Monetary policy played a pivotal role in the Great Depression Research Brief | 39th edition – March 2021

The root causes of the Great Depression from 1929 to 1933 have been researched extensively. In this context, economic historians view central bank policy as having played a pivotal role, something which empirical modelling often fails to confirm. A new study likewise examines this influence empirically, but more explicitly takes into account the functioning of the international monetary system at the time – the international gold standard.

From 1929 until into the 1930s, the Great Depression caused major economic upheaval around the world. Prices and economic activity slumped in many countries, while unemployment soared.

The causes of this phenomenon have been researched extensively. There is a widespread belief among economic historians that monetary policy played an important role in triggering deflationary developments (Bernanke and James, 1991; Eichengreen, 1992). By contrast, empirical studies that attempt to quantify individual influencing factors using time series models often fail to confirm the significance of central bank policy (Evans et al., 2004). While economic historians consider the workings of the international gold standard as essential, these have hitherto been neglected in empirical work. Against this backdrop, in a new study (Karau, 2020), I analyse the contribution made by monetary policy by focusing on central bank gold demand.

Increased central bank gold demand is deflationary

The monetary system at the time of the Great Depression was very different to the system we know today. Central banks no longer tie their currencies to gold, but instead gear their monetary policy more strongly towards domestic economic objectives. At the time of the gold standard, however, central banks backed a certain share of the currency they issued with gold, promising to exchange their currency for gold at any time at a given fixed rate. As a consequence, exchange rates between different currencies were fixed, too. Theory suggest that in such a system, changes to the degree to which central banks backed their currency by gold determined monetary conditions.

If central banks increased their gold reserve ratios, i.e. putting more gold in their vaults for every unit of currency issued, they reduced the volume of gold in circulation. As a result, less gold was available to the private sector for, say, producing jewellery or for industrial purposes. Whereas in today’s system the price of gold would increase in order to balance supply and demand, this was not possible under the gold standard – after all, the central bank guaranteed a fixed rate between currency and gold. The only way the increased value of gold could materialize was as a drop in all prices of goods expressed in units of currency, i.e. a decline in the price level.

An increase of this kind in the demand for gold by several central banks could indeed be witnessed at the end of the 1920s, with the central banks of France and the United States playing a particularly prominent role. In France, a law passed in the summer of 1928 restricted monetary policy and led to a rise in the Banque de France’s gold holdings (Eichengreen, 1986). At around the same time, also US monetary policy was being tightened. The US Federal Reserve was focusing less closely than before on the international spillover effects of its policy, instead paying greater attention to a supposedly overvalued domestic stock market. This prompted the Fed to raise interest rates several times (Hamilton, 1987). As a result of these developments, large amounts of money flowed to France and the United States, mainly from the United Kingdom. In turn, this put pressure on the Bank of England to likewise tighten its monetary policy.

Functioning of international gold standard crucial for empirical analysis

Why do many economic historians believe that rising demand for gold among individual central banks caused prices to fall around the world? The answer again lies in the workings of the international gold standard. If prices varied strongly from country to country, adjustment processes would kick in: for a certain amount of gold at the established price, traders could buy goods in a country with relatively low prices and sell them in another country where prices are higher. They could then exchange the foreign currency they had earned, minus any transport costs, at the fixed exchange rate for more gold than they had originally invested. Cross-border arbitrage transactions such as these would put pressure on goods prices until, converted into gold, they were roughly aligned (Samuelson, 1980).

However, if countries’ price levels are indeed closely linked (McCloskey and Zecher, 1976, 1984), this means, in turn, that an individual central bank on the gold standard had only a limited influence over domestic prices and economic activity. Instead, the monetary conditions prevailing in each individual country were determined by the monetary policies of all central banks participating in the gold standard (Sumner, 2015). Hence, a key finding in the economic history literature is that individual countries were hardly able to avoid the monetary policy influence of central banks with large gold reserves.

