Monthly Report: How climate policy influences equity prices

As outlined in the report, the 5,285 stock corporations included in the analyses are domiciled in 75 countries from various regions of the world, where their businesses are subject to the prevailing national climate policies. Together they account for more than half of global stock market capitalisation and are responsible for 17-20% of global greenhouse gas emissions. For the calculations, the companies – and the emissions they account for – were each assigned to one of twelve regions based on where the parent company is headquartered.

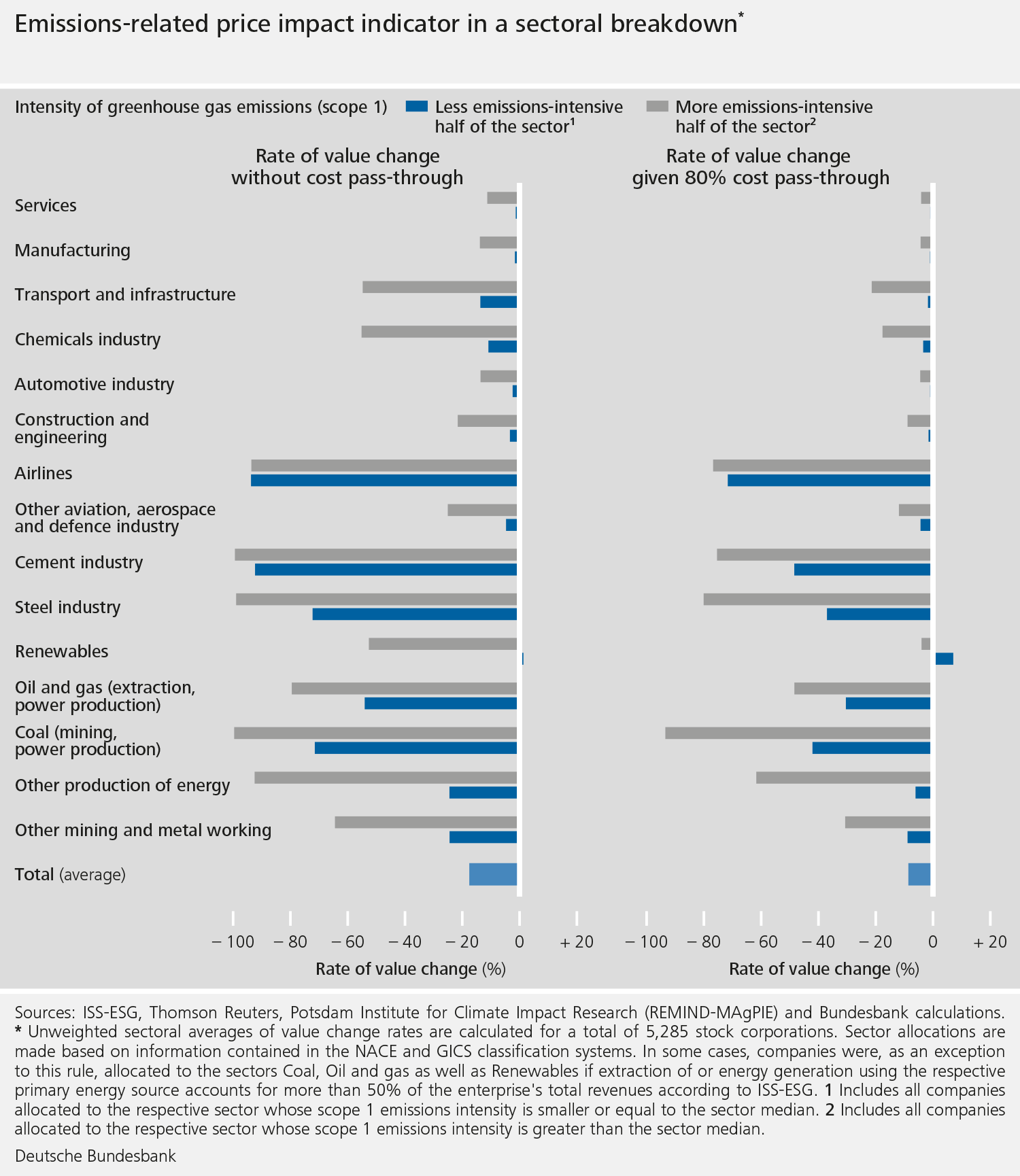

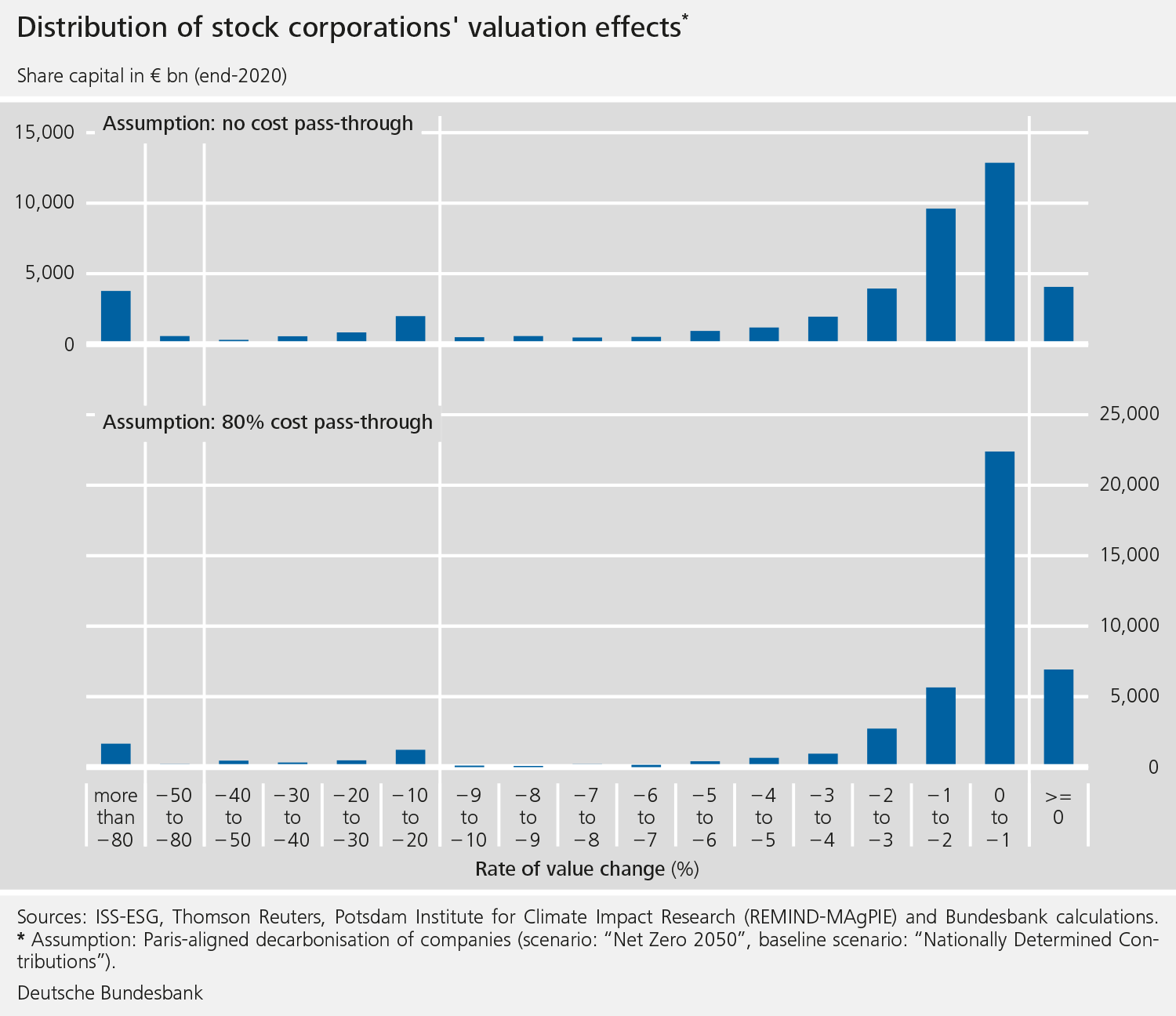

Large proportion of stock corporations suffers only small losses

The result of their analyses: given Paris-aligned decarbonisation and a correspondingly sharp rise in carbon prices, a large number of the companies under review can expect only small emissions-related equity price losses. At the same time, more than one-tenth of capitalisation – €4.7 trillion or 15% of all companies – suffers losses of more than 50% of the company’s value, the economists write. Meanwhile, 78% of the total market capitalisation is left unscathed by emissions-related share price losses of more than 4%.

Those stock corporations whose remaining greenhouse gas emissions cause them high costs in relation to their expected dividends, in particular, suffer large losses in value. Companies whose business activities are centred around fossil fuels will be strongly affected, the Bundesbank explains. “They may face the risk of stranding even if they reduce emissions in compliance with the Paris Agreement,

” so the report. An asset is said to be stranded prior to the end of its useful economic life – as expected at the time of investment – if it can no longer yield any economic return and thus loses its entire value.

Regional carbon price is key

“Climate-related valuation changes and the question of climate-related stranding of certain assets are therefore likely to play an important role in the financial markets going forward

,” the Bundesbank writes. With regard to “green” structural change or the transition to a low-carbon economy, stranding of certain business models may, however, be essential if the goal is the efficient use of funds for necessary investment in financial markets.

Footnotes: