How expectations of households and firms can impact the effectiveness of central bank communication Research Brief | 31st edition – February 2020

Recently, many central banks have begun communicating not just their current monetary policy, but also its probable predicted future path. However, the effectiveness of this communication hinges on how strongly it is able to influence the inflation expectations of households and firms. A standard property of macroeconomic models is that expectations respond very strongly to such announcements. A new theoretical study shows that the effects are much smaller in a model capable of matching survey evidence on expectations formation.

In the aftermath of the financial crisis, many central banks set their key interest rates close to or even below zero. To influence inflation while interest rates are at their lower bound, central banks need other policy instruments. Forward guidance is now a common choice. This is communication of the probable future path of monetary policy.

Forward guidance is based on the fact that when households and firms make decisions, they take into account the future state of the economy. As a result, households’ consumption and savings decisions will be affected by expected movements in the real interest rate (the difference between the short-term interest rate and the expected inflation rate). In particular, a lower real interest rate implies higher current consumption, as it makes saving less attractive. Households’ and firms’ inflation expectations are thus of key importance for monetary policy. This is especially true when interest rates are at their lower bound. In this case, the central bank can only lower real interest rates and stimulate inflation through higher inflation expectations.

The forward guidance puzzle

Researchers usually use general equilibrium models when assessing the effects of forward guidance on inflation and output. These models capture the interactions between the economy’s state and the expectations of households and firms. In such models, promising to keep interest rates low for a long time boosts demand by lowering real rates and so reducing households’ incentives to save. Higher demand leads firms to increase their prices, so inflation rises. The expected higher inflation rate further reduces the real interest rate so households prefer to shift even more of their consumption to the present.

The standard model leads to the surprising conclusion that the effect of promising to hold interest rates low for an additional period gets larger, the further into the future the extra cut takes place. This is because the future reduction in the interest rate immediately lowers the real interest rate, due to higher inflation expectations. With lower real interest rates from the announcement, households increase their consumption for the full period of low rates. Thus, the macroeconomic effects accumulate over time, and may produce an extremely large result. This conclusion is known as the forward guidance puzzle. In our study (Bersson, Hürtgen, and Paustian, 2019), we investigate how a more realistic expectations formation process influences the effectiveness of central bank communication and forward guidance.

Expectations formation in the model and the data

In standard models, it is generally assumed that households and firms immediately fully update their expectations after the announcement of a policy measure. In the academic literature, this is known as “rational expectations”. By contrast, our study examines the consequences of slowly adjusting expectations, in line with the empirical evidence.

Empirical studies on expectations formation based on both experiments (Mauersberger and Nagel, 2018) and surveys (Coibion, Gorodnichenko, Kumar and Ryngaert, 2018) show that households adjust their expectations only partially. In order to replicate this, our model of expectations formation is analogous to the way a chess player thinks: depending on their level of experience, they may think one, two, three or even more steps ahead. How far into the future they plan will then have an impact on their current choice.

Transferred to our model framework, this means that, in the first round of expectations formation in our model, households and firms take account only of the policy measure’s direct, immediate effect, keeping unchanged their expectations about the economy’s future path, i.e. as they were before the announcement. If all households and firms were to behave in this way in every period, it would lead to some temporary equilibrium path for the economy. At the second level of expectations formation, households form expectations based both on the direct effect of the measure, and on the temporary equilibrium path for the economy from the lowest level. Likewise, at the third level, households form expectations based on the direct effect of the measure as well as the temporary equilibrium path from the second level, and so on.

Were households able to calculate an infinitely large number of expectation levels, the outcome would correspond to the one under “rational expectations”. This is in stark contrast to the previously mentioned empirical literature, which typically finds evidence for only two to three rounds of expectations formation.