It is by taking into account these aspects that this study differs significantly from the existing empirical analyses of the Great Depression. These often examine changes in the monetary policy stance of individual central banks in isolation and focus on interest rate decisions – as is the norm for today's monetary system. This study, by contrast, measures international monetary conditions in the interwar period with reference to the demand for gold of all major central banks.

Greater demand for monetary gold responsible for falling prices and output

The empirical study is based on a time series model that uses a newly compiled monthly dataset for the period between the two World Wars. Alongside the central banks’ gold reserve ratios, this dataset also contains other variables describing, for example, developments in prices and output in many industrial countries. Structural shocks – i.e. isolated causes for the observed changes in the underlying variables – are identified by sign restrictions, with special attention paid to the aforementioned tightening of monetary policy in the US and France in mid-1928.

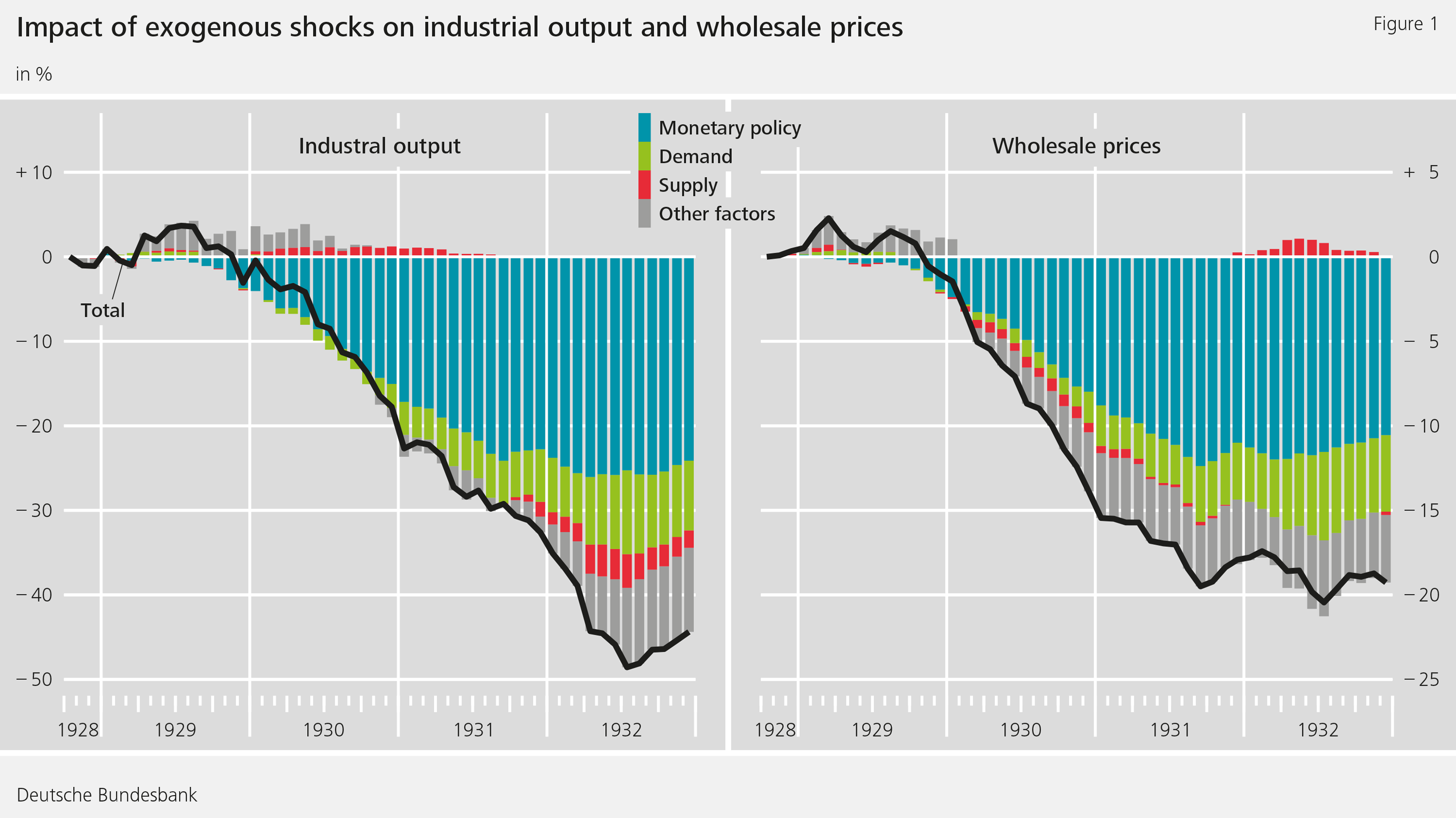

The analysis reveals that monetary policy shocks in the form of higher monetary gold demand can indeed explain much of the international decline in economic activity at the beginning of the crisis. The black lines in Figure 1 show developments in industrial output in numerous industrial countries from October 1928 to December 1932 (left) and developments in wholesale prices (right). The evolution actually observed during the crisis is presented as a deviation from a hypothetical baseline portraying how, according to the model, the variables would have developed had no shocks occurred. The variously coloured bars illustrate the different contributions made by the identified shocks. The model calculations indicate that, particularly at the start of the economic downturn, unexpected changes in monetary policy (blue bars) were by far the most important driving force behind the decline. Other factors do not start to significantly gain in importance until more than a year after the downturn commenced. These are modelled less explicitly, but are most likely connected to the banking crises and restrictions on international goods trade that occurred in the early 1930s.

Conclusion

Monetary policy factors are considered one of the main causes of the Great Depression in the 1930s. However, so far their significance could hardly be verified using statistical models. This study takes explicit account of the workings of the gold standard that prevailed at the time and supports the hypothesis that central bank policies played an important role in the crisis – especially for the initial downturn.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Bernanke, B. and James, H. (1991). The Gold Standard, Deflation, and Financial Crisis in the Great Depression: An International Comparison. In Hubbard, R.G., editor, Financial Markets and Financial Crises, pp. 33-68. National Bureau of Economic Research.

- Eichengreen, B. (1986). The Bank of France and the Sterilization of Gold, 1926-1932. Explorations in Economic History, 23(1):56-84.

- Eichengreen, B. (1992). Golden Fetters: The Gold Standard and the Great Depression, 1919-1939. NBER Books. National Bureau of Economic Research.

- Evans, P., Hasan, I., and Tallman, E. W. (2004). Monetary Explanations of the Great Depression: A Selective Survey of Empirical Evidence. Economic Review, (3):1-23.

- Hamilton, J. D. (1987). Monetary Factors in the Great Depression. Journal of Monetary Economics, 19(2):145-169.

- Karau, S. (2020). Buried in the Vaults of Central Banks – Monetary Gold Hoarding and the Slide into the Great Depression. Bundesbank Discussion Paper 63/2020.

- McCloskey, D. N. and Zecher, J. R. (1976). How the Gold Standard Worked, 1880-1913. In Frenkel, J. and Johnson, H., editors, The Monetary Approach to the Balance of Payments. George Allen and Unwin.

- McCloskey, D. N. and Zecher, J. R. (1984). The Success of Purchasing Power Parity: Historical Evidence and Its Implications for Macroeconomics. In: Bordo, M. and Schwartz,

- A., A Retrospective of the Classical Gold Standard, 1821-1931. National Bureau of Economic Research.

- Samuelson, P. (1980). A Corrected Version of Hume’s Equilibrating Mechanism for International Trade. In Chipman, J. and Kindleberger, C., editors, Flexible Exchange Rates and the Balance of Payments. North Holland, Amsterdam.

- Sumner, S. (2015). The Midas Paradox: Financial Markets, Government Policy Shocks, and the Great Depression. Independent Institute.

The author |

|

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein