Effects of the ECB asset purchase programme on economic activity and prices in the euro area Research Brief | 37th edition – December 2020

At the beginning of 2015, the ECB Governing Council decided to implement an asset purchase programme to increase inflation by lowering longer-term interest rates. In our study, we examine how the programme has affected prices and economic activity in Germany, France, Italy and Spain. We are particularly interested in whether the effects differ across countries.

In January 2015, the Governing Council of the ECB announced the launch of an asset purchase programme (APP). The aim of this programme was to lower long-term interest rates and thereby increase the inflation rate towards the target of below, but close to, 2%. The main component of the APP was a purchase programme for public sector bonds. Net purchases were initially discontinued at the end of 2018, by which point the APP had been adjusted several times in terms of maturity and purchase volumes. Various studies have shown that the APP helped to increase economic growth and inflation across the euro area as a whole. In our study, we estimate the economic effects of the APP in the four major Member States of the euro area (Germany, France, Italy and Spain) up to the end of 2018 and examine whether the programme has affected these countries differently.

For our analysis, we use a Bayesian vector autoregressive multi-country model in order to model the interaction between euro area financial market variables and country-specific economic variables, such as gross domestic product, consumer prices and government bond yields, for the four Member States. We estimate the effects of the APP by comparing two model scenarios, one with and one without a purchase programme. The simulations are based on the assumption that the programme was largely responsible for developments in euro area government bond yields over the APP period. We feed the stimuli generated by the APP measured in this manner into our model via changes in these yields. These are based on revisions to expected yields in consecutive Eurosystem staff macroeconomic projections.

The APP increased gross domestic product in all the countries examined

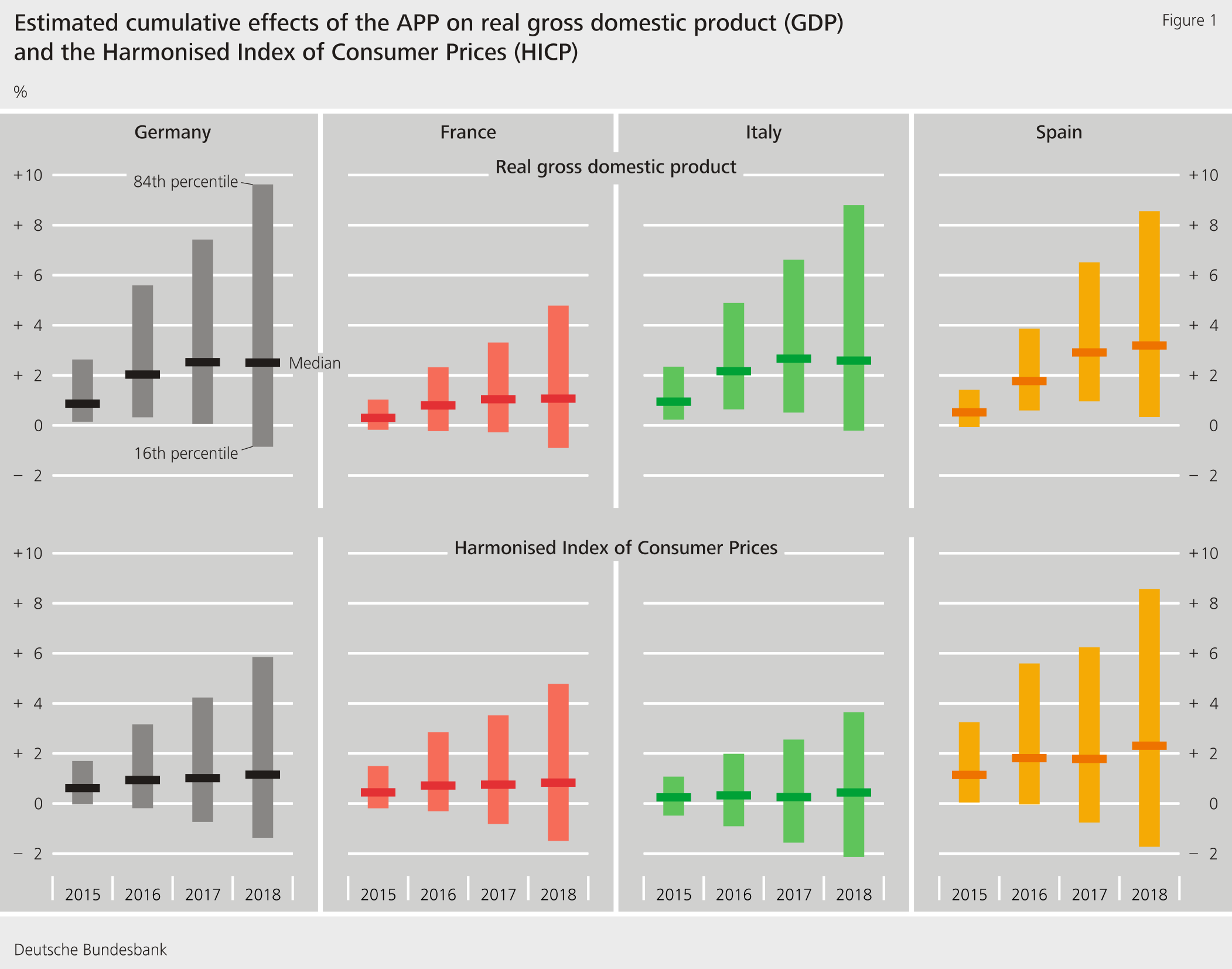

For the end of each year from 2015 to 2018, we estimate how real gross domestic product (GDP) and the Harmonised Index of Consumer Prices (HICP) differ in the four countries between the scenario with the APP and the scenario without the programme. The estimation method provides probability distributions for these findings, and Figure 1 shows some information about these probability distributions. The horizontal bars indicate the median of the estimated distribution. According to this estimate, real GDP in Germany was just under 0.9% higher at the end of 2015 than it would have been without the APP. We estimate its overall effects on GDP in Germany between 2015 and 2018 to be 2.5%.

The coloured bars represent the interval between the 16th and 84th percentiles of the distribution and provide an insight into the degree of estimation uncertainty. When assessing whether the APP had a positive effect, we consider the share of the probability distribution that lies within the positive range. These shares are above 70% for all countries, which suggests that the APP had a positive effect on real GDP. By comparison, the estimated effects on consumer prices are smaller and the shares of the probability distributions with positive effects are also somewhat lower than for real GDP. In Italy, in particular, it is doubtful whether the price level rose as a result of the APP. The finding that the APP had a weaker effect on the price level than on output is consistent with other studies (e.g. Burriel and Galesi, 2018; Wieladek and Pascual, 2016).

Effects on GDP in France comparatively weak

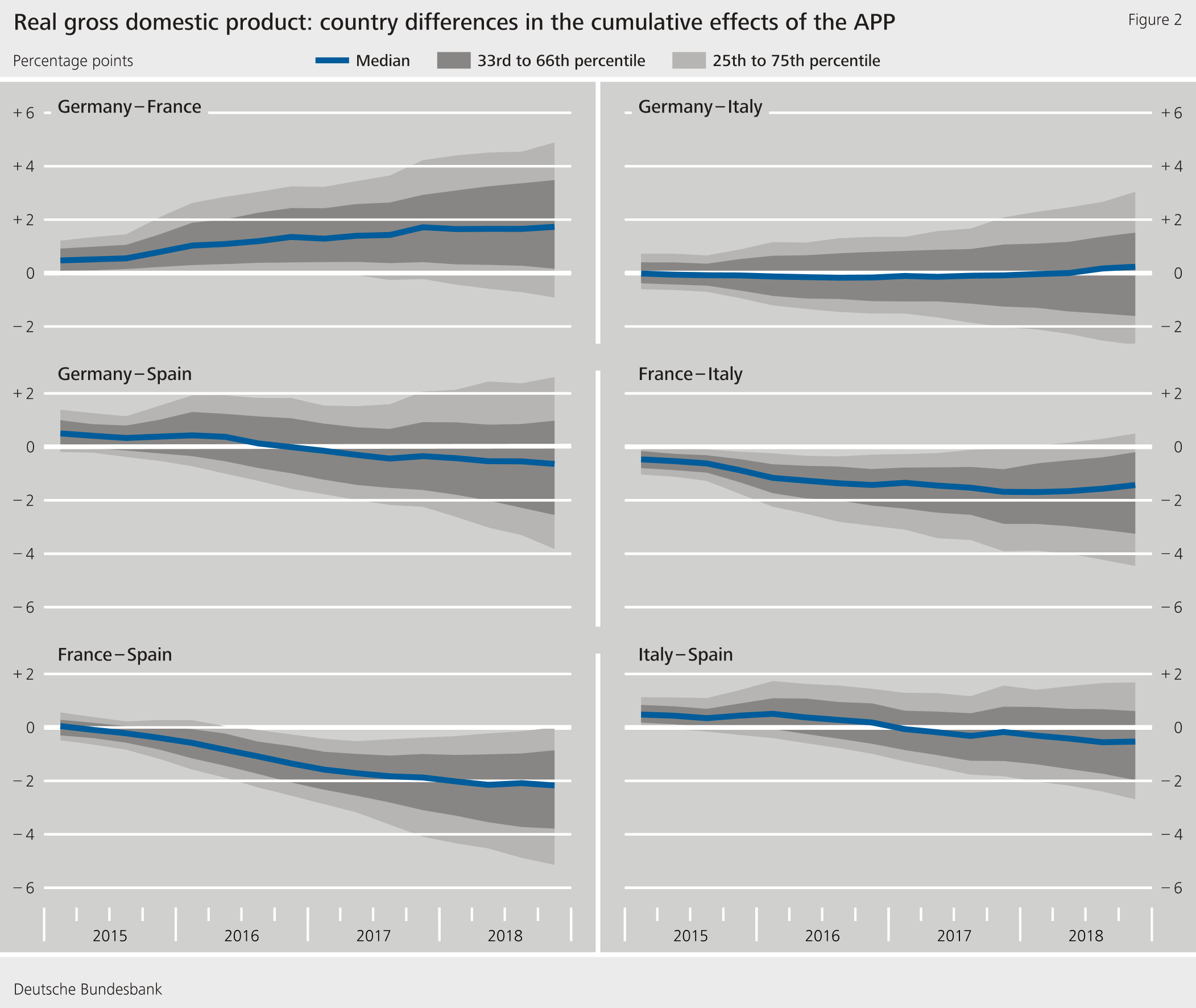

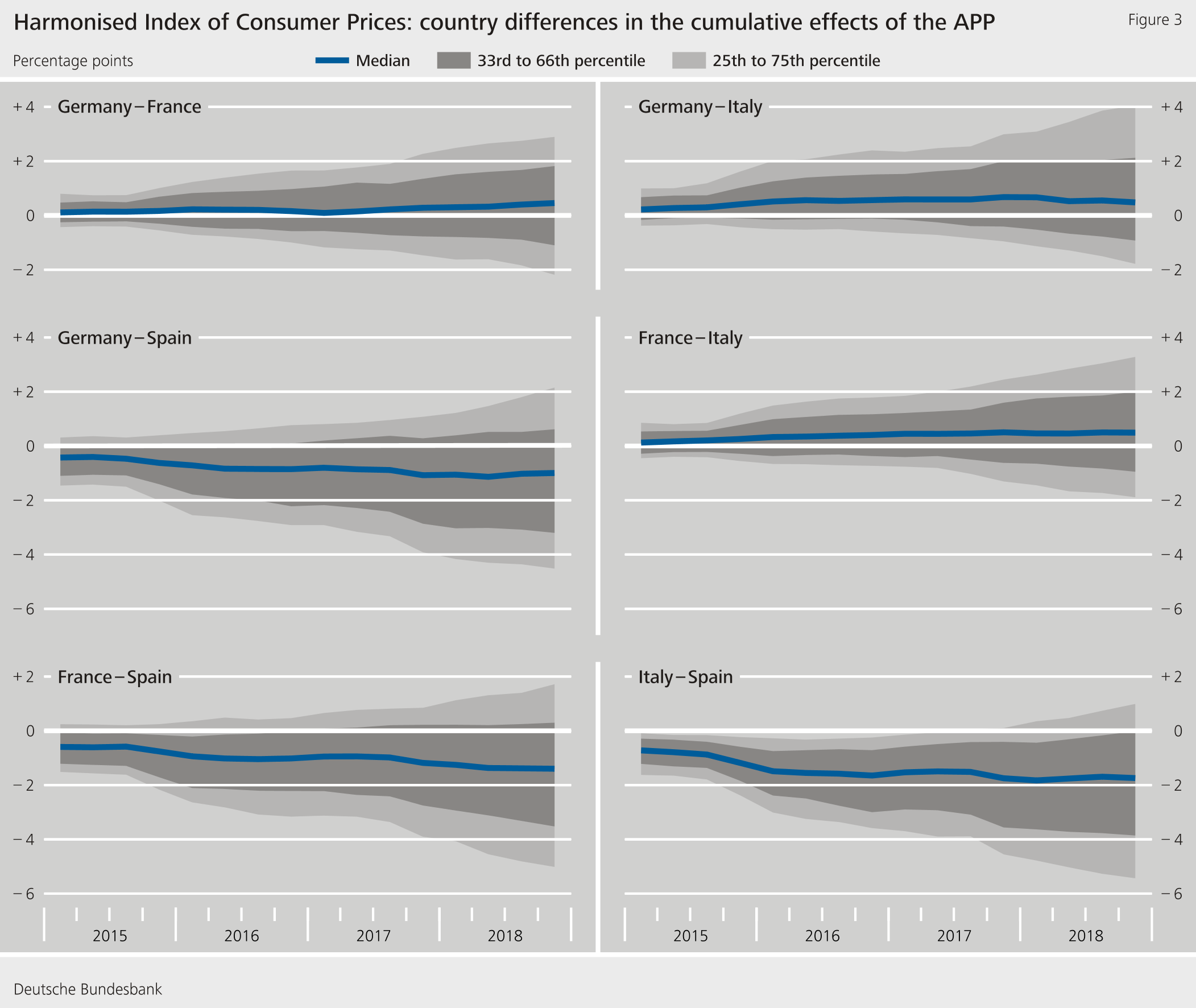

The findings in Figure 1 provide initial clues that the APP may have affected the four countries to differing degrees. We look at this question in more detail in the next step. To do this, we use our model to calculate the statistical distribution of the difference in the estimated effects of the APP for each country pair and for any point in time between the beginning of 2015 and the end of 2018. Figures 2 (real GDP) and 3 (HICP) show the findings for all possible country pairs. Positive values mean that the effects of the APP were greater in the first country named than in the second. Negative values mean that the effects were smaller in the first country. The location of the probability distribution relative to the zero line shows how greatly the effects of the APP differ in the two countries.

Comparing pairs of countries indicates clear differences in the effects on GDP between France and the other three countries. When comparing Germany with France, for example, a much larger share of the distribution lies above the zero line, indicating that GDP in Germany increased more strongly as a result of the APP than in France: the median of GDP in Germany rose by around 1.7 percentage points higher after four years than in France due to the APP. When comparing France with Italy and Spain, the vast majority of the distribution is in negative territory, which demonstrates that the APP also had weaker effects on GDP in France compared with Italy and Spain.

The differences between the countries in terms of the price level are less clear: the findings in Figure 3 indicate that the APP had a stronger positive effect on consumer prices in Spain than in the other three countries. Price effects tended to be weakest in Italy.

Conclusion

Our results show that the ECB’s asset purchases under the APP contributed to growth in real gross domestic product and consumer prices in Germany, France, Italy and Spain. Overall, the programme had a greater effect on output than on price developments, with this effect varying in degree between the individual countries. In France in particular, GDP rose much less strongly than in the other three countries. The reasons for this cannot be determined using our model, and this remains the task of future research.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- P. Burriel and A. Galesi (2018), Uncovering the heterogeneous effects of ECB unconventional monetary policies across euro area countries, European Economic Review, 101, 210-229.

- M. Mandler and M. Scharnagl (2020), Estimating the effects of the Eurosystem’s asset purchase programme at the country level, Deutsche Bundesbank Discussion Paper No 29/2020.

- T. Wieladek and A. Garcia Pascual (2016), The European Central Bank’s QE: A new hope, Discussion Paper Series DP11309, Centre for Economic Policy Research.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein