More stability through liquidity regulation Research Brief | 25th edition – May 2019

Regulatory requirements for banks are often criticised as having an adverse impact on lending and hence, indirectly, on the real economy. A new research paper uses a theoretical partial equilibrium model to study the direct effects a liquidity coverage ratio could have on banks’ loan supply.

Banks predominantly finance long-term loans using wholesale debt. But some of these debt claims can be withdrawn at short notice exposing banks to funding illiquidity risk. Since issuing new debt at short notice can sometimes be prohibitively expensive or only possible with a time lag, two new liquidity requirements have recently been introduced to mitigate liquidity shortfalls.

While the net stable funding ratio (NSFR) reduces funding risk over a longer time horizon, the liquidity coverage ratio (LCR) promotes the short-term resilience of banks’ liquidity risk profile, requiring banks, from January 2018 onwards, to hold a sufficient stock of high-quality liquid assets, such as sovereign bonds, to fully cover net outflows for a 30-day stress scenario.

These measures, however, may entail unintended side effects on banks’ loan supply (for an overview, see BCBS, 2016). One concern is that by requiring banks to hold more liquid assets, the LCR may crowd out the financing of loans. However, since the LCR has only been in operation since 2015, we lack sufficient data to quantitatively assess its effects on the real economy. Moreover, due to interactions with other regulatory instruments, indirect effects may mask the LCR's direct impact so that the latter may be difficult to identify. In Bucher et al. (2018) we thus use a theoretical model to examine the effect of the LCR and other instruments on a bank’s stability and loan supply. Interactions between different regulatory instruments are disregarded, which means that our paper cannot be interpreted as an all-encompassing assessment of these instruments.

Banks’ portfolio decision depends on credit risk

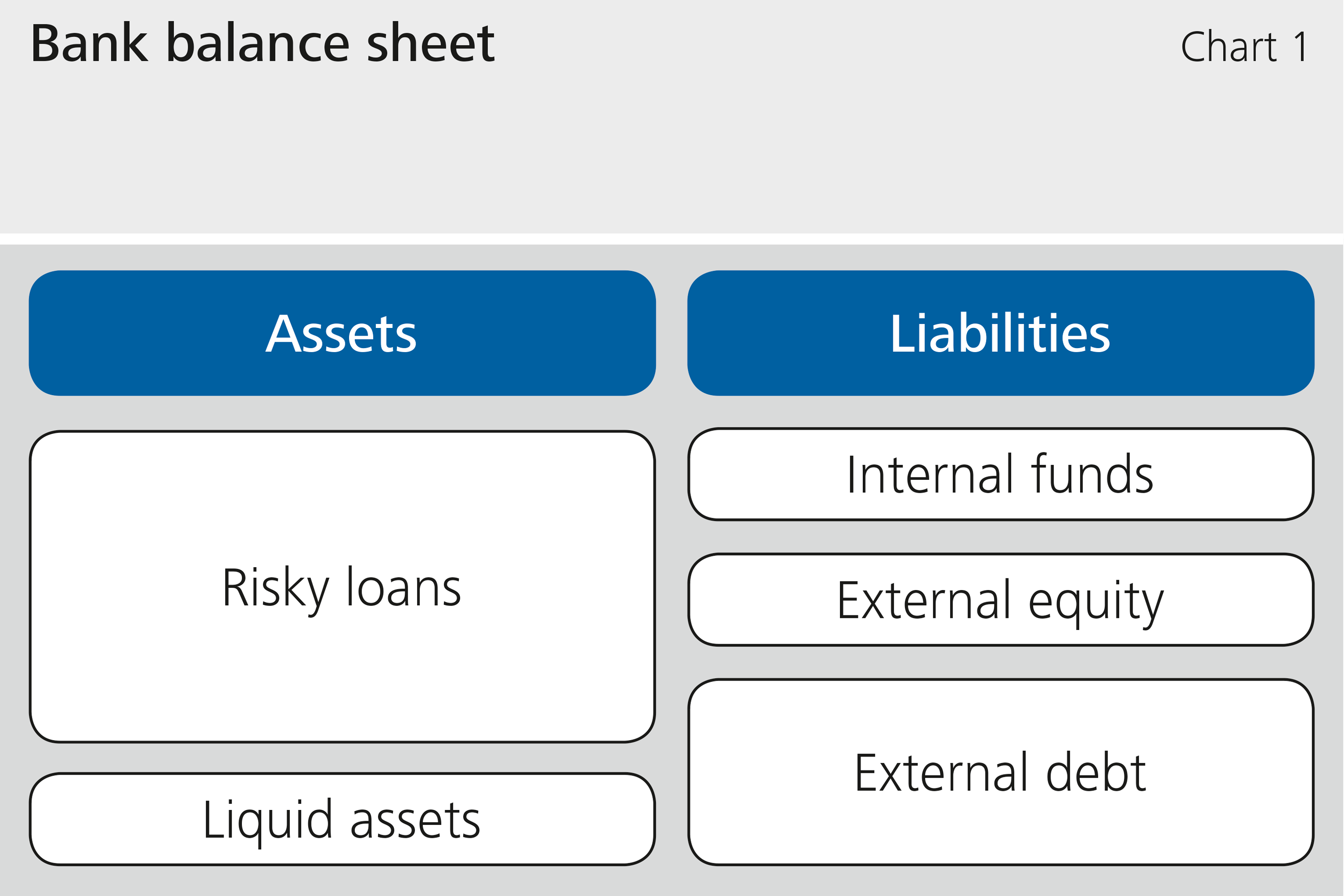

Expanding on Bucher et al. (2013), we consider a profit-maximising, forward-looking bank that decides on its investment and capital structure at the beginning of each period. By using internal funds, and raising equity and wholesale debt from external investors, the bank can invest in risky loans and hold risk-free liquid assets (see Chart 1).

Our model assumes that it is more costly for the bank to issue equity when compared with wholesale debt. This reflects governance issues between external shareholders and the bank’s management where, for example, the management possesses superior information regarding the bank’s risk profile than the shareholders. While wholesale debt claims may be withdrawn early, equity claims are stable. Consequently, the bank will fail if its interim returns are insufficient to repay early withdrawals by debt holders. By issuing equity, the bank can mitigate such failure, but this is costly and can hamper the loan supply. Internal funds comprise retained earnings as well as the values of existing assets, such as outstanding loans, and therefore cannot be changed at short notice. They are not as costly as external equity, but their volume hinges on past investment and funding decisions made by the bank and the performance of these investments.

Two options for investment decision

The bank internalizes how loan credit risk will impact the availability of internal funds for its future investment decision. If these earnings turn out to be low, the bank will only possess few internal funds in the future, and it will become more difficult to use these as collateral to raise new funds externally. This, in turn, will constrain its future loan supply.

In the absence of regulation, a bank has two options. The first is to grant more loans as a precaution. This will increase the bank’s internal funds at the interim, which will allow the bank to more easily issue new debt and increase the loan supply. As such, the bank is less exposed to the risk of failure and is less reliant on issuing debt to refinance loans. We refer to this as the safe capital structure option. Loan supply, however, would very much depend on how economic conditions evolve and thus fluctuate strongly over time. The second option is for the bank to be agnostic about the interim funding gap and delay any adjustment until the shock to internal funds has materialized. In this case, the bank would have less internal funds at the interim date to refinance loans, and it would issue more debt when compared with the first option. This, however, exposes the bank to a greater risk of failure. As such, we refer to this as the risky capital structure option.

The bank’s decision depends on various parameters. If, for example, the credit risk on loans is high, this will impinge on the bank’s retained earnings, thereby forcing the bank to take on more debt even though this exposes the bank to a greater risk of failure.

LCR brings greater stability, but loan volatility is stronger

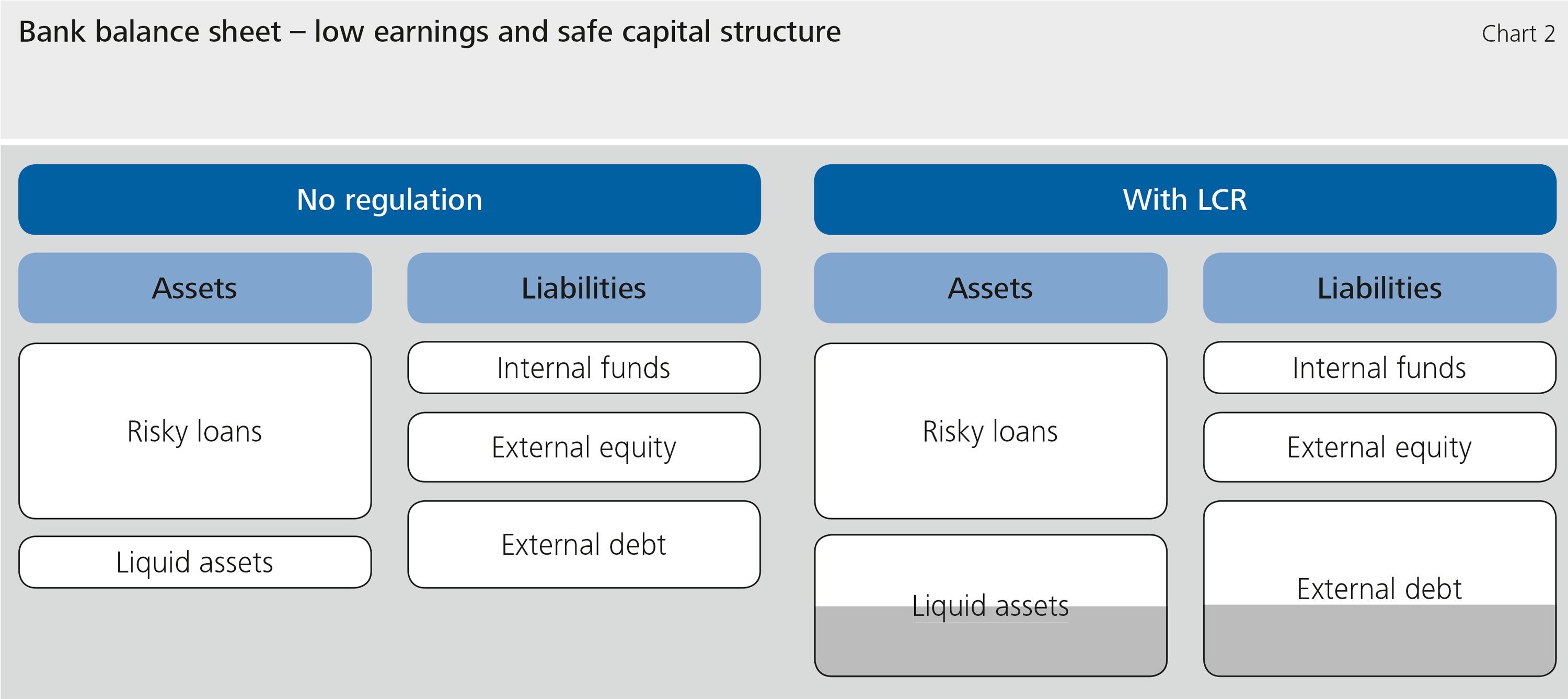

How does the LCR influence the bank’s choice on its capital structure? A bank required to comply with the LCR needs to hold a certain amount of liquid assets to cover total net cash outflows in each period. Provided the bank opts for a safe capital structure even without the LCR, the LCR will have no effect on loan supply. From the investors’ perspective, the bank’s debt is safe and, the return on debt is identical to the earnings from the liquid assets due to perfect competition. In order for the bank to comply with the regulatory requirement, it invests the newly raised debt into risk-free liquid assets. The balance sheet simply expands (see Chart 2).

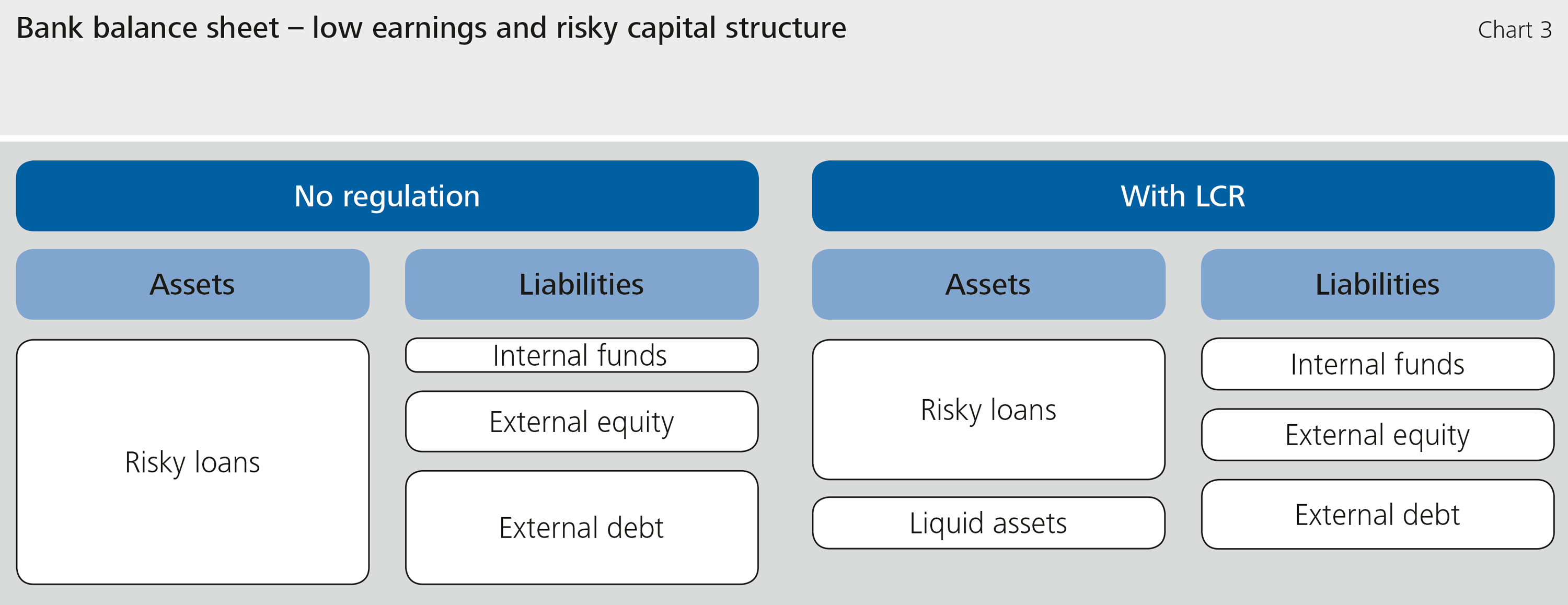

If, however, the bank opts for a risky capital structure, investors will be bound to have concerns that the bank could fail. They will demand a higher return on debt, which will also make it more expensive for the bank to invest in risk-free liquid assets. Without regulation, a bank with a risky capital structure will therefore have no incentive in our model to invest in liquid assets. If the bank’s earnings from its loans and thus its internal funds are low, the LCR works, economically speaking, like a tax. Debt is no longer available in its entirety to finance loans and must instead also be invested in unprofitable liquid assets. This constrains loan supply. A bank can dilute this effect of regulation by expanding its loan supply likewise to the first option as a precaution and building up additional internal funds so as to maximise its profit (see Chart 3).

Under the risky capital structure, the LCR induces an initial increase in the loan supply, which declines if retained earnings turn out to be low. Furthermore, the “taxation” of debt cuts into the profit made by the bank such that, even when loans entail greater earnings risks, the bank opts for a safe capital structure. Our findings therefore indicate that the LCR increases stability but also has the potential to trigger greater volatility in bank’s loan supply. As the model disregards possible feedback effects our paper should not be interpreted as an all-encompassing assessment of the LCR but rather of its direct incentive effects on banks.

Conclusion

We show that the effects of the liquidity coverage ratio on loan supply depend on the capital structure selected by an unregulated bank. Banks that already have a solid capital structure without this regulation are likely to be able to meet the new requirements by simply expanding their balance sheets and not constraining their loan supply. The LCR may give other banks an additional incentive to lower balance sheet risks. This may, however, result in a more volatile loans supply, depending on the earnings risks associated with loans.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- BCBS (2016), Literature Review on Integration of Regulatory Capital and Liquidity Instruments, BCBS Working Paper 30.

- M. Bucher, D. Dietrich und A. Hauck (2013), Business Cycles, Bank Credit and Crises, Economics Letters 120, 229-231.

- M. Bucher, D. Dietrich und A. Hauck (2018), Implications of Bank Regulation for Credit Intermediation and Bank Stability: A Dynamic Perspective, Bundesbank Discussion Paper 43.

The authors | ||

| Monika Bucher Economist at Deutsche Bundesbank, Directorate General Banking and Financial Supervision | Diemo Dietrich Senior Lecturer at Newcastle University Business School | Achim Hauck Associate Professor at Nottingham Business School |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein