below, but close to 2%" and also down on the previously projected path. What is more, inflation expectations measured with the aid of financial market variables have diminished as well, raising the question of whether there are any grounds to believe that inflation expectations, in particular, are still anchored over a more distant horizon.

Long-term inflation expectations are a key variable for central banks, serving, as they do, as a crucial barometer for central bank credibility and monetary policy effectiveness. They reveal whether experts, the general public or market participants are confident that monetary policy is willing and able to again hit its price stability target, give or take some slight fluctuations.

This prompted the Bundesbank's Research Centre to draw up a discussion paper which investigates how market-based inflation expectations have responded to macroeconomic "surprises" since 2004. The finding enabled the author to explore whether, and in what way, market players have brought their expectations into line with the low realised inflation rates. A macroeconomic surprise is defined as a situation where a released indicator describing the current state of the economy, say, deviates quite substantially from the previous consensus expectations of market participants. For market participants, then, the release represents a new piece of information on the state of the economy, making it a "surprise".

Market-based inflation expectations are measured with the aid of inflation-linked swaps (ILSs), which are financial derivatives used to hedge inflation risk. ILSs indicate how agents operating in the markets see inflation and the attendant risks developing in the future. The fact that both short-term and long-term ILSs are traded in financial markets is a crucial asset for researchers, since by comparing ILS rates for different horizons, they can deduce whether market players have adjusted only their short-term inflation expectations in response to the "surprises" or whether they might have changed their long-term views as well.

The anchoring issue centres around long-term expectations. If the Eurosystem's monetary policy objective is not firmly anchored, the public at large and investors might change their view of the inflation rate targeted by the central bank depending on the prevailing economic situation. Were that the case, their long-term inflation expectations would respond to economic surprises as well. If, on the other hand, market players expect the Eurosystem to be willing and able to hit its inflation target within a given horizon, they will also believe that economic fluctuations in the short run will even out over time. Hence, long-term expectations derived from swap rates should not respond to macroeconomic surprises as long as inflation expectations are anchored.

"Inflation expectations responded more readily to macroeconomic news following the outbreak of the financial crisis than prior to it,"

the author notes, conceding that this primarily concerns shorter forecast horizons, though these do also reflect the economic cycle or commodity price developments. Summing up his results, the author writes: "Medium-term expectations normally respond little to macroeconomic news and may still be considered firmly anchored."

He did, however, identify two periods in which medium-term inflation expectations had indeed responded to macroeconomic news. "First, in 2009, a surprisingly strong recession led to a sharp decline in the inflation rate, which is taking longer than usual to return to its target,"

he notes; "second, in February 2015, higher than expected inflation led to a rise in medium-term inflation expectations toward the [Eurosystem's] inflation target"

. By contrast, the author adds, the surprising decline in inflation seen in 2013 and 2014 has not impacted significantly on medium-term inflation expectations.

The discussion paper explains how inflation expectations over very distant forecast horizons remain consistently insensitive to economic surprises. "The response of medium-term inflation expectations is therefore a sign of a protracted phase of inflation adjustment towards the Eurosystem's inflation target and should not be interpreted as a de-anchoring of inflation expectations or a credibility problem on the part of the Eurosystem,"

the author concludes.

This discussion paper was prepared by the Deutsche Bundesbank's Research Centre. It was authored by Christian Speck. The opinions expressed in the paper do not necessarily reflect those of the Bundesbank or its employees.