Dynamics in the crude oil market dictated by the manufacturing sector Research Brief | 40th edition – May 2021

It is often said that industry in oil-importing countries is especially hard hit when oil prices climb. However, a new study reveals that the manufacturing sector actually often does well during episodes of elevated oil prices. This is because, from a global perspective, that particular sector is a driving force behind oil price movements. The manufacturing sector’s healthy performance thus bolsters the economy of oil-importing countries in times of rising oil prices. Conversely, industry often exerts negative effects when oil prices fall.

Why do oil prices fluctuate and what are the macroeconomic implications of such fluctuations? These are questions that have long occupied economic researchers. Until the beginning of the 2000s, the prevailing view was that oil prices were primarily determined by unexpected changes in crude oil production. In the meantime, however, the idea that shifts in demand also play a significant role for the oil market has become established. The distinction between demand-driven and supply-driven changes in oil prices is an important one. If, for instance, a pick-up in economic activity in some parts of the world occasions a hike in demand for oil, the economy of oil-importing countries tends not to be negatively impacted by the rise in oil prices (see, for example, Kilian 2008 and Bodenstein et al. 2012).

In a new study, I take a closer look at what drives fluctuations in oil demand. In particular, I explore the significance of the prevailing economic conditions in the manufacturing sector. After all, this is a sector which is comparatively oil-intensive, not only in terms of production but also because of its reliance on transport services. A cursory look at the path traced by the data is enough to suggest that there is an important relationship at play: oil prices typically climb when manufacturing output – in particular relative to activity in the services sector – tracks upwards. Conversely, oil prices mostly decline when manufacturing output wanes (see Khalil 2020).

To conduct a deeper analysis, I employ an estimated general equilibrium model with three regions (United States, Organization of the Petroleum Exporting Countries – OPEC, rest of world), covering the period from 1974 to 2019. The model distinguishes between the manufacturing sector and the services sector and captures crude oil production as well as crude oil inventories. Unlike services, the manufacturing sector is tied into international trade, including in the form of cross-border value chains.

Manufacturing is the key force driving oil price movements

My findings suggest that, in the period under review, industrial activity was the most important source of fluctuations in demand for oil. This is partly because the manufacturing sector makes heavy use of manufactured intermediate goods. Packaging is one example, but more complex components are involved too. Demand for such inputs typically fluctuates strongly and, according to the estimations, firms’ call for crude oil is always higher when they utilise more manufactured intermediate inputs.

Another factor is that oil prices climb when demand for manufactured final goods picks up unexpectedly. This applies to private consumer goods and – although these are not captured in the model in detail – capital goods, such as machines or commercial vehicles. Production of final goods is very oil-intensive and utilises manufactured goods as inputs, which themselves are closely tied to oil demand.

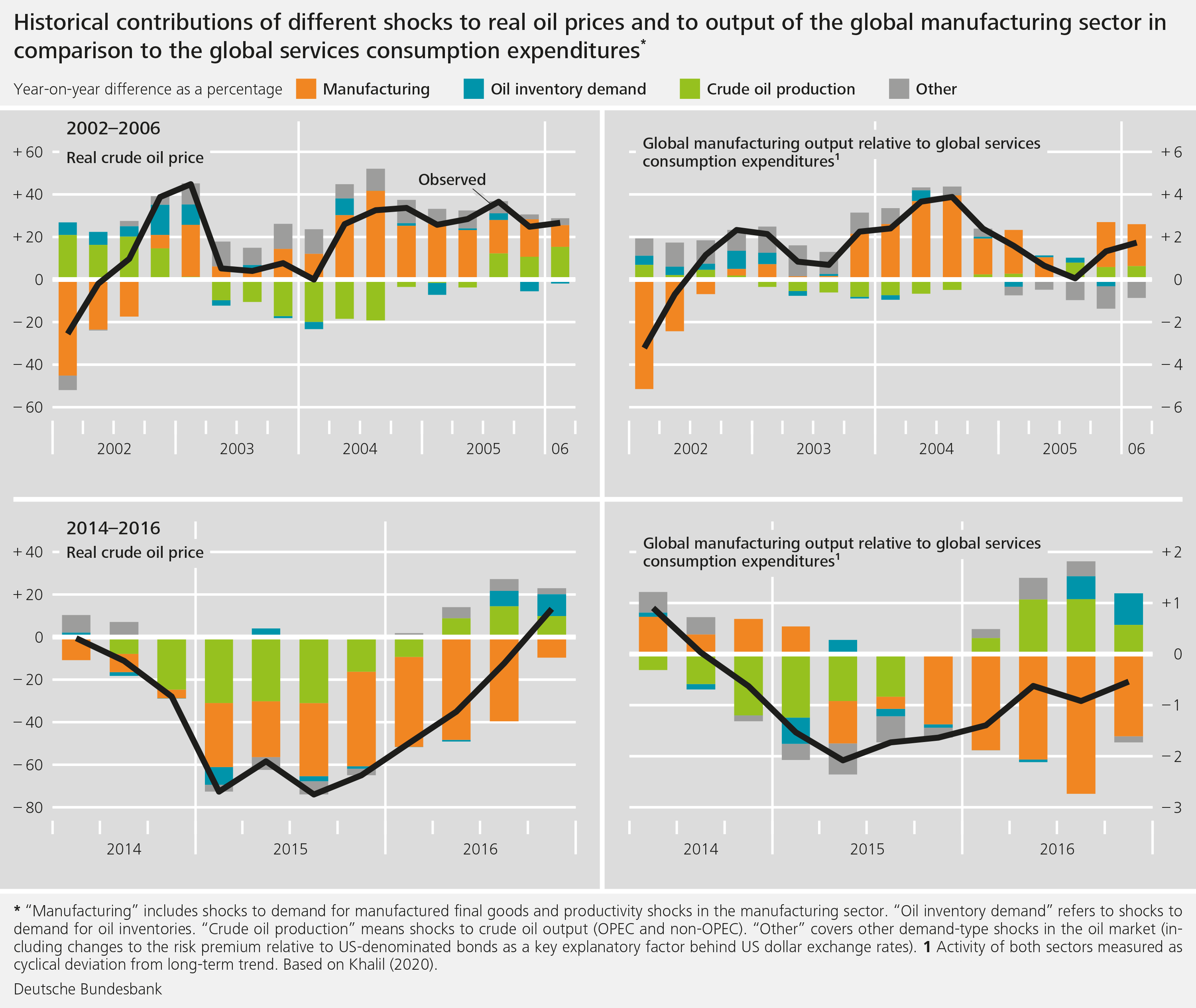

Two periods in the 2000s serve to illustrate these interlinkages. Between 2002 and 2006, oil prices climbed steeply due to significantly increased demand for manufactured intermediate inputs and final goods (consumer goods and capital goods) worldwide. In spite of rising costs for crude oil, the manufacturing sector expanded rather considerably relative to the services sector (see the top panels of the chart).

The period spanning mid-2014 to 2016 is also of interest (see the bottom panels of the chart). Oil prices stayed low for a long time, not least because of a global slowdown in activity in the manufacturing sector. Interestingly, the unexpected increase in global crude oil production – which the estimations identified as one of the main reasons for the slump in oil prices – also depressed manufacturing output significantly up to mid-2015. The associated income losses experienced by the OPEC countries dampened their imports of industrial goods. According to the model, these demand losses eclipsed the positive effects for the sector stemming from the lower oil prices.

Sectoral shifts in the oil importing countries when oil prices change

Significant price changes in the global oil market are accompanied by sectoral shifts in the oil importing countries. This was the case in the United States between the end of 2002 and 2006, a time when the export sector in particular – and, with it, manufacturing – enjoyed robust demand for goods the world over. By contrast, the estimates indicate that the services sector actually even suffered at times in this setting because private consumption fell. In the model, the latter sinks when short-term interest rates are raised on the back of higher inflation rates. The stronger upward pressure on prices results not only from higher oil prices but is also a product of climbing wages and rising prices for manufactured intermediate inputs. The upshot is that, overall, countervailing sectoral influences mean that the ups and downs of the crude oil market do not necessarily exert a particularly strong effect on the economy as a whole nor push it in the direction often assumed. Barely any positive impulses for US gross domestic product are apparent for the period between 2014 and 2016 – a phase where oil prices declined – and they are even distinctly negative in 2016.

These results are also of relevance for Germany, where manufacturing plays a highly significant role. The past few months are a testament to that fact. While measures to contain the pandemic once again put pressure on the global services sector from the autumn, global manufacturing was largely spared, with world industrial output even outstripping pre-pandemic levels of late. The price of crude oil has also picked up considerably once more. German industry benefited significantly from global economic developments and was able to cope well with rising oil prices.

Conclusion

The cyclical driving forces of the manufacturing sector are the most important cause of oil price fluctuations. In part due to trade links, it is in fact this sector that performs well in oil-importing countries when oil prices are high, while the services sector tends to lose out. On the whole, the macroeconomic effects exerted by movements in the oil market are therefore often relatively small, however.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Bodenstein, M., L. Guerrieri, and L. Kilian (2012). Monetary policy responses to oil price fluctuations, IMF Economic Review 60 (4), 470-504.

- Khalil, M. (2020). Global oil prices and the macroeconomy: The role of tradeable manufacturing versus nontradeable services. Bundesbank Discussion Paper 67/2020.

- Kilian, L. (2008). The economic effects of energy price shocks. Journal of Economic Literature 46 (4), 871-909.

| The author |

© Nils Thies

Research economist, Deutsche Bundesbank, Directorate General Economics |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein