How institutional investment funds’ reach for yield intensifies asset price volatility

Research Brief | 38th edition – January 2021

27.01.2021

Research Brief

Alexandru

Barbu, Christoph

Fricke, Emanuel

Mönch DE

Institutional funds manage the majority of the assets under management of all German investment funds. This research brief documents that institutional funds act in a strongly procyclical manner: they actively invest in higher-yielding, longer-duration and lower-rated assets as yield spreads compress. We show that this intensifies asset price volatility and highlight reasons behind this procyclical investment behaviour.

Institutional funds, which are set up as specialised funds in Germany, manage the assets of a few institutional investors, mostly smaller banks and insurers, but also pension funds, foundations and churches. Unlike retail funds, they are only available to experienced (institutional) investors, often have more flexible investment mandates and prescribe longer redemption notice periods for fund shares. Institutional funds make up the majority of German investment funds and managed three-quarters of the assets under management of all German investment funds at the end of June 2017.

Institutional funds’ reach for yield

In recent years, global interest rates have fallen significantly. Yields on new investments in bonds issued by many governments and enterprises are even negative at present. The literature has shown that this development leads to an increase in the risk appetite of private investors, but also of banks, insurers and retail funds (see, for example, Hanson and Stein (2015), Becker and Ivashina (2015), and Choi and Kronlund (2018)). In a new study (Barbu, Fricke and Mönch (2020)), we examine whether this also applies to institutional funds. For our analysis, we use the investment fund statistics collected by the Bundesbank, which have recorded the portfolios of all investment funds registered in Germany in detail on a monthly basis since 2009. Our focus is on institutional bond funds and mixed funds that hold euro-denominated bonds. In the period we observed – from November 2009 to June 2017 – the level of risk in the bond portfolios of these funds grew significantly. The average bond credit rating went down by two notches, from AA+ to AA- (S&P scale). At the same time, average duration, a measure of interest rate risk, increased by just under one year. These changes extend far beyond the adjustments that banks, insurers and retail funds made to their bond portfolios, for example, over the same period. As this period was shaped by falling and negative interest rates as well as declining risk premia, it is reasonable to assume that, on average, the increased level of risk in the fund portfolios was driven by reaching for yield in response to falling interest rates.

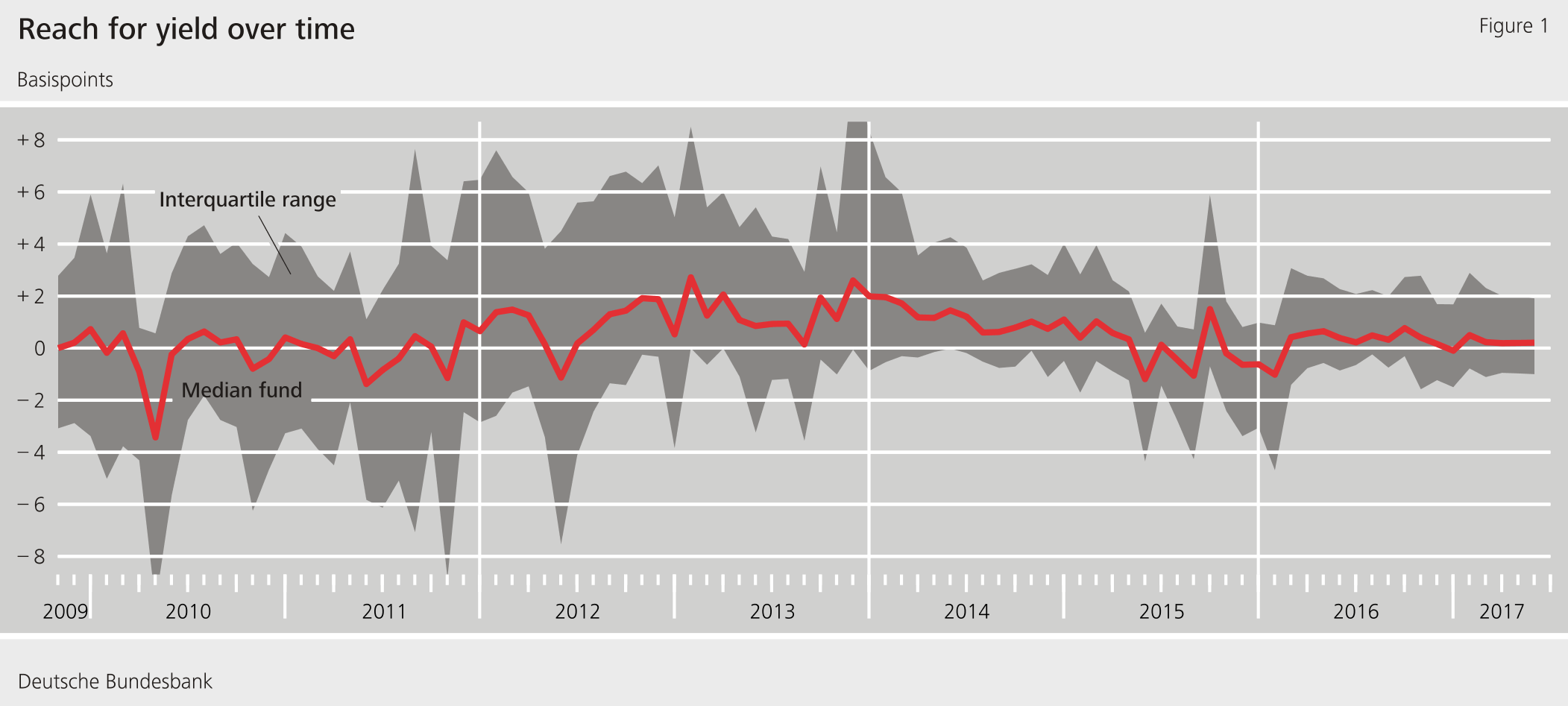

In order to separate the intentional increase in portfolio risk from pure valuation effects, we measure the reach for yield using the change in the total portfolio return as a result of active portfolio rebalancing from one month to the next. Specifically, we interpret a transaction-related increase in the total portfolio return as an intensified reach for yield. According to this measure, reaching for yield was especially pronounced in the period from 2012 to 2015, during which the majority of funds increased the level of risk in their portfolios (see Figure 1).

Figure 1: Reach for yield over time

In various regression analyses, we are able to provide evidence that the reach for yield increases when there is a reduction in the interest rate on the funds’ bond portfolios. To this end, we decompose the interest rate into two components that proxy credit risk and interest rate risk. The credit risk of a bond is calculated using the interest rate spread vis-à-vis the German zero-coupon Bund rate with an equivalent maturity. Interest rate risk is defined as the interest rate on the bond less the default risk and the risk-free interest rate. If the interest rate risk premium for existing bonds is 1 percentage point lower, institutional funds purchase bonds in the following month with yields that are, on average, 42 basis points higher. Following an equivalent change in credit risk, funds invest in bonds with yields that are 16 basis points higher. Their investment behaviour is therefore procyclical: on average, the funds increase their share of riskier bonds when their prices rise and reduce their share of riskier bonds when their prices fall.

