Germany’s foreign direct investment stocks at the end of 2024

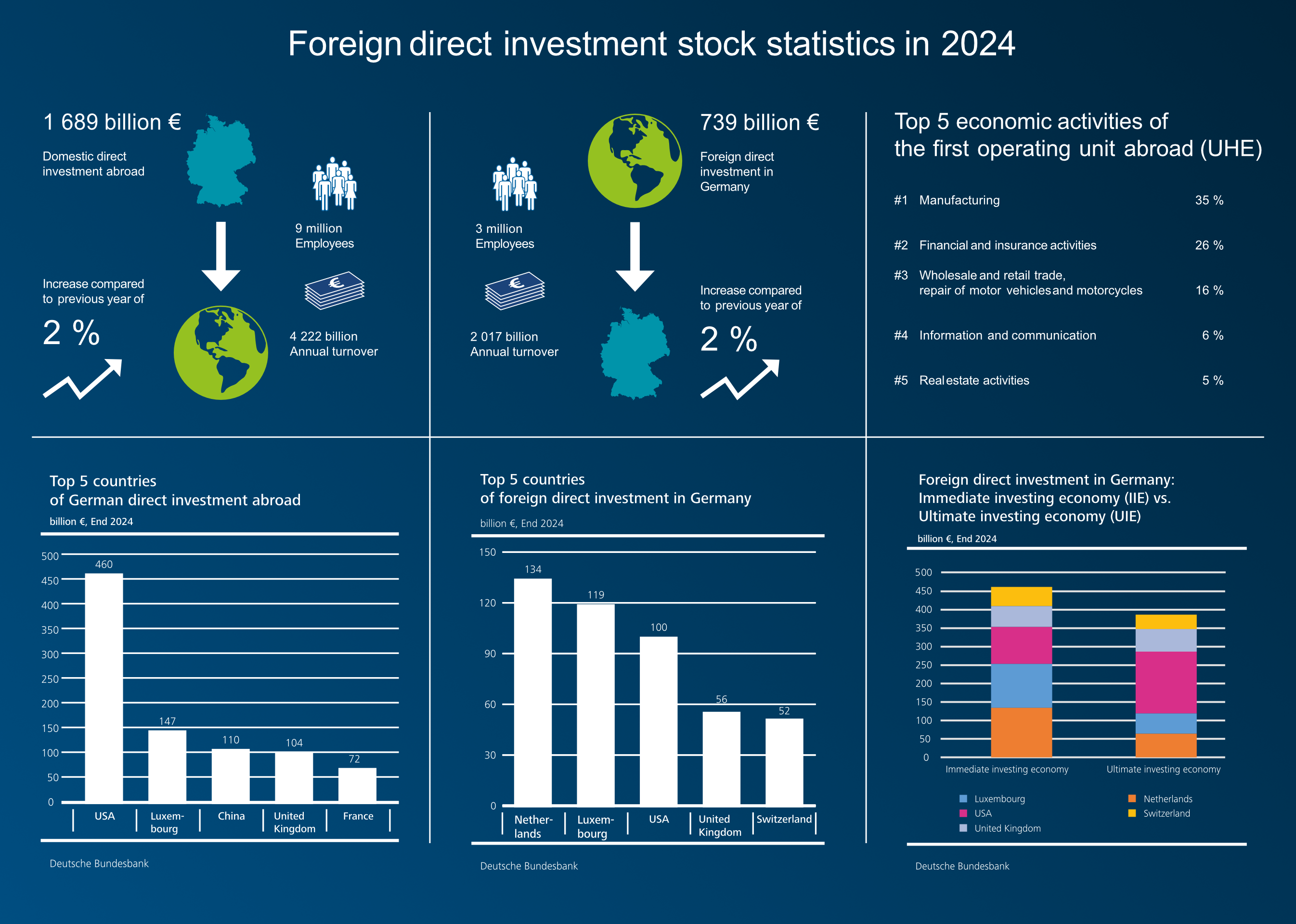

A better view of the regions and economic sectors that are actually targeted by the FDI can be obtained by looking through foreign holding companies in the ownership chain (ultimate host economy, UHE). In this consolidated view, outward German FDI amounted to €1,689 billion. A regional breakdown shows that half of Germany’s total outward FDI (€857 billion) remained in Europe, with €645 billion of that amount being attributable to EU countries. America followed in second place, at €560 billion, or one-third of stocks. More than €460 billion was invested in the United States alone. At €234 billion, Asia ranked a distant third, with 14 % of German outward FDI; after more than ten years of growth, German enterprises’ direct investment in China now declined for the second year in a row, from €115 billion in 2023 to €110 billion in 2024.

Across all target countries, consolidated German outward FDI (in the first operating unit by economic sector) was directed primarily towards manufacturing (€587 billion) and financial and insurance activities (€439 billion). By comparison, looking at FDI by economic sector only, the bulk of the stocks, at 60 % or €1,046 billion, was accounted for by holding companies (with and without a management function), a perspective which obscures the actual purpose of the FDI.

Inward FDI by immediate investing economy (IIE) likewise only edged up slightly by 2 % compared to end-2023, from €1,018 billion to €1,034 billion. Of this, €828 billion (+ €11 billion) stemmed from equity capital and €205 billion (+ €5 billion) from the balance of foreign loans.

Holding companies were responsible for around two-thirds (€679 billion) of inward FDI stocks overall. Here again, the consolidated data provide a better view of the domestic economic sectors that were actually targeted by the FDI (in the first operational unit). This resulted in a stock of inward FDI of €739 billion, of which €263 billion was accounted for by the financial and insurance activities sector and €169 billion by the manufacturing sector.

Tracing the ownership chain to its source and thus to the economy of the ultimate controlling parent (UCP), the ultimate investing economies (UIEs) shift – markedly in some cases – in terms of their importance for inward FDI in Germany. Viewed from this perspective, the United States ranked as the most important UIE, while stocks from the Netherlands and Luxembourg – traditional holding locations that are mainly used as “pass-through” countries for capital – more than halved.

In the same analysis (UIE), the picture for FDI in Germany was similar to that for Germany’s outward FDI, although the share of European countries was even more significant here, accounting for €471 billion and thus 64 % of the total stock of inward FDI in Germany. The EU was responsible for €355 billion of this amount. At €177 billion, stocks of FDI in Germany from America amounted to just under one-quarter of the aggregate, with €167 billion coming from the United States. Asia ranked third here as well, accounting for 12 % of FDI, equal to stocks of €86 billion. €10 billion of this figure was attributable to China.