April results of the Bank Lending Survey (BLS) in Germany

- The real economic consequences of the COVID-19 pandemic and uncertainty surrounding future developments are making themselves felt in Germany both in banks’ lending policies and in demand for credit,

- with the German banks responding to the Bank Lending Survey (BLS) tightening their lending policies in all surveyed credit segments in the first quarter of 2020.

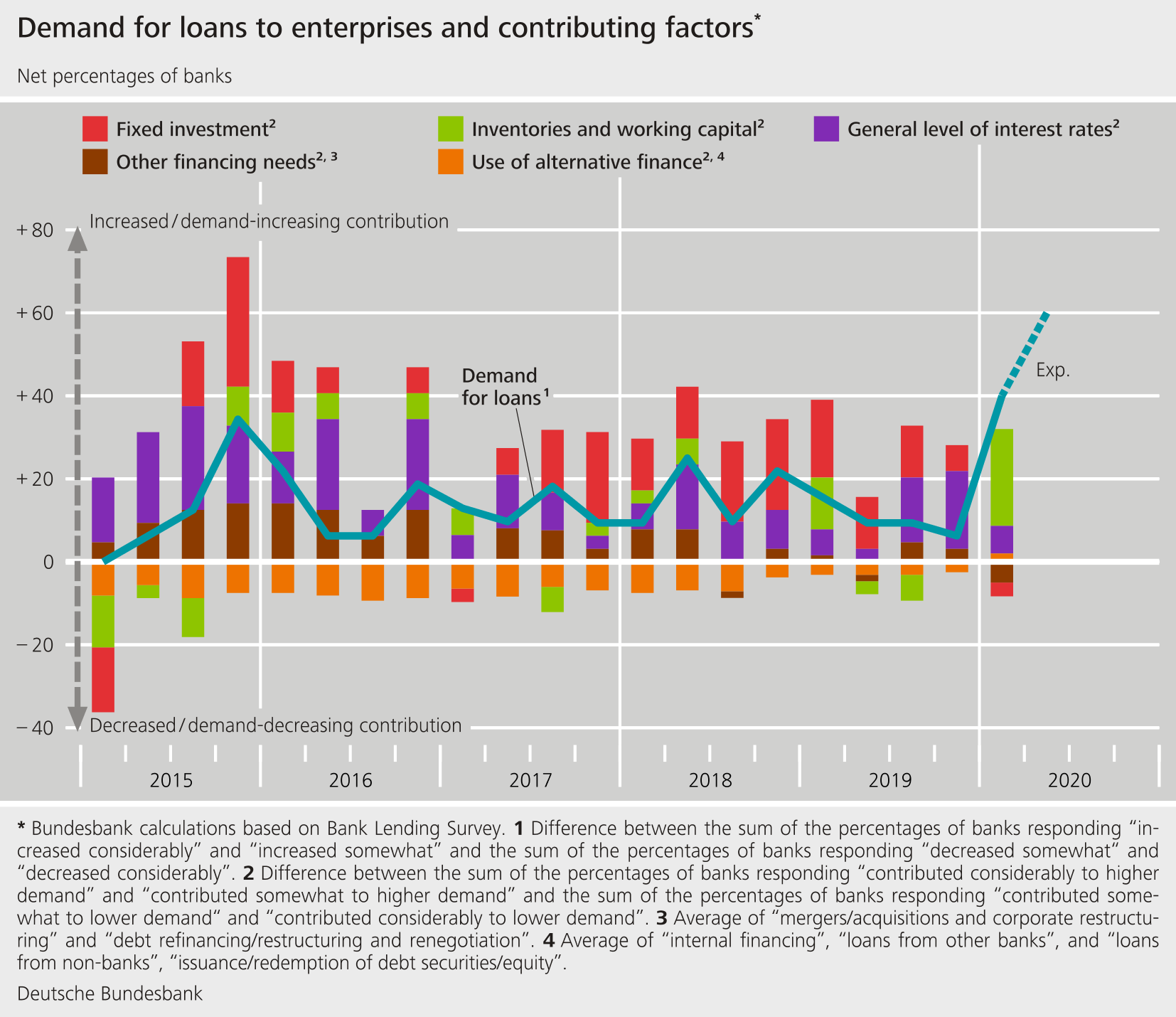

- In addition, demand for loans to enterprises requiring additional funding in order to bridge liquidity shortfalls rose considerably. Demand for loans, especially that of small and medium-sized enterprises for short-term lending, is set to increase even more sharply in the second quarter.

- The Eurosystem’s expanded asset purchase programme (APP) again weighed on banks’ earnings. Alongside the hit to profits, banks are expecting an improvement in their liquidity position owing to the APP and the pandemic emergency purchase programme (PEPP) in the coming six months.

- The negative interest rate on the deposit facility once again contributed to a decline in banks' net interest income. The two-tier system for remunerating excess liquidity holdings, meanwhile, impacted positively on net interest income.

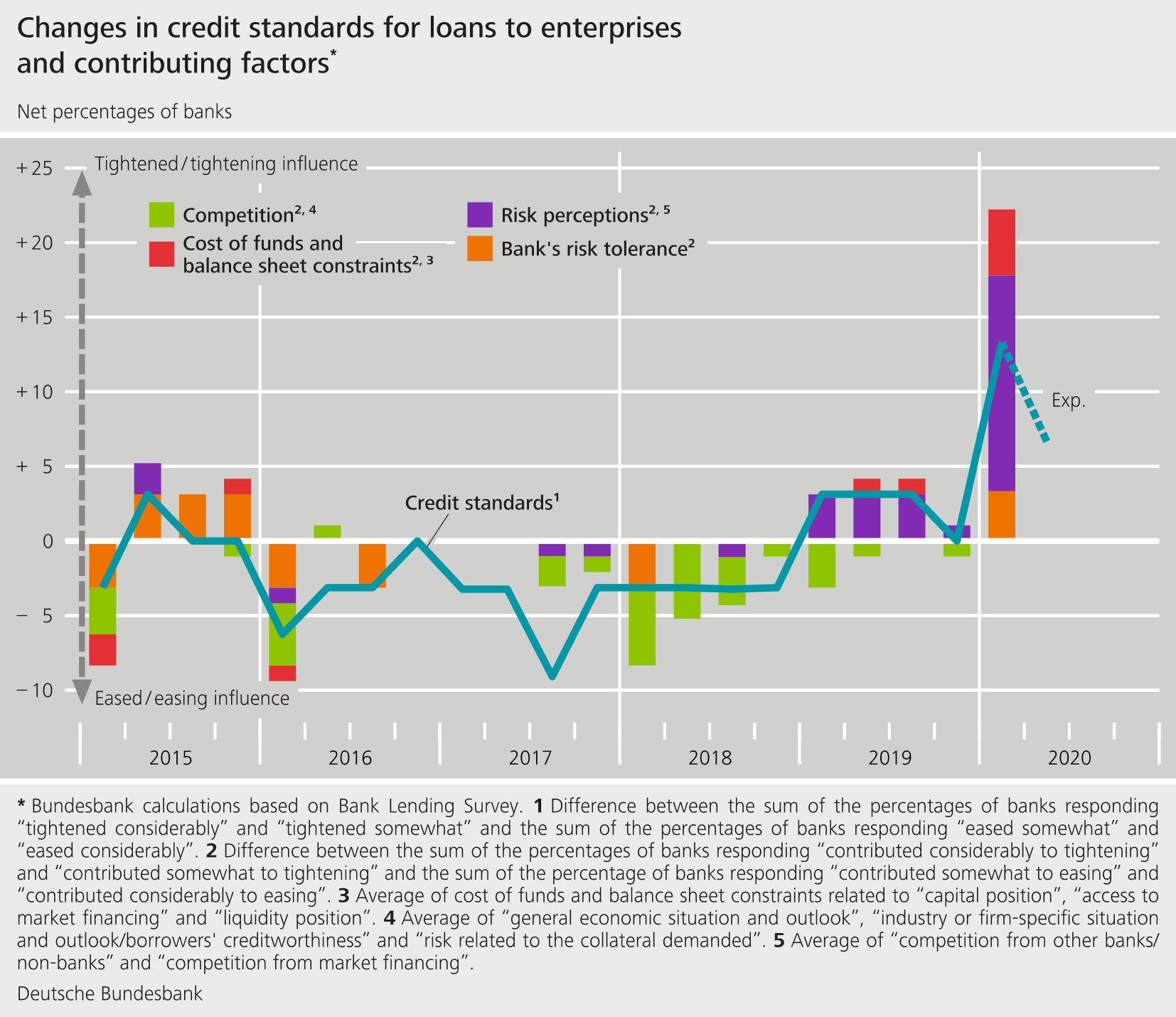

The BLS covers three loan categories: loans to enterprises, loans to household for house purchase, and consumer credit and other lending to households. The surveyed banks tightened their credit standards (i.e. their internal guidelines or loan approval criteria) for loans to enterprises (a net percentage of +13 %), especially loans to large enterprises. Credit standards for consumer credit and other lending to households (a net percentage of +10 %) and for loans to households for house purchase (a net percentage of +3 %) were tightened as well. The banks are planning to tighten their standards further in all surveyed segments over the coming three months.

{kind=link}

{kind=link}

The banks stated that demand for credit increased sharply in all surveyed lines of business, with demand for loans from firms needing more funding in order to bridge liquidity gaps rising considerably. The greater demand for loans to households for house purchase, however, was due primarily to the low general level of interest rates. The key driver of growth in consumer credit and other lending to households was an increase in the propensity to purchase consumer durables. For the coming three months, the banks are expecting an even stronger expansion in demand for loans to enterprises, especially from small and medium-sized enterprises looking for short-term credit and a sharp collapse in demand for loans to households for house purchase. The banks are expecting a further increase in consumer credit and other lending as well. This could well be because demand for liquidity assistance among the self-employed is likely to increase.

The April survey contained ad hoc questions on banks’ funding conditions and on the impact of the Eurosystem’s expanded APP, including the PEPP. In addition, it asked about the effects of the negative interest rate on the Eurosystem’s deposit facility. In this round, this question was augmented for the first time by a question on the impact of the two-tier system for remunerating excess liquidity holdings. For the second time, the survey contained questions on the Eurosystem’s targeted longer-term refinancing operations III (TLTRO III).

Against the backdrop of conditions in financial markets, German banks reported a deterioration in their funding situation compared with the previous quarter. The Eurosystem’s expanded APP continued to weigh on banks’ earnings through weaker net interest income. However, in the banks' assessment, the burden was less heavy than in the previous survey round. The APP had a positive impact only on the credit volume for loans for house purchase. The banks are expecting the APP and PEPP to lead to a significant improvement in their liquidity position and market financing conditions in the coming six months. The negative deposit facility rate once again contributed to a decline in banks’ net interest income, in part through lower lending rates. The negative earnings effect, however, was tempered by the two-tier system of remunerating excess liquidity holdings. At the same time, the lending volume rose once again in all credit segments, viewed in isolation. Three banks from the German sample took part in the TLTRO III in March 2020, mainly out of profitability considerations. The banks reported using the uptake in funds primarily for lending and liquidity holding in the Eurosystem. They would participate in future operations primarily owing to the attractive design of the TLTRO III and in order to avoid future funding constraints. The TLTRO III had no impact on banks’ lending policy.

The Bank Lending Survey, which is conducted four times a year, took place between 19 March and 3 April 2020. In Germany, 34 banks took part in the survey. The response rate was 94 %.