Inflation – lessons learnt from history

The potential consequences of inflation demonstrate how important it is to keep the value of a currency stable.

The German Empire experienced hyperinflation and hidden inflation during and after both world wars. West Germany also saw comparatively high inflation rates in the 1970s.

Inflation and hyperinflation in Germany 1914-23

In 1923, during the months of hyperinflation, the value of the German currency fell at such a rate that in many places wages were being paid daily. People collected notes in bags and suitcases and crowded into shops to exchange their money for goods as quickly as possible. Since the value of the Mark was declining rapidly virtually on a daily basis, traders were constantly increasing their prices. Many began to sell goods and services only in exchange for food and coal; others closed their businesses altogether. This led to social tensions.

A policy of inflation emerged following the outbreak of war in 1914. German banknotes were no longer redeemable in gold; they could now be covered by government bonds in place of gold. Instead of financing the costs of war through higher taxes, the government borrowed from the German population, and increasingly from the Reichsbank, which in turn printed more and more banknotes.

By the time the war had ended in 1918, the German government faced serious financial problems. In addition to domestic war debt in the form of the war bonds that had been issued, social spending needed to be high in order to stabilise the German Reich, which was politically, socially and economically shattered. Moreover, the victorious powers were demanding large reparation payments. The government borrowed increasingly large amounts from the Reichsbank, which put more and more money into circulation. This was not matched by growth in the supply of goods in Germany, and huge price increases resulted.

As galloping inflation became hyperinflation in 1923, the currency could no longer function as a general means of payment or store of value. The government introduced currency reform, replacing the Mark with the Rentenmark in November 1923. Inflation had almost completely devalued all financial assets and liabilities that had been in Mark. The state benefitted most from this because the sum of all German war debt, valued at 154 billion Mark, dropped to just 15.4 Pfennig on the day the Rentenmark was introduced.

Hidden inflation in Germany 1936-48

The German government financed the Second World War by borrowing from the central bank, together with a major expansion of the money supply. Price freezes, wage controls, rationing and coupons kept inflation hidden. Nevertheless, the huge depreciation of the currency in 1948 led to currency reform, under which the Deutsche Mark was introduced. The exchange rate was fixed at 1 Deutsche Mark to 10 Reichsmark. Savers and holders of financial assets found that, to a large extent, they had been expropriated.

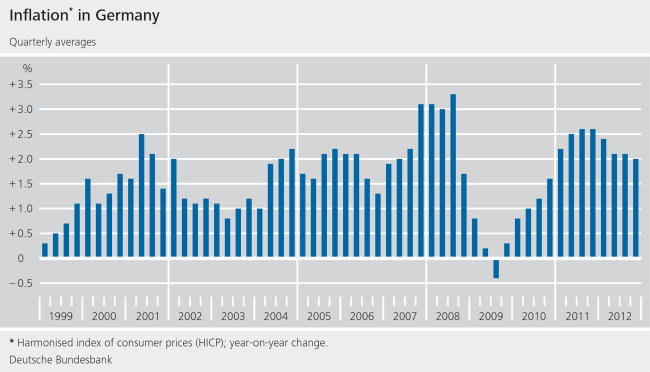

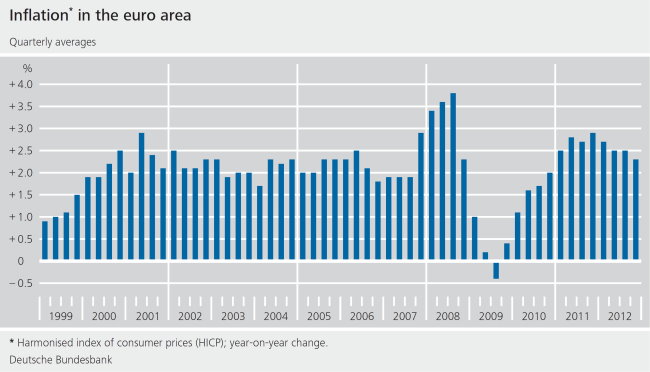

Global inflation in the 1970s and 1980s

From the early 1970s to the mid-1980s, the industrialised countries saw inflation rise to high levels. There were several reasons for this. The US Federal Reserve was already using a policy of low interest rates in the 1960s in order to finance the country’s budget deficit, which was progressively increasing as a result of the costs of the Vietnam War and extensive social reforms. The policy was also intended to stimulate an economy that was bogged down in recession. The high demand for goods and services that was triggered as a result led to increases in wages and consumer prices.

Lessons learnt from history