Cash payments more popular in Germany than in other countries Research Brief | 1st edition – February 2016

By international standards, cash continues to be a very popular means of payment in Germany. Even for larger purchases, customers in Germany tend to use cash more frequently than those in other countries. A new study provides indications of the reasons behind this behaviour.

For several years now, people have been predicting the imminent end of cash. In view of historically low interest rates and current debates surrounding monetary policy, some academics have even advocated for the abolition of cash. Nevertheless, coins and notes have remained very popular.

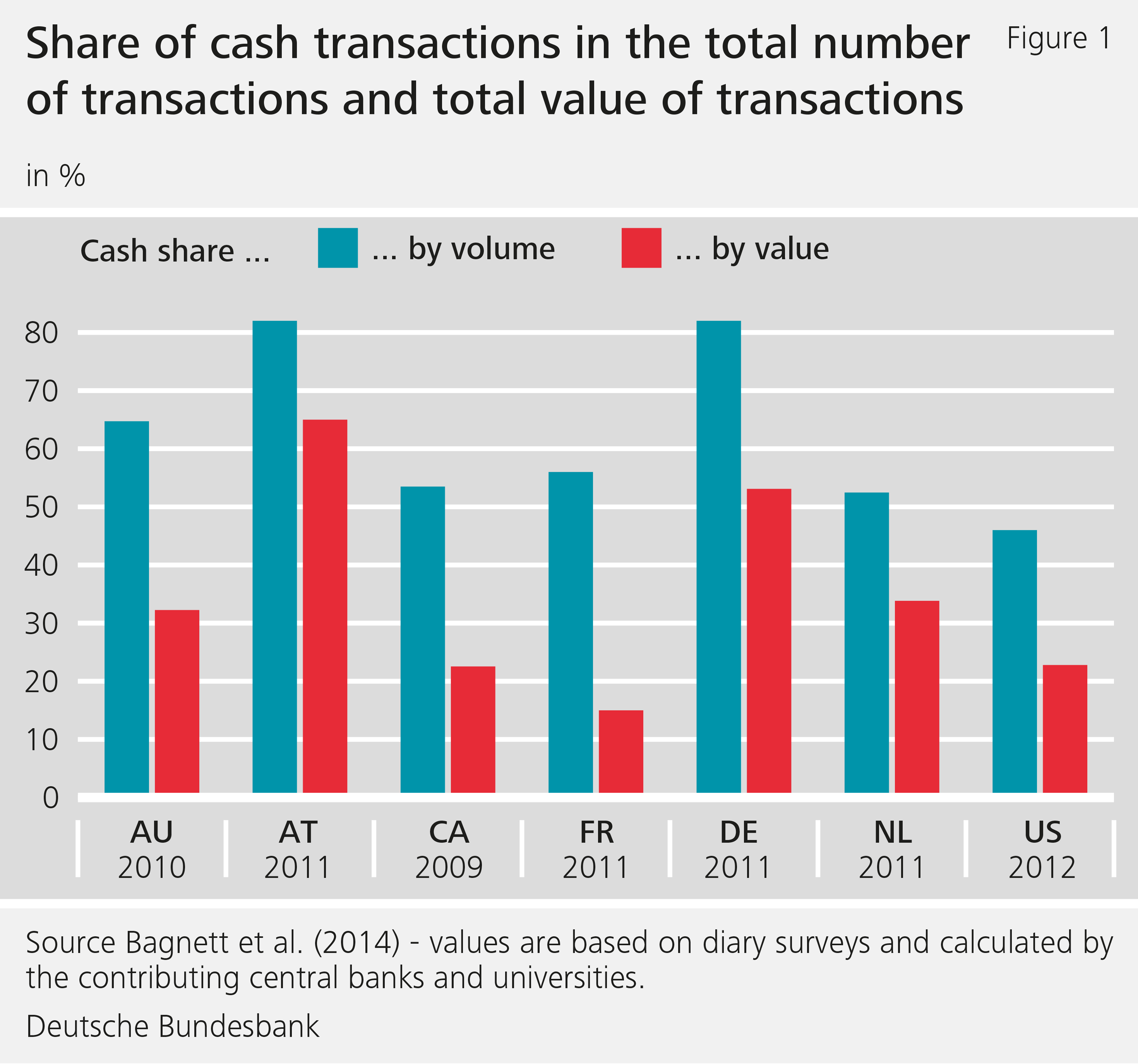

This is confirmed by a new study in which my colleagues and I have analysed internationally comparable data from payments diaries kept between 2009 (Canada) and 2012 (United States). More than 18,500 consumers in Australia, Austria, Canada, France, Germany, the Netherlands, and the United States kept a written record of their payments over a period of between one day and one week, also taking note of what payment methods they used. The dataset comprises a total of 103,000 payments. The results of the analysis show that customers still frequently opt for cash at the point of sale in all countries studied. In terms of volume, cash accounts for more than 50% of payment transactions in all of these countries, with the exception of the United States.

In most of the countries, consumers mainly use cash for smaller transaction amounts of less than 10 euro or 10 dollars. In Germany, however, almost 40% of larger purchases with values equivalent to more than 40 US dollars are made in cash. By way of comparison, this figure is less than 20% in the United States.

Thus, clear differences exist between Germany and most of the other countries in terms of how intensively cash is used by consumers. Our study looks into these differences and describes possible factors which may help to explain them.

Socio-demographic and structural differences

First, socio-demographic factors, such as the consumers' age or highest level of education attained – for instance, older persons tend to favor cash payments – impact on currency usage. This means that country-specific differences in these characteristics can partly explain the differences in payment habits from one country to another. However, the variance in cash usage between Germany and other countries is too large for socio-demographic characteristics to be the only explanation.

Second, payment locations and transaction purposes vary across countries. In France, for example, a higher percentage of expenditure goes towards food products, which are typically paid for in cash, than in most of the other countries. However, these factors only explain a small fraction of the country-specific differences.

Third, even "classic factors" (see Baumol, 1952, and Tobin, 1956) such as those referred to as "shoe leather costs" where even walking to the ATM costs time and effort, for example, differ across countries. Other opportunity costs of holding cash, such as interest rates, also vary from country to country. However, these differences do not display a unique pattern that can be directly linked to cash use.

Trading, conventions and reward programmes

Fourth, merchant behaviour is also important. For example, (retail) traders' acceptance of cashless payment instruments such as debit or credit cards at the point of sale is quite low in Germany compared with the other countries. Our study finds that for large-value amounts in particular, the share of cash transactions would be lower in Germany if cards were a more commonly accepted means of payment.

Fifth, other factors such as the social conventions and culture of a particular country might also play a role. In order to test this hypothesis, we looked at how high the respective shares of the individual payment instruments were at filling stations in the various countries. This payment behaviour is of particular interest, as cards are readily accepted at filling stations in all of the countries studied and the respective transactions are of approximately the same value. However, even in this instance, we found that Germans pay with cash much more frequently than consumers in the other countries.

Another possible factor is the use of reward programmes to make card use more attractive, or additional fees which make certain payment instruments less attractive. There is some evidence that incentives for using a particular payment instrument are able to steer consumers' payment behaviour (see, for example, Bolt et al, 2010, and Ching und Hayashi, 2010). Card providers, banks and retail organisations in some countries such as Australia, Canada, France and the Netherlands, have launched nationwide campaigns to promote card payments (Jonker et al, 2015). In Germany, on the other hand, card reward programmes and marketing activities are used much less to influence payment behaviour. This is one reason that might partly explain the differences in cash usage.

Conclusion

Our study identifies a number of factors related to cash usage, including socio-demographic characteristics, size and type of payment, and merchant behaviour. Even if all of these factors are taken into account, differences between Germany and the other countries studied, with the exception of Austria, still exist with regard to the use of cash. Why Germans have a clear preference for cash therefore remains a topic for further research.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- J Bagnall, D Bounie, K P Huynh, A Kosse, T Schmidt, S D Schuh and H Stix (2015), Consumer cash usage: a cross-country comparison with payment diary survey data, Deutsche Bundesbank Discussion Paper, No 13/2014, Frankfurt am Main, forthcoming in the International Journal of Central Banking.

- W J Baumol (1952), The transaction demand for cash: an inventory theoretic approach, Quarterly Journal of Economics, Vol 66, No 3, pp 545 – 556.

- W Bolt, N Jonker and C van Renselaar (2010), Incentives at the counter: an empirical analysis of surcharging card payments and payment behaviour in the Netherlands, Journal of Banking and Finance, Vol 34, No 8, pp 1738 – 1744.

- A T Ching and F Hayashi (2010), Payment card rewards programs and consumer payment choice, Journal of Banking and Finance, Vol 34 , No 8, pp 1773 – 1787.

- N Jonker, M Plooij and J Verburg (2015), Does a public campaign influence debit card usage? Evidence from the Netherlands, De Nederlandsche Bank, Working Paper 470, Amsterdam.

- J Tobin (1956), The interest elasticity of transactions demand for cash, Review of Economics and Statistics, Vol 38, No 3, pp 241 – 247.

| The author |

© Bert Bostelmann

Research Economist in the Household Finance Team at the Research Centre of the Bundesbank |

{kind=link}

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein