Monthly Report: digital money a source of both opportunities and risks

The world of cashless payments is becoming ever more digital, particularly so since the onset of the COVID-19 pandemic, which has boosted the uptake of non-cash transactions, according to a Bundesbank study. Key drivers of the digitalisation trend include not just contactless payments at the point of sale but also the increasing availability of digital payment solutions in online commerce, especially those offered by global card systems and new providers like fintech and bigtech firms. The emergence of state-of-the-art techniques, above all distributed ledger technology (DLT), is another important factor. These support new forms of digital money that can be sent across decentralised networks and used by protocols known as smart contracts as payment instruments in programmable applications.

Fintech businesses cooperate with market incumbents and offer new technical solutions that give bank customers the option of managing their accounts, viewing their account balance or sending money by smartphone. Bigtech firms – technology or data-driven platform providers with a large customer base – offer payment solutions of their own, and some are even planning to roll out their own stablecoins. These include Facebook’s Diem stablecoin system, previously known as Libra. Bigtech firms and international card systems, using dedicated apps as a digital interface, are likely to become increasingly important for customers. This growing reliance on non-European infrastructure in the European market for payment services has led to a situation where payments is increasingly being regarded in political circles as a strategically important sector for European sovereignty. |

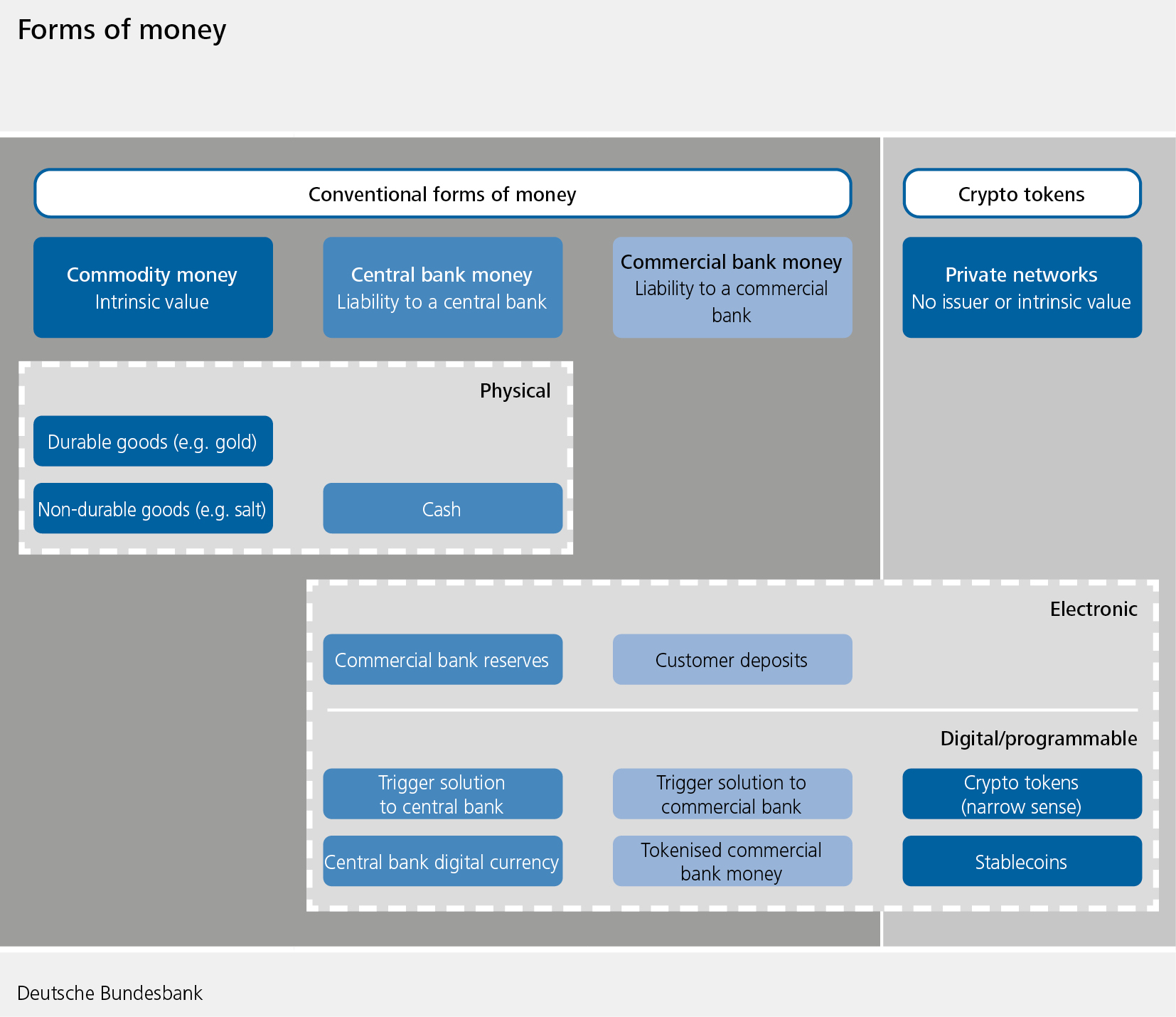

Central bank money in digital form

Digital money is also high on the agenda at central banks, which are regarding trigger solutions (see link below), digital central bank currency for a limited set of users (wholesale CBDC) and digital central bank currency for the general public (retail CBDC) as conceivable options. Debate in the euro area is centred around the possible development of a digital euro, which was the subject of a Eurosystem report in October 2020. According to this report, the digital euro would be offered for use by the general public and also be available for simple payment transactions. Consumers would thus have access to central bank money not only as cash but in digital form as well. The digital euro would be introduced alongside cash, complementing rather than replacing it. The Governing Council of the European Central Bank (ECB) is expected to decide whether to launch an investigation towards mid-2021.

A quick and convenient means of payment