Results in the standard model with rational expectations

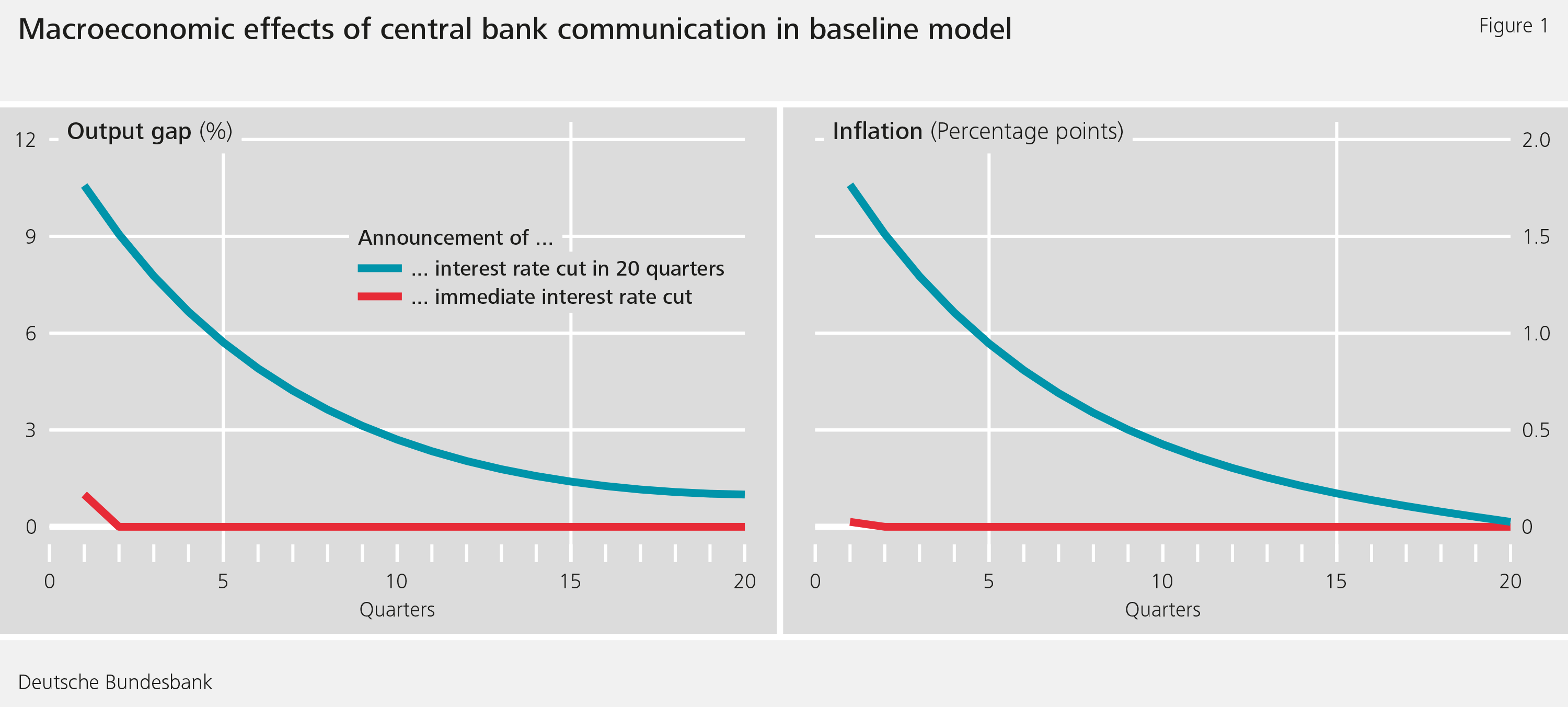

To illustrate the transmission channel of forward guidance in the standard model, we compare two different policy measures. The red lines in Figure 1 show the effects of an immediate interest rate cut of 100 basis points on the output gap (the difference between actual gross domestic product and potential output) and on inflation. We compare these outcomes to the results of a promise from the central bank to lower their interest rate in twenty quarters, holding fixed interest rates in the intervening time. This is shown with the blue lines in Figure 1. Given an immediate monetary policy impulse, inflation and output show a slight rise (red lines). However, if the same monetary policy impulse is announced twenty quarters in advance, with a commitment to hold rates constant for the intervening period, the effects on inflation and output become many times stronger (blue lines). This is due to the fact that the future expansionary monetary policy measure raises inflation expectations (so lowers real rates and increases consumption and inflation) as soon as it is announced. The longer the commitment to hold rates constant before the rate cut, the greater the amplification of the macroeconomic effects.

