On the reference indicator for determining the Basel III countercyclical capital buffer Research Brief | 27th edition – July 2019

The global financial crisis was a lesson that it is not enough to merely monitor the stability of individual banks – the stability of the banking sector as a whole is also a crucial factor, which is precisely what the countercyclical capital buffer (CCyB), a key instrument under the Basel III regime, is there to help safeguard. However, recent research indicates that adhering too strictly to the reference indicator envisaged under the Basel III framework might lead to a situation in which supervisors activate the CCyB either too late or not at all ahead of a future financial crisis.

Excessive lending in a number of countries, first and foremost the United States, has been identified as one of the main factors which led to the last global financial crisis. To dampen the risks stemming from excessive lending, the Basel Committee on Banking Supervision recommends deploying the countercyclical capital buffer (CCyB). Thus, during spells in which supervisors believe that too much credit is flowing into the private non-financial sector, banks are expected to build up a capital buffer to safeguard the banking sector as a whole against a potential credit-fuelled financial crisis.

Supervisors form their opinion on current lending activity within a country, and thus on whether or not to activate the country-specific CCyB, using what is known as “guided discretion” – an approach which combines a rules-based component with a discretionary component to arrive at an overall assessment of risks (Tente et al. (2015)). While a variety of indicators and complementary analysis feed into the discretionary component, the rules-based component is based on a reference indicator. If this country-specific reference indicator exceeds a certain level, the idea is that supervisors should consider activating the CCyB. Ideally, two potential mistakes should be avoided here. First, the indicator should not mistakenly signal excessive credit growth when there is none, since this might lead to the CCyB being activated when it is not warranted. Second, the indicator should signal excessive credit growth in both a reliable and timely manner so that the CCyB can be activated in good time.

Reference indicator and risk of “inaction bias“

One benefit of having a reference indicator is that it allows a shared analytical framework to be formulated across countries. Another is that it is a starting point, in the assessment of lending, for avoiding what the theory calls “inaction bias“ – that is to say, the inclination to act too tentatively and thus too late or not at all.

However, under certain circumstances, having a reference indicator can also promote “inaction bias”, for example if that reference indicator does not measure exactly what it is supposed to. Imagine a situation where lending is excessive. If the reference indicator does not flag this, but the indicators which feed into the discretionary component do, supervisors might be inclined to act tentatively and give a higher weighting to the evidence provided by the reference indicator, precisely by demonstrating “inaction bias”.

Since the reference indicator (and any CCyB buffer guide derived from it) is a starting point for analysis (see Basel Committee on Banking Supervision (2010)), it is often the first thing supervisors discuss when making their decisions. This could make other indicators seem less important, even if supervisors are alerted to the fact that any indicator can convey misleading signals and each of them should thus be interpreted with care (see Basel Committee on Banking Supervision (2010)).

My latest paper concludes that the Basel III reference indicator is fraught with methodological problems which could result in macroprudential policymakers receiving misleading signals regarding the deployment of the CCyB (Schüler (2018)). I find that the Basel III reference indicator may well tend to promote “inaction bias” rather than curb it.

Problems involved in calculating the Basel III reference indicator

The reference indicator used is the credit-to-GDP gap. It is extracted via a statistical filter from the ratio of lending to the private non-financial sector and gross domestic product (GDP). My research concludes that this filter gives reason to doubt whether the credit-to-GDP gap is capable of flagging excessive lending across countries and over time.

The statistical filter used is the Hodrick-Prescott filter (Hodrick and Prescott (1997)) which, though frequently used in economic analysis, has also attracted criticism. My paper finds that the filter, as it is defined in the Basel III regime, can give rise to severe problems.

Why use a statistical filter in the first place?

As mentioned above, the rules of the Basel III framework require the reference indicator to be calculated on the basis of the credit-to-GDP ratio. An increasing ratio means that lending is growing faster than economic output. But that does not necessarily mean that too many loans are being granted. Indeed, there have been times in the past where the credit-to-GDP ratio increased persistently for a variety of fundamentally sound reasons, one example being the introduction of new financial instruments. To detect whether a rise in the credit-to-GDP ratio does indeed point to excessive lending, the Basel III framework recommends to adjust the credit-to-GDP ratio by eliminating the factors driving a long-term increase. These long-term increases, the so-called trend, are supposed to be identified by the Hodrick-Prescott filter mentioned above. The reference indicator – that is, the credit-to-GDP gap – is then the difference between the credit-to-GDP ratio and its trend. If this gap is two percentage points or more, supervisors should consider activating the capital buffer.

Filter method masks short-term cycles

The filter is applied to a time series (the credit-to-GDP ratio) which rises (or declines) over longer periods. One problem arising from this is that, within the gap, cycles of a certain length are particularly amplified, thereby masking others. Cycles are amplified at the point at which the filter “detrends” the time series, i.e. decomposing it into trend and the gap itself. In the filter design proposed by the Basel III framework, cycles which are longer than roughly 30 years are regarded as trend. Owing to this assumption, the credit-to-GDP gap is driven chiefly by long-term cycles, i.e. those lasting up to 30 years. As a result, shorter-term cycles such as business cycles, which often last between two and eight years, can no longer be discerned. Being the reference indicator set forth under the Basel III framework, the Hodrick-Prescott filter is applied as a constant under this assumption to the credit-to-GDP ratio for various countries and over time.

However, one problem with this assumption is that credit-to-GDP cycles (or credit cycles) tend to differ in length from one country to the next, as pointed out by a great many studies. In fact, they sometimes resemble business cycles and can vary between shorter and longer phases (see, for example, Schüler et al. (2017)). Inevitably, then, this assumption means that the reference indicator probably is not suited to measuring excessive credit growth across countries. Another observation which supports this finding is that common rates of change – which are calculated using a difference filter and are not fraught with the problems facing the Hodrick-Prescott filter – are demonstrably better suited than the Basel III gap for predicting financial crises.

An additional problem is the significance of the filter design proposed in Basel III for the future path of the credit-to-GDP gap. If financial crises occur at shorter intervals, it is unlikely, owing to the filter design, that the reference indicator will flag them going forward. For instance, if a crisis occurs in the next few years, only a little more than ten years would have elapsed since the last crisis. But because the Basel III reference indicator amplifies long-term cycles, it may need up to 30 years for it to flag the next crisis.

For the reasons set out above, then, there is a possibility that if the reference indicator is adhered to strictly, the credit-to-GDP gap calculated according to the Basel III rules could result in a CCyB which is out of sync with lending.

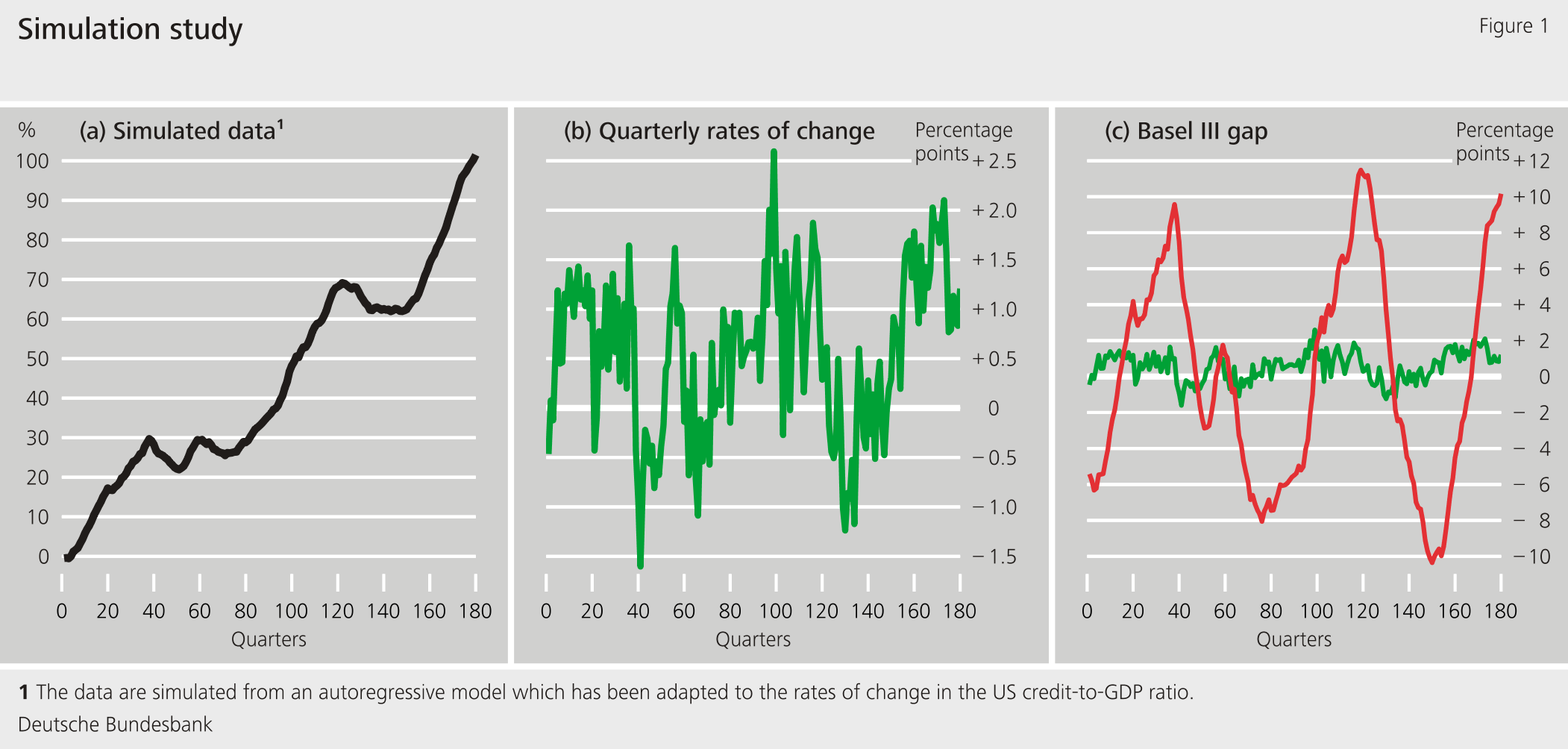

Simulated data show how the Hodrick-Prescott filter amplifies cycles

Figure 1 uses simulated data to illustrate how the Hodrick-Prescott filter amplifies certain cycles. Panel (a) shows the credit-to-GDP ratio following an empirically plausible path. It rises on average over time, but also experiences the occasional setback. This empirical path means that the quarterly rates of change show all the short-term and long-term cycles (panel (b)). Lastly, panel (c) indicates the cycles amplified by the method proposed under the Basel III regime (red line). As readers can see, the short-term fluctuations visible in the green time series are masked here, but the long-term developments are still evident.

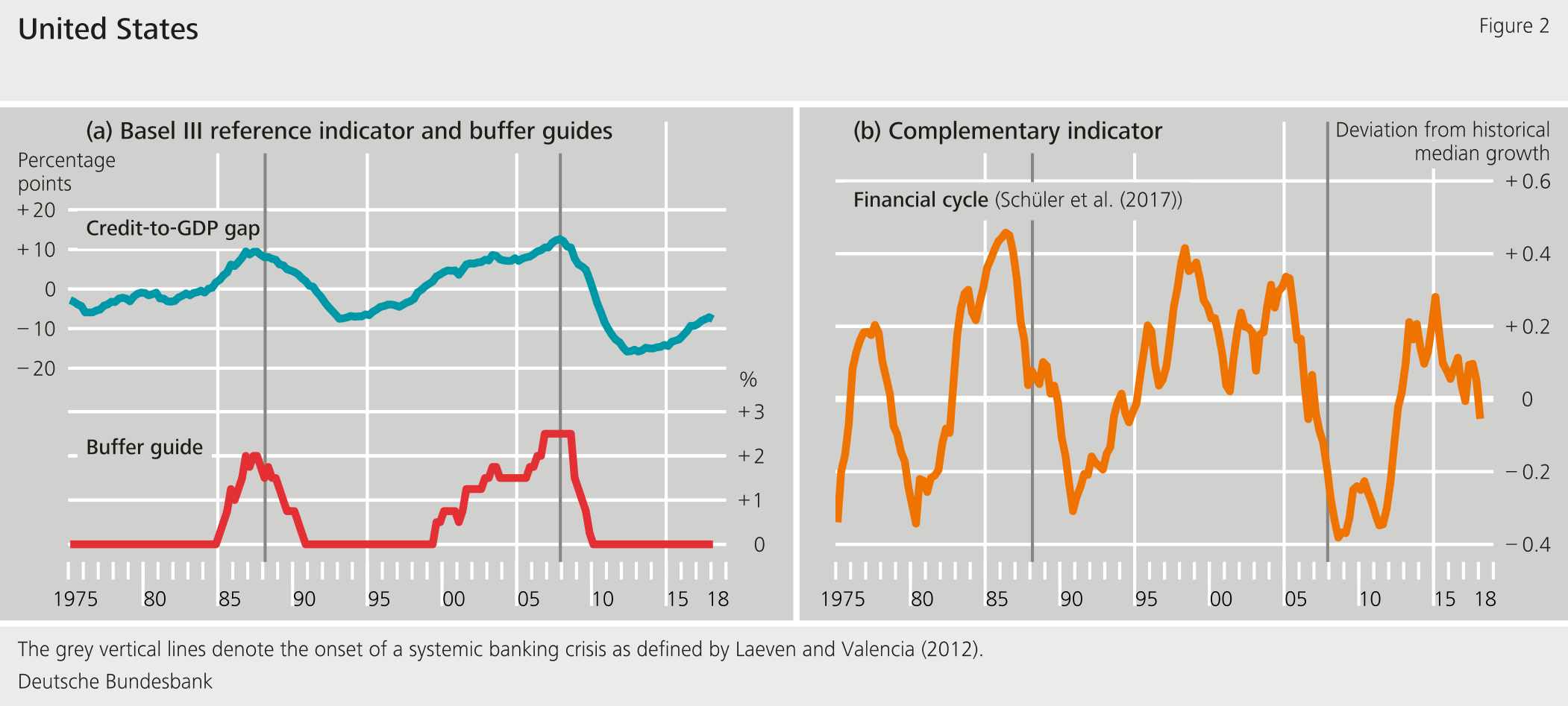

US credit-to-GDP gap not currently flagging any risk, but a complementary indicator does

Figure 2 (a) shows the actual reference indicator for the United States (blue line) and the buffer guide derived from it (red line). The latter value indicates the percentage by which the CCyB would need to be increased for US banks if the decision were based solely on the rules-based component. The focus on long-term cycles inherent in this method produces two undesirable effects. First, after the onset of the global financial crisis in the autumn of 2007 (grey vertical line in Figure 2(a)), the reference indicator does not signal quickly enough that the buffer can be released. It is especially after financial crises that the buffer needs to be released in order to shore up bank lending. Second, the reference indicator at last count (i.e. at the beginning of 2018) is still strongly negative, even though lending in the United States has already recovered, which may signal a build-up of risk. On this point, Lael Brainard, who is a member of the Board of Governors of the US Federal Reserve System, remarked back in April 2018 that it may well be appropriate to activate the CCyB if the US economy continues on this path. The buffer is currently still set at 0%.

Together with Paul Hiebert and Tuomas Peltonen, I propose a different measure which avoids the problems outlined above because it is based on a difference filter (Schüler et al. (2017)). The idea behind this complementary indicator is that, so far, excessive lending can be identified by a simultaneous strong increase in asset prices, such as the rise in house prices in the United States before the onset of the global financial crisis. More specifically, this indicator flags expansions and contractions common to credit and asset prices, as a signal for leveraged asset price bubbles. Using G7 countries and a group of 13 European countries, we demonstrate that our indicator is better than the credit-to-GDP gap at predicting financial crises. Unlike the US credit-to-GDP gap, our indicator for the United States quickly flags both the onset of the global financial crisis and the recovery in the US financial sector, as Figure 2 (b) illustrates.

Conclusion

The reference indicator envisaged under Basel III for determining the CCyB, which is used in many countries, disregards the fact that credit cycles can differ significantly in duration – both over time and across countries – besides attaching too little significance to shorter cycles in particular. Adhering too rigidly to the reference indicator risks promoting “inaction bias” because there may be cases where the reference indicator is incapable of flagging excessive lending. Measures designed to detect leveraged asset price bubbles represent a promising complement for supervisors.

Disclaimer |

The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Basel Committee on Banking Supervision (2010): Guidance for national authorities operating the countercyclical capital buffer, Bank for International Settlements.

- Brainard, L. (2018): Safeguarding financial resilience through the cycle, Speech at the Global Finance Forum, Washington, D.C., April 19.

- Tente, N., Stein, I., Silbermann, L. und Deckers, T. (2015): Der antizyklische Kapitalpuffer in Deutschland. Analytischer Rahmen zur Bestimmung einer angemessenen inländischen Pufferquote, Deutsche Bundesbank.

- Hodrick, R. and E. Prescott (1997): Postwar U.S. business cycles: An empirical investigation. Journal of Money, Credit and Banking 29, 1-16.

- Laeven, L. and Valencia, F. (2012): Systemic banking crises database: An update, IMF Working Paper WP/12/163.

- Schüler, Y., Hiebert, P. and Peltonen, T. (2017): Coherent financial cycles for G-7 countries: Why extending credit can be an asset, ESRB Working Paper 43.

- Schüler, Y. (2018): Detrending and financial cycle facts across G7 countries: Mind a spurious medium term!, ECB Working Paper 2138.

The author |

|

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein