How would a shift from taxing wages to taxing real estate affect the aggregate economy? Research Brief | 24th edition – January 2019

Tax reform designed to improve the conditions for macroeconomic growth without weighing on government budgets has been the topic of recent debate in Europe. One proposal on the table suggests reducing taxes on wages whilst at the same time raising those on land and property. A new study uses a modern DSGE model to examine how, within this model framework, such a shift would impact on the aggregate economy and to what extent property owners and tenants would be affected.

In Europe, wages are taxed at relatively high rates compared with other OECD countries. This minimises the incentive to work and can constrain the conditions for growth. The European Commission has repeatedly urged that labour taxation be reduced. The International Monetary Fund (IMF 2014) and the Organisation for Economic Co-operation and Development (OECD 2012, 2015), amongst other entities, suggest higher taxes on property ownership in order to recoup the revenue shortfalls. Proponents argue that higher tax rates would be associated with fewer distortions as the assessment basis is relatively immobile. In addition, they believe that the relevant tax rates in European countries are still relatively low.

Shifting from taxing wages to taxing real estate, in principle, has two countervailing effects. On the one hand, the lower level of labour taxation raises disposable labour incomes. In addition, if, for instance, employers’ non-wage labour costs fall, firms will increase their payrolls. Both of these effects would increase demand – including that for real estate – and stimulate economic output. On the other hand, taxing real estate at higher rates would diminish the attraction of property ownership. This could also affect tenants if the higher costs are passed through to rents. That, in turn, would reduce disposable incomes, and demand – especially for real estate – would fall, constraining output.

Positive effects prevail in macroeconomic terms

In order to assess which of these effects would prevail, macroeconomic equilibrium relationships have to be factored into the equation. Our analysis, based on a dynamic stochastic general equilibrium (DSGE) model, shows that the positive effects of such a tax reform would prevail in macroeconomic terms (Stähler 2018). In the model, households can buy or rent real estate. Loans can be taken out to finance the acquisition of real estate. The model is calibrated on the basis of European data for the 1999 to 2015 period.

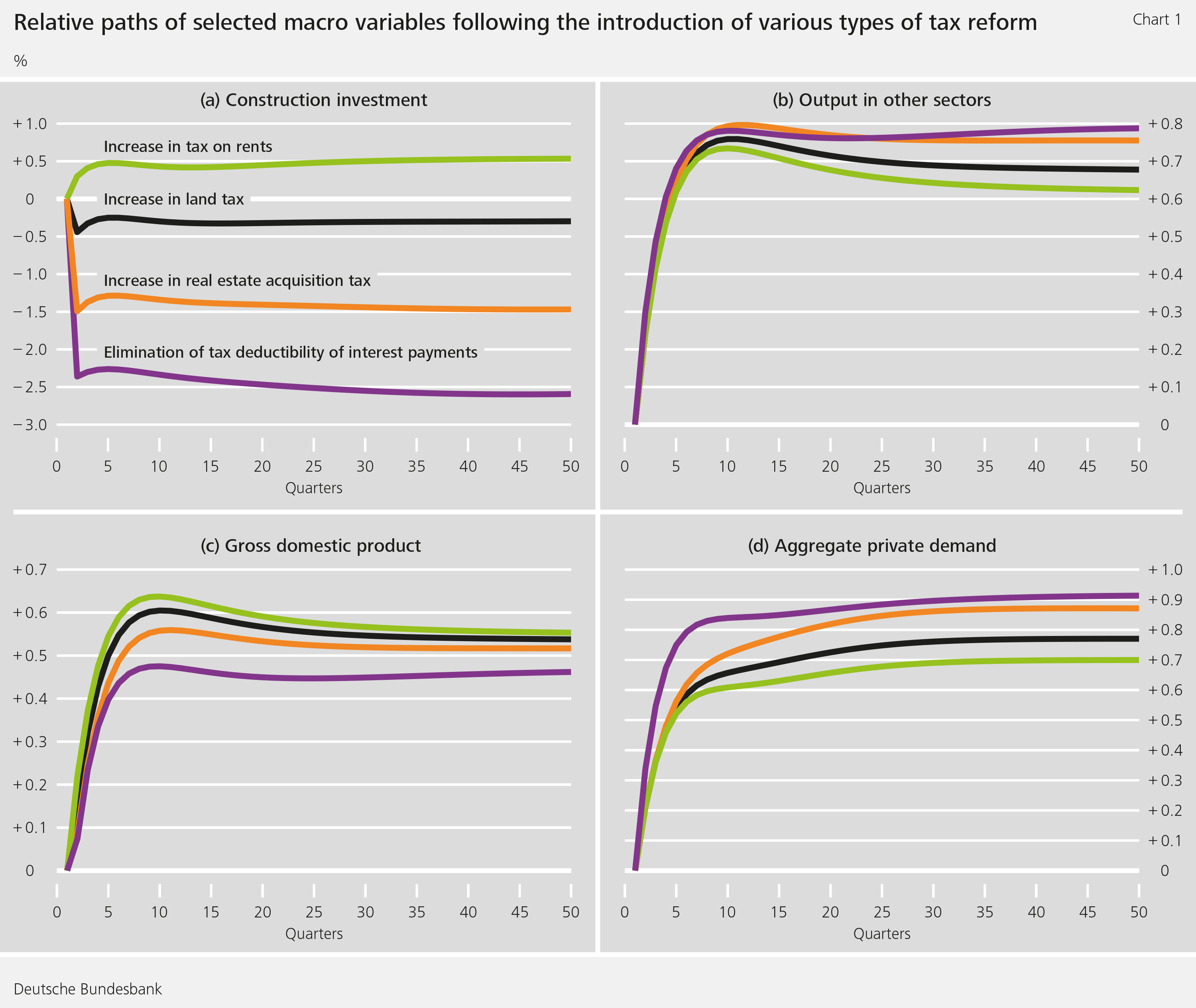

What we specifically study is a decrease in the average rate of labour taxation of nearly two percent funded in any one of four different manners: by increasing land tax, by increasing real estate acquisition tax, by increasing taxes on rents, and by eliminating the option of deducting interest payments on real estate loans from personal income taxes. Chart 1 presents output gains and losses in the various sectors and the effects on demand for consumer goods generated by the tax shift (each in percent compared with a scenario with no tax reform).

The detailed effects

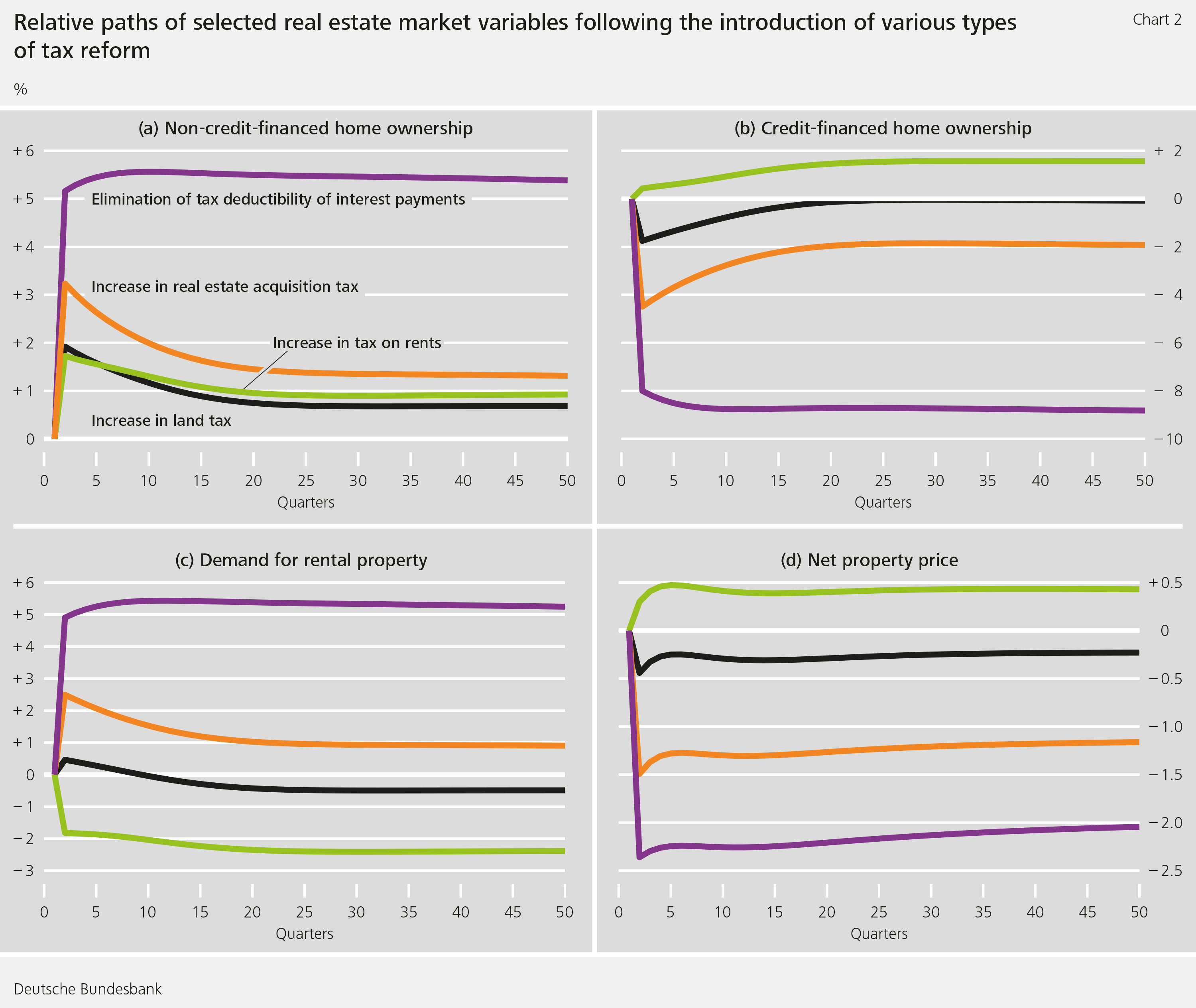

A land tax increases property owners’ ongoing costs. Real estate demand and prices, as well as construction investment, decline (see Chart 1a and Chart 2d). Landlords can pass part of these increased costs through to their tenants. A decline in construction work causes employment in the construction sector to decline. If taxes on wages fall, this generates positive effects in all other sectors that are not affected by higher taxes on real estate. These effects prevail in macroeconomic terms – yet the positive net impact is moderate (see Chart 1c).

If, however, real estate acquisition tax is increased instead, the effects are similar. However, in this case instead of the running costs of property ownership going up, transactions are taxed more heavily. Their volume is significantly smaller than the value of the stock of real estate. The rate of real estate acquisition tax must therefore be raised more strongly in order to achieve the same intake. As is shown by Chart 2d, owing to the stronger negative impact on transaction volume, this has greater effects on average net property prices, i.e. pre-tax purchase prices. In the case of rental property, part of those costs can, in turn, be passed on to tenants. To be sure, this increases the incentive to purchase residential property. On the other hand, since at the same time gross property prices – i.e. the purchase price including tax – also go up, overall the demand for credit-financed residential property falls (Chart 2b). This also causes the demand for rental property to increase (see Figure 2c). Disposable income losses are, on the whole, greater than if the land tax is increased. The negative impact in the construction sector is stronger. Nonetheless, here, too, the macroeconomic impact is positive, but less so than in the case of land tax (see Chart 1c).

Higher taxes on rents will initially hit landlords, whose disposable incomes will decrease. They will raise rents to offset this effect, thus increasing the incentive for people to acquire property for their own use (see Chart 2c). This increases aggregate demand for real estate even though the demand for properties to let decreases. Compared with the measures explained above, higher taxes on rents will have the mildest impact on GDP and employment, primarily owing to the positive effects in the construction sector. Consumer goods production shows the weakest rise, in relative terms (see Chart 1b).

In some European countries – but not in Germany – interest payments on real estate loans can be deducted from personal income tax. Eliminating this deduction option has strong negative effects on demand for credit-financed real estate (see Chart 2b). It becomes more expensive to finance a property. Landlords can take advantage of this trait to raise rents. Tenants and those who have to borrow to purchase property bear the negative effects. Landlords and wealthy purchasers benefit because property prices fall owing to the overall drop in demand for real estate. By contrast, the negative effects are the most severe in the construction sector. In this case, too, the overall macroeconomic effects are positive, yet these effects are the smallest (see Chart 1c).

Conclusion

Our model simulations show that the macroeconomic effect of shifting taxation from wages to real estate is moderately positive. In all cases considered, gross domestic product and household consumption rise. Although negative impacts in the construction sector may be expected, the other sectors will benefit. The burden or relief on landlords, tenants and owners of owner-occupied housing, however, depend on the specific implementation of the reform. If we assume that the real estate market is characterised by search frictions, however, the results are similar (see Bielecki and Stähler 2018).

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Bielecki, M. and N. Stähler (2018), Labor Tax Reductions in Europe: The Role of Property Taxation, Deutsche Bundesbank Discussion Paper No 30/2018.

- OECD (2012), OECD Economic Surveys: Spain, OECD Publishing.

- OECD (2015), OECD Economic Surveys: Italy, OECD Publishing.

- IMF (2014), Fiscal Monitor 2013 – Taxing Times, IMF World Economic and Financial Surveys.

- Stähler, N. (2018), Who Benefits From Using Property Taxation To Finance A Labor Tax Wedge Reduction?, Deutsche Bundesbank Discussion Paper No 03/2019.

| The author |

| Nikolai Stähler Research economist at the Deutsche Bundesbank, Directorate General Economics |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein