The impact of Eurosystem bond purchases on the repo market Research Brief | 21st edition – September 2018

German sovereign bonds have become scarce on the European repo market over recent years. A new analysis investigates the impact of the Eurosystem’s monetary policy asset purchase programme on the repo market, and shows that central bank securities lending can help to counteract scarcity.

In March 2015, the Eurosystem central banks began purchasing sovereign bonds from euro area countries as part of the public sector purchase programme (PSPP). Our analysis investigates the impact of this programme on the repo market. In a repurchase agreement (short “repo”), a security is sold for a – generally fixed – period of time and then repurchased. There are essentially two types of repos, which differ with regard to their collateralisation: general collateral and specific collateral repos.

In economic terms, a general collateral repo is comparable to a short-term collateralised loan. The buyer of the security provides the seller with short-term liquidity. In return, the buyer receives a security from the seller as collateral. The buyer receives the repo rate as remuneration for the provision of short-term liquidity. In this context, any bond from a pool of equivalent securities can serve as collateral (“general collateral”). By contrast, in the case of a specific collateral repo, the focus is on the specific security that the buyer acquires via the repurchase agreement. From an economic standpoint, a specific collateral repo is – for the buyer – comparable to securities lending, and the repo rate can be interpreted as a securities lending fee. Short-term purchases of specific securities are generally motivated by delivery obligations that need to be fulfilled, short positions, arbitrage transactions, or liquidity provisions on the secondary market. In our analysis, we are focusing on the repo rate for specific collateral.

Chart 1 shows that, since 2015, the repo rate of German sovereign bonds for specific collateral has been well below the (negative) interest rate of the Eurosystem deposit facility. The purchaser or borrower of the security therefore has to pay a comparatively high securities lending fee. This means that the targeted lending of a specific bond on the repo market is costly in relative terms, and this bond is referred to as “special”. We measure the degree of “specialness” as the difference between the deposit facility rate and the specific collateral repo rate of a given bond. The result is known as the “specialness spread”. A comparable spread is found by calculating the specialness spread with respect to the general collateral rate. The wider this spread, the scarcer a bond is on the market.

As the name suggests, specialness is actually a phenomenon that should only occasionally arise for isolated securities. However, Chart 1 shows that specialness has been more the rule rather than the exception for German sovereign bonds in recent years. Furthermore, increased volatility – i.e. the level of fluctuation in the repo rate – has been observed at year-ends and quarter-ends since 2015. This is often associated with efforts by financial intermediaries to retain German sovereign bonds, which are considered safe and liquid, and avoid offering them on the repo market on regulatory reporting dates (see BIS 2017).

Various explanatory approaches for changes on the repo market

What are the causes of these changes on the repo market? One possible explanatory approach for the specialness on the repo market is the Eurosystem asset purchase programme. The high volume of purchases within the PSPP may lead to certain sovereign bonds becoming scarce on the market. If the purchases are made primarily from active investors on the repo market, the supply of acquired bonds on the repo market may fall. As a result, the price of securities lending rises, which is reflected in a higher specialness spread. However, various regulatory measures implemented in the same time frame may have an impact on the repo market. For example, the leverage ratio and liquidity coverage ratio introduced as part of Basel III come into question as potential influencing factors.

In our analysis, we investigate the extent to which purchases of German sovereign bonds have impacted the repo market. In order to isolate the PSPP’s effects on the repo market from other influencing factors, such as the regulatory measures mentioned above, we look at the cross-section of German sovereign bonds on a day-by-day basis. This panel analysis enables us to control for market-wide determinants as well as for bond characteristics, which generally influence the repo rate. Usual determinants include, for example, the liquidity of the bond, high demand for the bond due to delivery obligations arising from Bund future contracts, or periods before an issue from the Federal German Finance Agency. In more concise terms, our analysis compares the specialness of various bonds that were purchased to a different degree by the Bundesbank on a particular day.

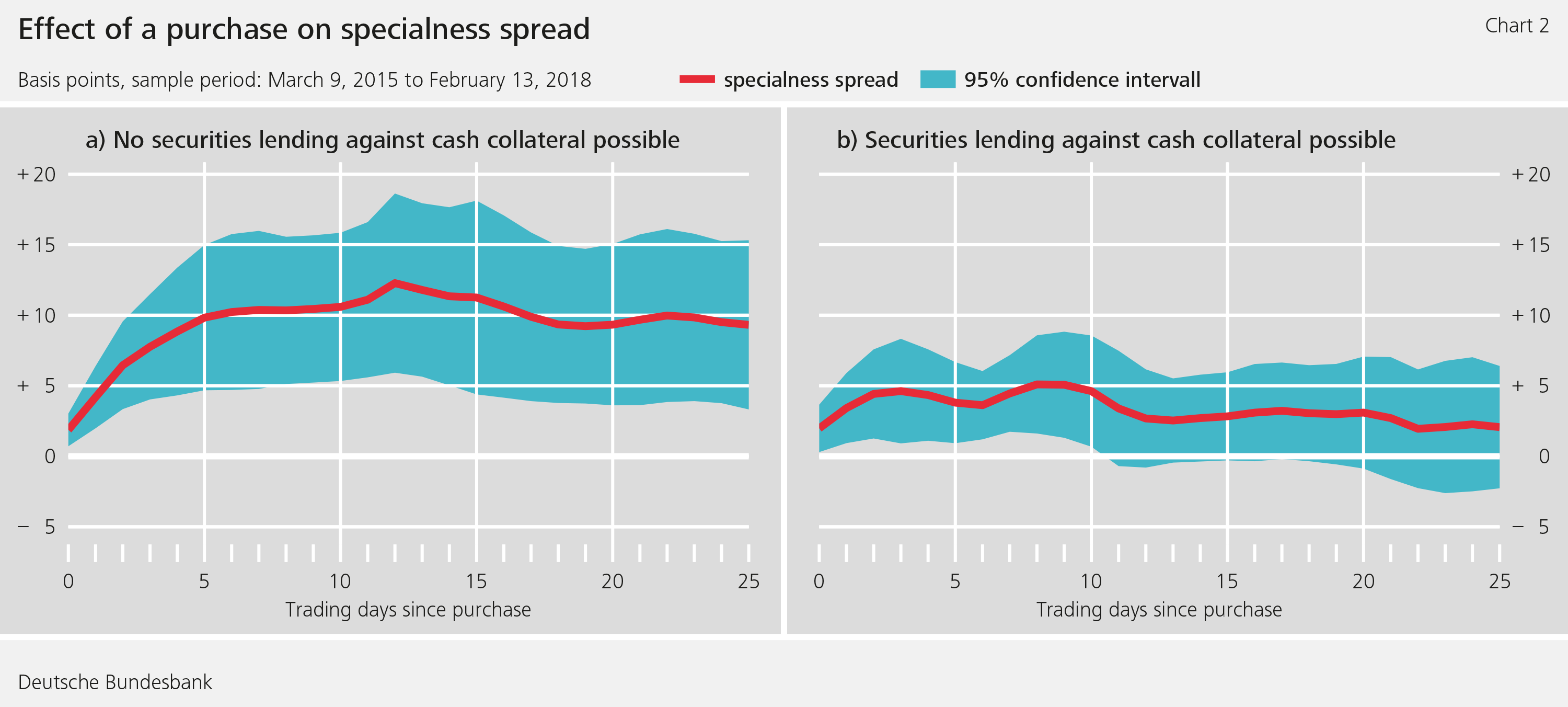

Based on our analysis, we calculate the impact of a purchase of a Federal bond on its specialness spread over the subsequent days. We first look at the impact of a purchase without the possibility of securities lending against cash collateral at the central bank. The development of the regression coefficients illustrated in Chart 2a shows that, following a purchase, the bond’s specialness spread rises significantly over the subsequent days. A purchase of one per cent of a bond’s outstanding nominal amount therefore results in its specialness spread rising by ten basis points, which is both economically and statistically significant. PSPP purchases therefore reduce supply on the repo market, which is reflected in higher lending fees. The studies by D’Amico, Fan, and Kitsul (2015) as well as Arrata, Nguyen, Rahmouni-Rousseau, and Vari (2017) document similar scarcity effects arising from purchase programmes in the United States and the Euro area. In addition, we were able to determine that the scarcity effect becomes greater as the volume of a bond that has already been acquired increases.

Counteracting scarcity effects via securities lending

In order to counteract potential scarcity on the bond market, the Eurosystem makes some of its assets acquired via the purchase programme available for securities lending. Initially, securities lending was carried out as combined repo/reverse repo transactions. This means that, if a bank wishes to borrow a bond from the Bundesbank, it must offer an equivalent bond as collateral. After sovereign bonds in the euro area became scarcer over the course of 2016, the Eurosystem adapted its procedure in December 2016. Since then, repos up to a certain limit have also been possible without an offsetting transaction, i.e. against cash collateral. Especially securities lending against cash collateral is in high demand among market participants.

In the following, we therefore investigate the extent to which this securities lending can mitigate scarcity on the repo market. Chart 2b shows the impact of a purchase on the specialness spread if securities lending against cash collateral is possible at the Bundesbank. Specialness rises to a considerably lesser extent at first and falls again more rapidly over time. This suggests that securities lending against cash collateral noticeably reduces the scarcity effect of the purchase programme. This finding also becomes apparent in Chart 1, where it can be seen that – apart from the large fluctuations at year-ends and quarter-ends – the repo market has stabilised considerably since the introduction of securities lending against cash collateral on 15 December 2016. Since the introduction of securities lending against cash collateral, the purchases of German sovereign bonds within the PSPP no longer result in additional, prolonged scarcity on the repo market. Another potential influencing factor in this context is the PSPP purchase parameters that were amended by the ECB Governing Council at the start of January 2017. From that point in time, the Eurosystem was also able to purchase bonds with interest rates lower than the deposit facility rate. This decision meant that the purchase volume was more evenly distributed across the maturity range, which may have also led to falling scarcity premiums for purchased bonds.

Conclusion

Due to the Eurosystem’s monetary policy asset purchase programme, German sovereign bonds have become more scarce on the repo market. Our analysis suggests that the securities lending implemented by central banks – particularly lending transactions against cash collateral – is an effective way of counteracting the effects of scarcity on the repo market.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

References

Arrata, W., Nguyen, B., Rahmouni-Rousseau, I., & Vari, M. (2017). Eurosystem's Asset Purchases and Money Market Rates.

BIS (2017). Repo market functioning, CGFS Paper No 59.

D'Amico, S., Fan, R., & Kitsul, Y. (2015). The scarcity value of Treasury collateral: Repo market effects of security-specific supply and demand factors.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein