Why world trade collapsed during the financial and economic crisis Research Brief | 7th edition – October 2016

World trade suffered a marked decline during the financial and economic crisis which started in 2008, even more so than global economic output. A new study investigates what factors can explain the changes in world trade since 2000.

World trade in goods and services collapsed very markedly in 2009, even more so than global economic output. This is referred to in the literature as the great trade collapse. In a new study, we investigate the key factors behind this.

Trade can be analysed in two ways. The first is on the basis of gross trade flows, although this can produce biases on account of imported foreign value added in the form of intermediate inputs and the resulting multiple counting (Koopman, Wang and Wei, 2014). One alternative thus consists in value-added-based measures of foreign trade, which circumvent this problem and allow a more nuanced picture of world trade and the factors driving it. They show to which countries the value added of an end product can actually be attributed. In comparison, they are thus better suited to assessing countries' price competitiveness, trade imbalances and labour market effects of foreign trade.

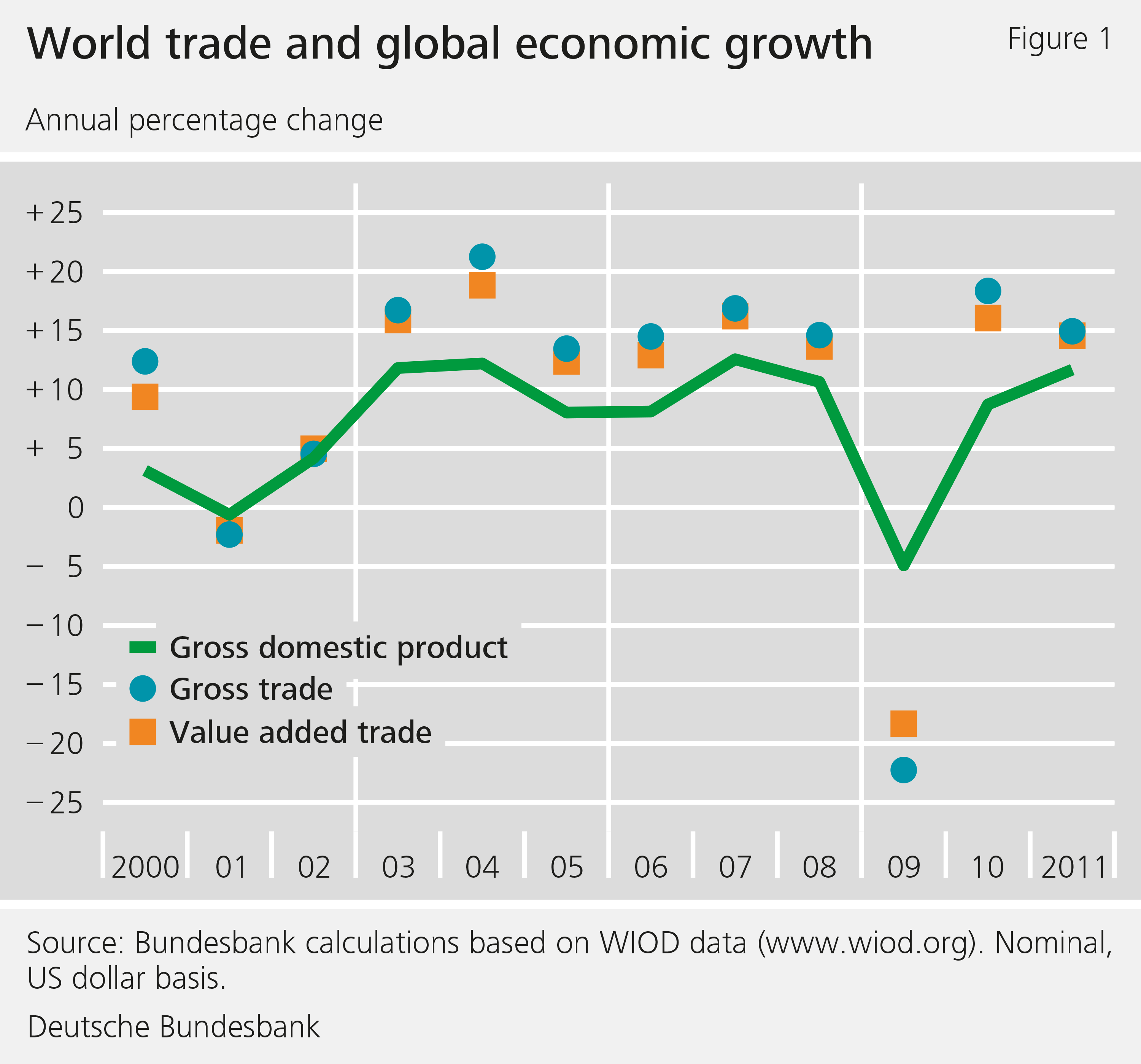

Figure 1 clearly shows that world trade declined in 2009, both in terms of gross trade flows and according to value-added-based measures. While global nominal GDP, as a measure of global value added, fell by no more than 4.9% in 2009, traded value added plummeted by 18.3% during the same period. The decline in gross trade was even more pronounced, at 22.3%. This was due to particularly strongly affected capital goods such as machinery, which are produced by industries with a high percentage of imported inputs (Bems et al, 2011).

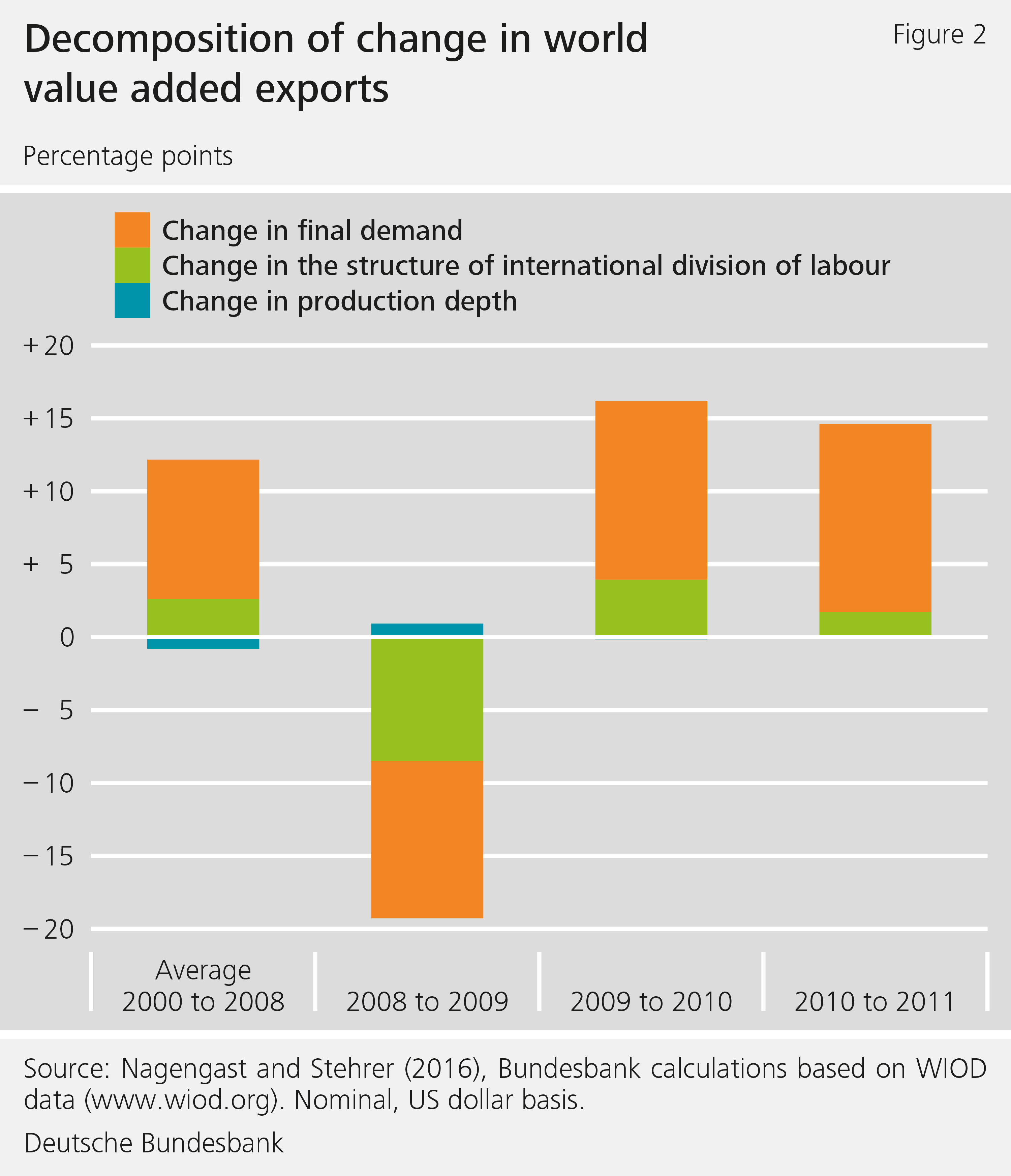

In this study, in order to gain a better understanding of the reasons for this decline, we decompose the changes in world value added exports into three basic components [using data from 41 countries and 35 sectors]: changes in sectoral production depth (ie how much of output is produced within a sector itself); changes in the structure of the international division of labour (in other words, from which countries intermediate inputs are sourced); and changes in the demand side (ie what and how many goods are in demand and from whom).

Figure 2 shows that, in an average year prior to the crisis, the volume of value added trade rose by around 11% in nominal terms. This was due to global increasing demand. By contrast, the expansion of cross-border value chains, ie firms in different countries cooperating in the production of goods, made only a small contribution.

In 2009, value added trade declined. Although falling demand played a large part in this, its relative importance was smaller than in previous years. In contrast, a less intensive international division of labour explains almost half of the collapse in value added trade: during the crisis, firms evidently increasingly sourced more of their intermediate inputs from domestic suppliers and made less use of international suppliers.

By 2010, global economic activity had already picked up again. The scale of the international division of labour, on the other hand, was still slightly below the pre-crisis level even in 2011, which was the last year for which data was available for our analysis.

International division of labour declined during the crisis

We are also able to show that the international division of labour declined in many countries and industries during the financial and economic crisis. Global growth was not, therefore, driven by individual outliers.

We also demonstrate that global value chains change with the economic cycle: during recessions, there is generally a marked decrease in the scale of such international cooperation. Our results are not confined to value added trade; they apply equally to gross trade flows.

We do not yet know at present why global value chains became shorter during the financial crisis. The trade collapse was, to a certain degree, a nominal phenomenon, since the prices of traded goods decreased above-average in 2009. In the analysis using price-adjusted data, however, it becomes apparent that the decline in the international division of labour nevertheless also explains just under half of the (real) trade collapse. Other possible causes, such as changes in the composition of firms constituting a sector or a more restrictive trade policy, can likewise be eliminated as an explanation.

The poorer financing conditions during the financial crisis might, however, provide an explanation: trade credits, which are deemed to be relatively risky, became significantly more expensive during this period (Asmundson et al, 2011). This increases the prices of imported intermediate inputs compared with those sourced from domestic suppliers, which leads export firms to tend to choose domestic suppliers instead. However, further studies are needed in order to provide direct evidence of the connection between the international division of labour and the supply of credit.

Regional and sectoral composition of demand

Alongside the decline in the international division of labour, the global slump in demand played a significant role in the great trade collapse.

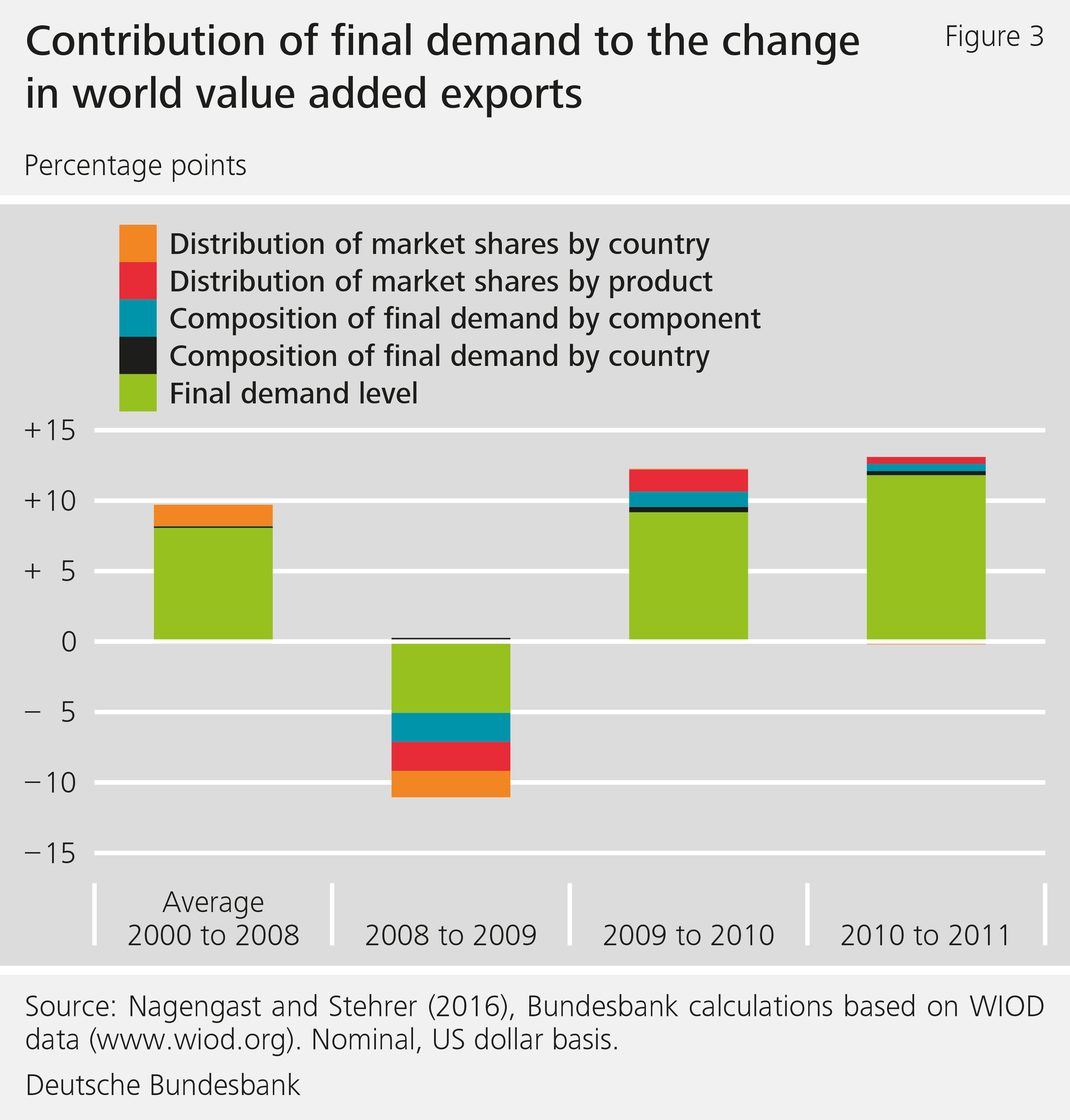

In our paper, we decompose the changes in final demand into one level effect and four composition effects. Figure 3 shows that the rising level of demand was the key factor prior to the crisis. A further, smaller contribution came from market share gains by China and other emerging market economies. For the trade collapse, on the other hand, the change in the composition of demand was at least equally important as the end users' reduced expenditure.

First, investments and inventories declined more strongly than consumption, as is usual in recessions. Since these demand components have a comparatively large import share, this further reduced value added trade. In particular, there was less demand for manufactured goods such as vehicles. These are purchased to an above-average extent from abroad.

Another cause of the trade collapse was the fact that global market shares shifted during the crisis. Economies like the countries of the European Union were particularly affected by falling demand. These countries make intensive use of the advantages of the international division of labour and are highly integrated into cross-border value chains.

Value added trade in the services sectors

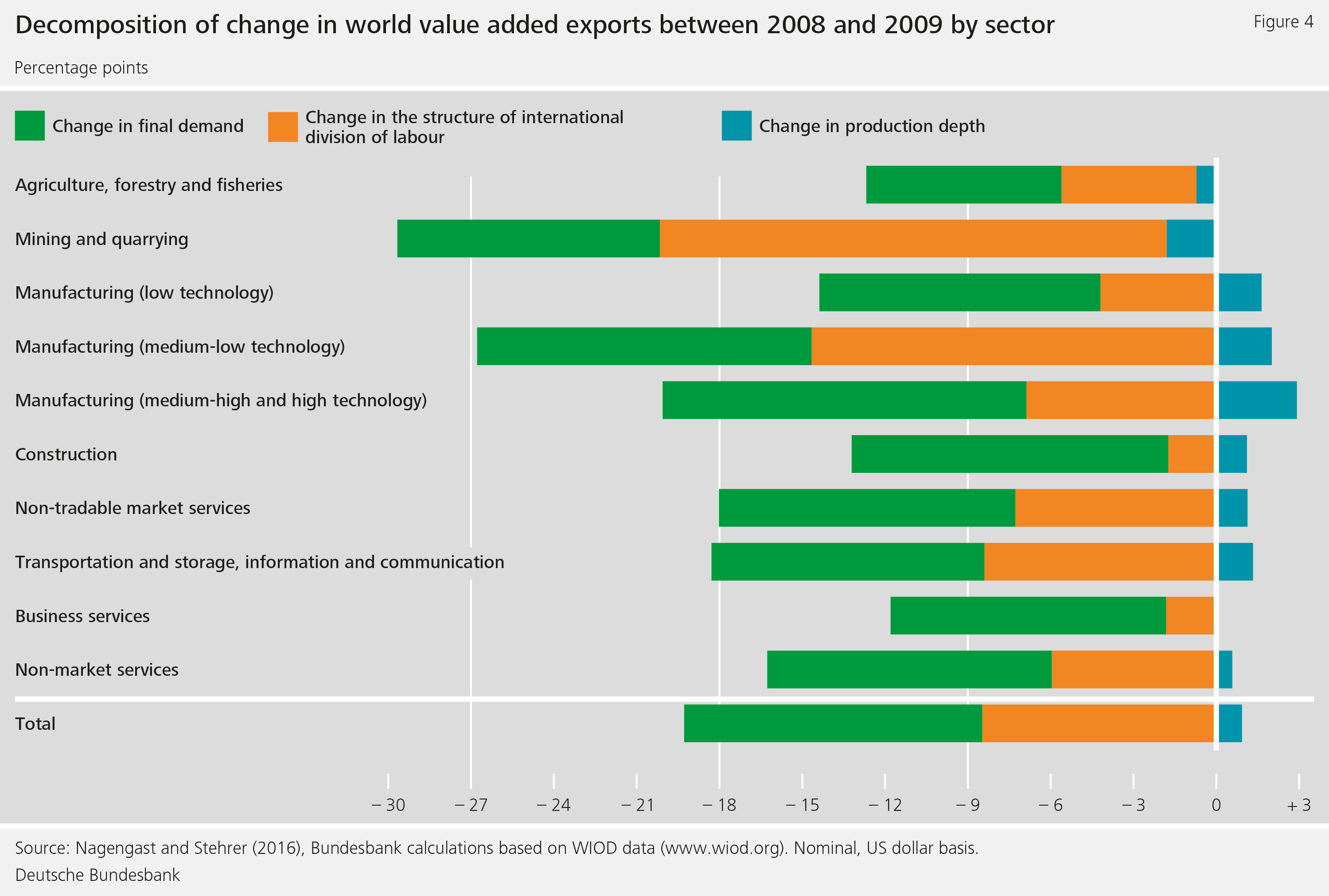

It is not only goods that are traded internationally. How did the trade collapse affect services? In terms of gross trade flows, there is much evidence that, unlike trade in goods, services transactions were largely unaffected by the crisis (Ariu, 2016). The value-added-based analysis, however, corrects this finding: the value added trade of nearly all the services sectors suffered a very marked slump during the great trade collapse, as is shown in Figure 4.

Our results are consistent with what we know about the differences between value added and gross trade flows: the percentage of services in value added trade is far higher than the percentage of services transactions in global gross trade flows. This is due to the fact that direct goods exporters often source intermediate inputs from domestic services firms, whereas direct services exports are hampered, for example, by different languages and legal systems. As a consequence, services firms indirectly benefit from their customers' export success. Conversely, however, they are also more vulnerable to external shocks than is generally acknowledged.

Conclusion

Our study shows that the great collapse in value added trade in 2009 was largely attributable to changes in the composition of final demand and to a temporary decline in the international division of labour. Unfavourable financing conditions during the financial crisis may possibly have played a part in the latter. Furthermore, the value-added-based analysis shows that the services sectors were much more strongly affected by the trade collapse than it would appear from the gross trade flows.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- A Ariu (2016), Crisis-Proof Services: Why trade in services did not suffer during the 2008-2009 collapse, Journal of International Economics, Vol 98(1), pp 138-149.

- I Asmundson, T W Dorsey, A Khachatryan, I Niculcea, and M Saito (2011), Trade and trade finance in the 2008-09 financial crisis, IMF Working Papers 11/66, International Monetary Fund.

- R Bems, R C Johnson and K-M Yi (2011), Vertical linkages and the collapse of global trade, American Economic Review, Vol 101 (3), pp 308-12.

- R Koopman, Z Wang and S-J Wei (2014), Tracing value-added and double counting in gross exports, American Economic Review, Vol 104(2), pp 459-94.

- A J Nagengast and R Stehrer (2016), The great collapse in value added trade, Review of International Economics, Vol 24(2), pp 392-421.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

2 MB, PDF