What opportunities and risks would this possible new form of euro present? The primary focus should be to strike a sensible balance between the benefits of widespread usability and its risks, the Bank’s experts write in the Monthly Report. From a user perspective, it is important for a means of payment to be quick and straightforward in order to achieve wide acceptance. Programmability plays a special role in this regard. A digital euro should be useable not just in conventional payment situations, such as at the point of sale or in online commerce, but ideally offline as well, using wearable devices like smartwatches or bracelets. The innovative benefits of a digital euro would particularly come to the fore if it were programmable, which would allow it to be integrated into DLT-based processes with a minimum of friction. That would support functions such as fully automated billing and settlement between devices. For instance, an electronic vehicle could independently charge its battery and pay the charging station at the car park, or it would be possible to directly pay an amount of money depending on consumption or use. However, digital central bank money presents a number of risks as well, the experts warn. One is that the large-scale replacement of commercial bank money by CBDC could impact on monetary policy and financial stability and reduce the importance of banks as intermediaries in the financial system. Banks and financial service providers might be crowded out of the market and thus also offer less innovative products. The Bank’s experts therefore recommend that the banking industry be involved from the outset in discussions surrounding the potential design of a digital euro so as not to risk squandering the benefits offered by the existing division of tasks between commercial and central banks.

Data protection particularly important

The experts go on to stress that the digital euro cannot fully replace all of the functions and advantages of cash. One such upside of cash is that transactions are totally anonymous. Transfers of digital money, on the other hand, are always logged in an electronic register to prevent it from being copied and used multiple times. A public consultation by the ECB recently showed that data protection is particularly important for the general public and experts. What respondents want most from a digital currency is privacy (43%), followed by security (18%), usability across the euro area (11%), the absence of additional costs (9%) and offline use (8%). The Bank’s experts wrap up their article by stating that any solutions will need to be well-designed, secure and convenient. “Otherwise, neither the ambitious political expectations for a digital euro as an alternative to private sector stablecoins, nor the simultaneous responsibility of the central bank for the stability and maintenance of the market-based functioning of the financial system can be met,”

they conclude.