Investment behaviour still procyclical during coronavirus crisis

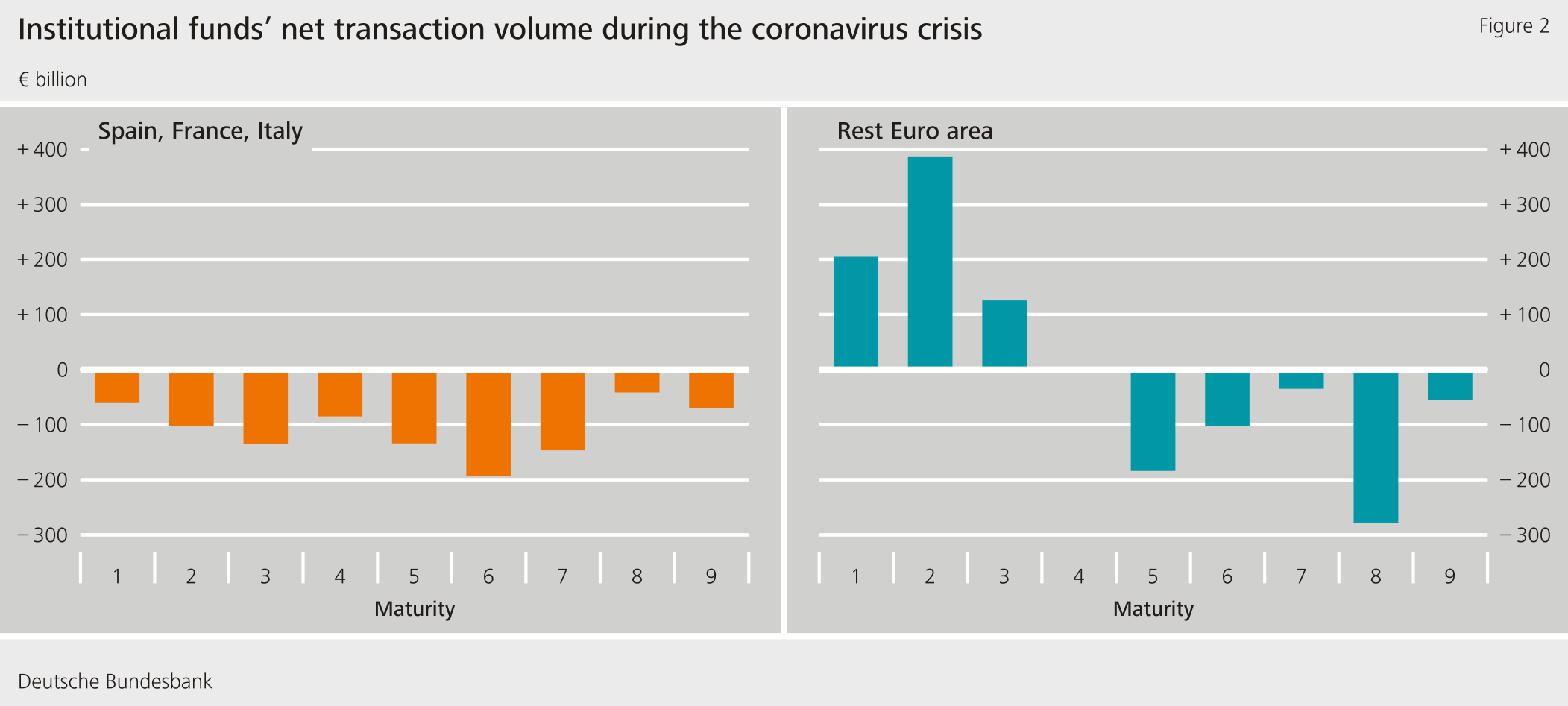

We also observed institutional funds engaging in such procyclical investment behaviour at the beginning of the coronavirus pandemic in February and March 2020. The prices of government bonds issued by the countries initially hit the hardest by the pandemic in the European monetary union (Italy, Spain and France) fell rapidly. At the same time, the prices of bonds issued by countries that were affected to a lesser degree, such as Germany, remained relatively unchanged. Figure 2 shows that German institutional funds sold a total volume of around €1 billion worth of the crisis countries’ bonds within a short period of time, despite bond prices declining sharply in these countries. At the same time, they bought around €300 million worth of sovereign bonds from other euro area countries – primarily bonds with short maturities. This indicates a reduction in risk during times of acute financial market stress, which is usually consistent with an increase in investors’ risk aversion as well as rising risk premiums, and thus confirms the marked procyclical behaviour of German institutional funds, even during the coronavirus crisis.

Figure 2: Institutional funds’ net transaction volume during the coronavirus crisis

Interest rate volatility attributable to reach for yield

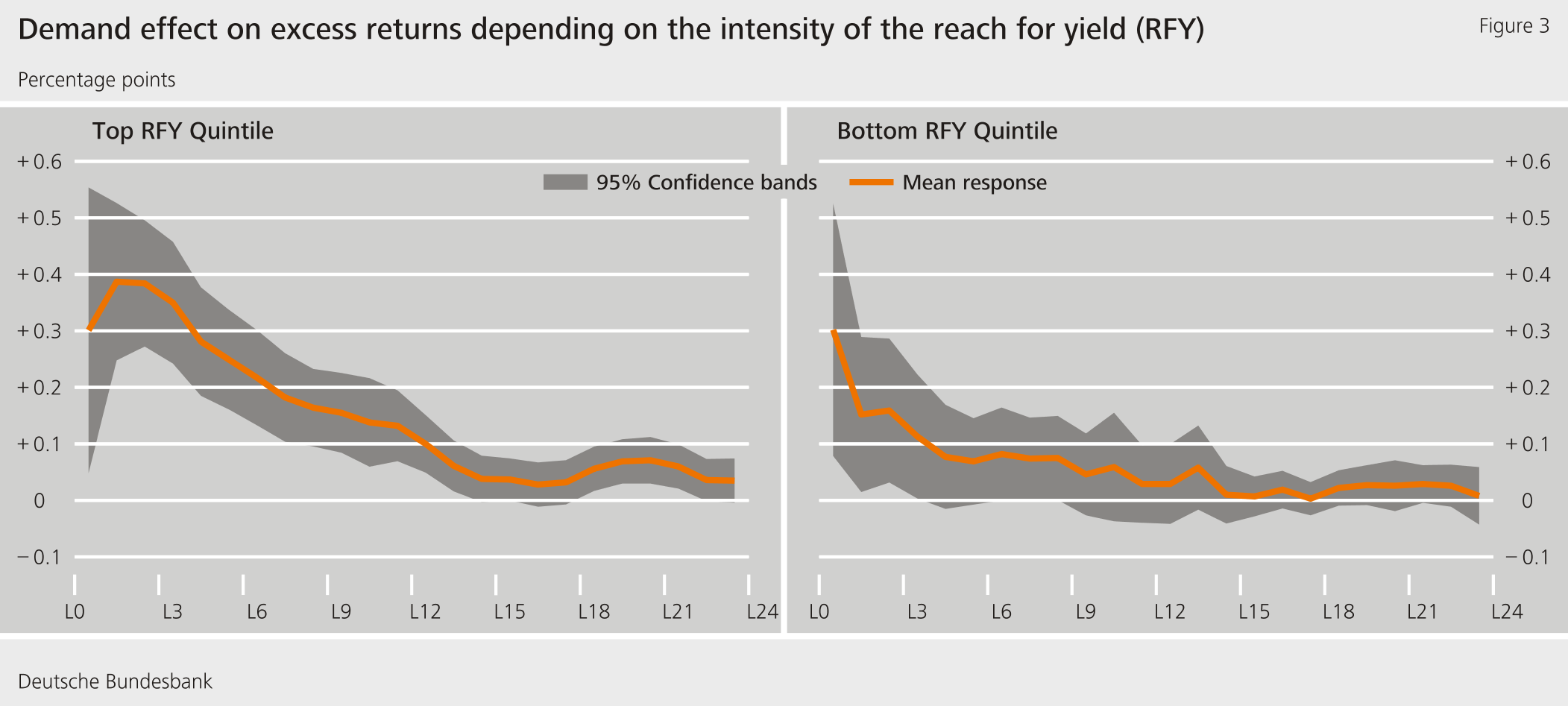

Using individual securities holdings data, we examine whether this procyclical investment behaviour increases asset price volatility. To this end, for the period from 2009, we compare the monthly yields of all European corporate and government bonds held by German institutional funds to the total net purchases of these bonds by German institutional funds in the previous month. This involves controlling for the corresponding net purchases by other sectors, such as banks, credit institutions, insurers and pension funds. Our regression analysis shows that institutional funds have a significant and lasting impact on bond excess returns. This applies especially to funds which are particularly inclined to reach for yield and to bonds with lower ratings or longer maturities. In Figure 3, the chart on the left-hand side shows that net purchases by funds which are in the top 20% of all funds in terms of reaching for yield lead to significant excess returns in the following 12 months. The right-hand chart shows that funds in the bottom 20% have an effect on excess returns that lasts for a shorter period of time only.

Figure 3: Demand effect on excess returns depending on the intensity of the reach for yield (RFY)

Incentives in the fund sector promote the reach for yield

Given their stable liabilities compared with retail funds, institutional funds’ procyclical investment behaviour initially seems puzzling. However, we are able to empirically attribute this behaviour to implicit incentives for fund managers and explicit yield targets.

We demonstrate that implicit incentives for a risky investment strategy arise because institutional investors penalise a less risky investment strategy. Funds with a comparatively low reach for yield within the sector are three times as likely to have their mandate terminated by investors than funds which reach the most aggressively for yield. This effect reverses, however, in times of increased financial market stress and correspondingly higher risk aversion among fund investors, who then increasingly terminate their investment mandates with the funds which were previously operating comparatively aggressively.

Explicit yield targets for fund managers also incentivise the reach for yield, particularly in a negative interest rate environment. Such targets are set, inter alia, by funds which offer a guaranteed return on investors’ capital. Correspondingly, the portfolios of guarantee funds are usually less risky compared with the portfolios of other specialised funds, since guarantee funds try to use their investments in comparatively safe bonds to eliminate losses for their investors. However, negative interest rates pose a challenge for guarantee funds in terms of being able to honour their guarantees. In fact, we are able to demonstrate that guarantee funds are more inclined to reach for yield as the share of negative-yield bonds in their portfolios increases.

Conclusion

Institutional funds manage the bulk of assets under management in Germany. Although these funds have a relatively stable investor structure, their behaviour is strongly procyclical: they buy bonds when their prices rise and sell them when prices fall. Central banks and supervisors are well advised to keep a close eye on specialised funds as this behaviour intensifies asset price volatility.

Disclaimer

The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem.

Literature

Barbu, A., C. Fricke and E. Mönch (2020), Procyclical Asset Management and Bond Risk Premia, Deutsche Bundesbank Discussion Paper No 38/2020.

Becker, B. and V. Ivashina (2015), Reaching for Yield in the Bond Market, The Journal of Finance, Vol. 70, No 5, pp. 1863-1901

Choi, J. and M. Kronlund (2018), Reaching for Yield in Corporate Bond Mutual Funds, The Review of Financial Studies, Vol. 31, No 5, pp. 1930-1965.

Coval, J. and E. Stafford (2007), Asset Fire Sales (and Purchases) in Equity Markets, Journal of Financial Economics, Vol. 86, pp. 479-512.

Guerrieri, V. and P. Kondor (2012), Fund Managers, Career Concerns, and Asset Price Volatility, American Economic Review, Vol. 102, No 5, pp. 1986-2017.

Hanson, S. G. and J. C. Stein (2015), Monetary Policy and Long-term Real Rates, Journal of Financial Economics, Vol. 115, No 3, pp. 428-448.

Emanuel Mönch Head of Research of the Deutsche Bundesbank and Professor of Macroeconomics at the Goethe University Frankfurt

News from the Research Centre

Publications

“Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in theEuropean Economic Review.

“The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in theJournal of Economic Dynamics and Control.