Model with more realistic expectations formation

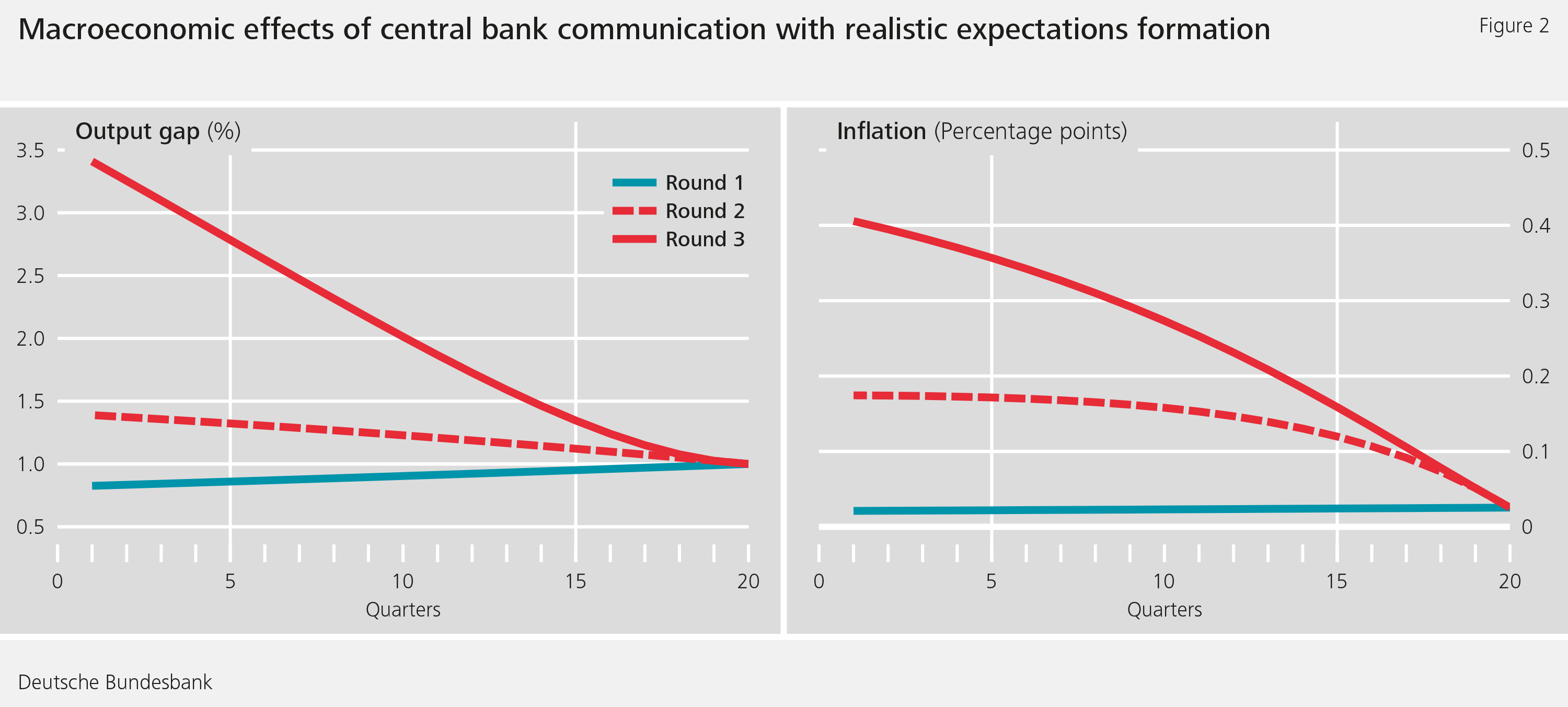

Figure 2 shows the impact of the same two exercises in a model in which households’ and firms’ expectations formation is more realistic. In line with experimental studies and surveys, we show results for households and firms that go through one, two or three levels of calculation in order to form their expectations. This expectations formation process reduces the strong anticipation effects present under rational expectations (see the blue lines in Figure 1).

If households only go through one level of calculation for expectations (blue line in Figure 2), then only the direct effect is taken into account. If households go through two levels of calculation (dashed red line), some of the expected future effects are considered, resulting in slight increases in the impact on inflation and output. If households complete three levels of calculation (red line), then there is a substantial effect on the output gap, but it is still considerably lower than in the standard model (Figure 1).

Increasing the number of levels of calculation households and firms go through in order to form expectations means they take more and more account of the future macroeconomic effects of the announcement, resulting in dynamics approaching those of the standard model with rational expectations (Figure 1, blue line). Our results show that forward guidance has more plausible (i.e. muted) effects than in the standard model if a more realistic expectations formation process is used. The prior literature discusses various other model changes that can further mitigate the surprising effects of forward guidance. These include relaxing the assumption that households take decisions under perfect information.

Conclusion

Committing to hold interest rates low for an additional period can have very large economic effects in the standard model with rational expectations. These effects become considerably weaker if expectations formation is modelled in an empirically plausible way. Our analysis underlines the importance for central banks of understanding how households and firms form their expectations. The Bundesbank’s pilot study on expectations of households in Germany should be able to supply crucial data to help with this; see Deutsche Bundesbank (2019).

Disclaimer |

The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Bersson, Betsy, Patrick Hürtgen and Matthias Paustian (2019), “Expectations formation, sticky prices, and the ZLB”, Bundesbank Discussion Paper 34/2019.

- Coibion, Olivier, Yuriy Gorodnichenko, Saten Kumar, and Jane Ryngaert (2018), “Do you know that I know that you know…? Higher-order beliefs in survey data”, NBER Working Paper 24987.

- Deutsche Bundesbank (2019), “The relevance of surveys of expectations for the Deutsche Bundesbank”, Monthly Report, December 2019, pp. 53-71.

- Mauersberger, Felix and Rosemarie Nagel (2018), “Chapter 10: Levels of Reasoning in Keynesian Beauty Contest Models: A Generative Framework”, in C. Hommes and B. LeBaron, Handbook of Computational Economics, Volume 4.

The authors | ||

© privat

|

|

© privat

|

| Betsy Bersson Duke University | Patrick Hürtgen Deutsche Bundesbank | Matthias Paustian Federal Reserve Board |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein