Monthly Report: Bundesbank sees benefits in blockchain technology

The Deutsche Bundesbank’s latest Monthly Report looks at distributed ledger technology (DLT). The Bundesbank's experts investigate whether DLT, which was originally developed for the Bitcoin virtual currency, offers any potential for the financial sector. Their analysis focuses chiefly on what DLT might mean for payments and securities settlement.

The pros of DLT

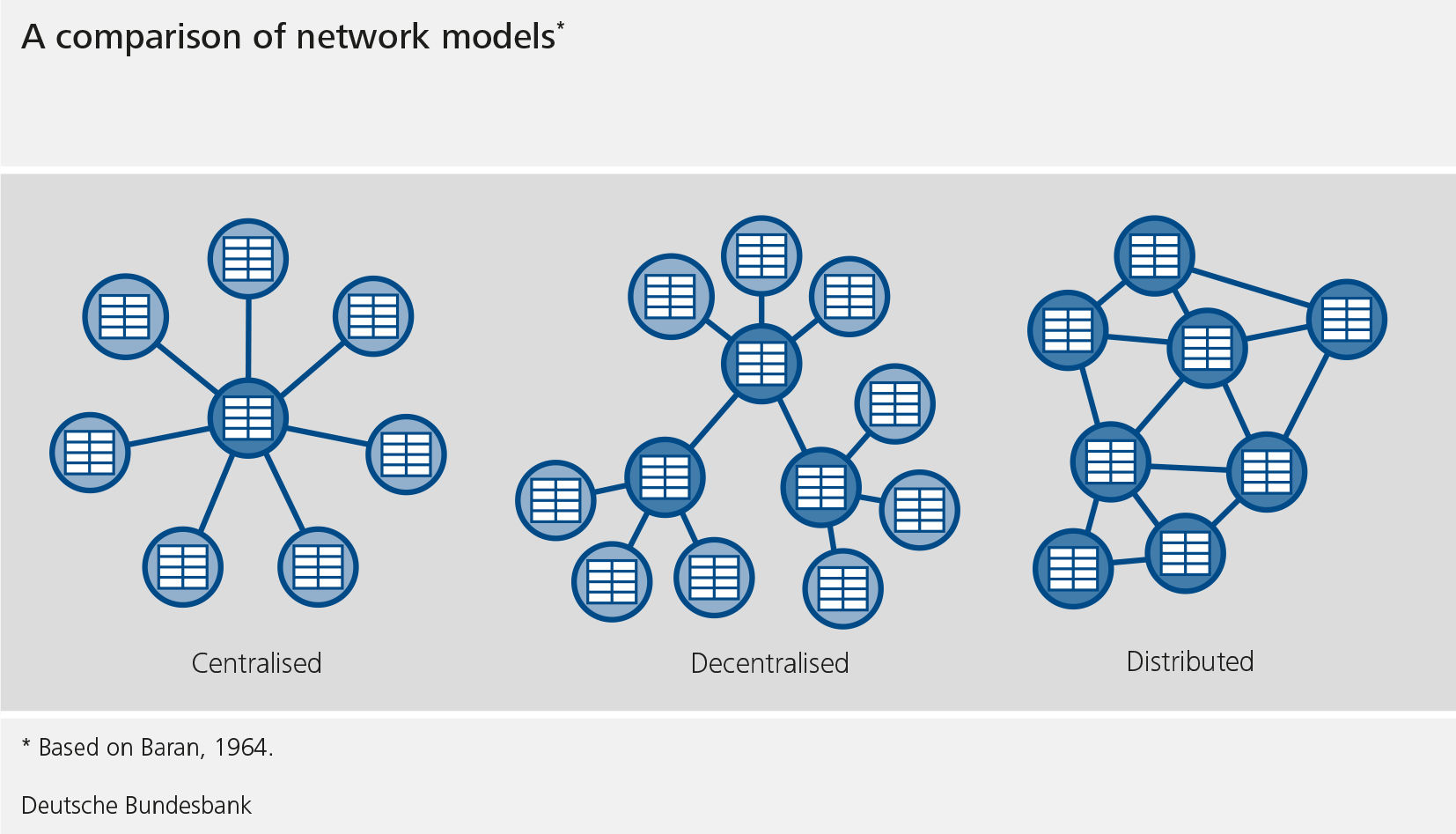

Payments hitherto have, for the most part, been settled using centralised architecture, where only a single authority that is considered trustworthy has the right to alter data such as account balances with legally binding effect. That authority, then, runs the ledger. In decentralised network models, meanwhile, multiple entities – each of which have access to the information – have the right to update data. DLT, on the other hand, uses a distributed database (a "distributed ledger") which gives every participant in the network ("nodes") the same rights to write, read and store data.

"Potentially, DLT offers a number of benefits on account of the distributed storage of data, which can eliminate reconciliation processes associated with complex work-sharing value added chains,"

the Bank’s payment specialists write, adding that DLT might also improve transparency and potentially offer superior protection against cyber attacks. This is because DLT enables settlement to continue even if, for instance, one of the nodes failed or were blocked. The Bank's specialists do, however, also see a number of challenges. These include confidentiality issues, the need to establish the identity of users (which is especially important for tackling money laundering), and the question of how the assets transferred via the blockchain can be reliably matched with "real world" assets and by whom. The experts note that points of reference in the real world are irrelevant for Bitcoin, which is still the best-known DL network, given that Bitcoins are merely virtual and do not exist outside the blockchain. The Monthly Report article expands upon these insights by investigating what potential DLT might offer for the individual areas of the financial sector.

DLT in payments

The Bundesbank’s experts see little prospect of DLT being put to widespread use in the field of individual and retail payments given the current state of the art. Particularly for payments within the euro area, they argue, the systems in operation have already been optimised for fast transfers and require a minimum of reconciliation, besides being able to process millions of transactions with ease every day.

Yet for all these advantages which the new technology might offer in the world of payments, putting it to use will arguably present some major challenges. Certain special conditions apply in the financial industry. For one thing, payments have to be settled with immediate finality, while in the case of decentralised systems, some reconciliation processes first need to take place between participants. That, the Bundesbank’s experts write, is why DLT, above all in its Bitcoin format, requires extensive modification if it is to be adapted to suit the needs of the financial sector.

Streamlining securities settlement

The Monthly Report article also investigates whether DLT has any potential uses in the settlement of securities. Compared to payments, traditional settlement operations involve a far greater number and variety of intermediaries. These include securities traders, exchanges and clearing houses. Given the complexity, arduous reconciliation and error-prone nature of manual processes, this is an area where DLT could offer some benefits, as it has the technical capability to reduce securities settlement to just a few process steps. "If two nodes make a matching declaration in the distributed ledger, the entry in the distributed ledger could be simultaneously interpreted as the trade, clearing, settlement and accounting," the Bank’s experts write, adding that the nodes can all access the same data pool. They concede, however, that it is still unclear whether DLT also has the edge over today’s technology in terms of security, efficiency, costs and speed.

Central bank-issued digital currency

Another topic the Bundesbank experts explore is whether the use of DLT could be flanked by the provision of central bank-issued digital currency. In their view, the repercussions of central bank-issued digital currency very much depend on its specific features. Probably the most pressing question here is whether central bank-issued digital currency should be issued to non-banks as well. However, the implications of central bank-issued digital currency for monetary policy and financial stability and for the structure and business models of banks are hard to fathom, the Monthly Report explains, which is why there is currently no realistic prospect of central bank-issued digital currency being rolled out in the foreseeable future. In current payment systems, market participants insist on settlement in central bank money for large amounts. Hitherto, that can take the form of overnight deposits with the central bank or currency in the shape of banknotes and coins.

Joint Bundesbank/Deutsche Börse research project

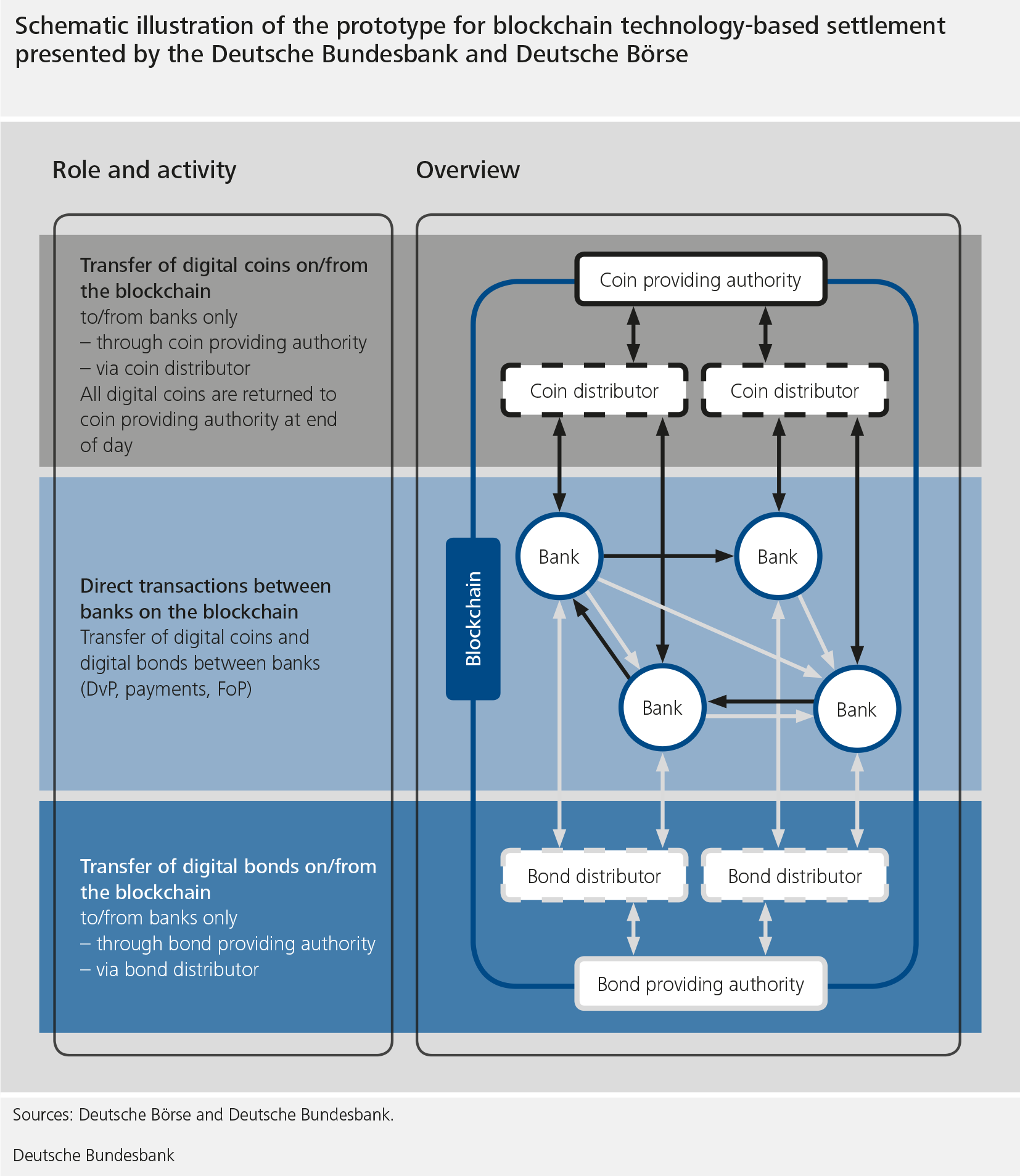

The Bundesbank has been getting to grips with the topic of DLT on account of its special statutory mandate, which requires the Bank to develop and operate payment and settlement systems and to act as a catalyst in forging improvements in payment operations. It furthermore monitors the stability of systems and tools used in the field of payments and settlement. As part of its analysis of blockchain technology, the Bundesbank has been running trials in conjunction with Deutsche Börse on a jointly developed prototype.