Monthly Report: The role of ANFA in implementing monetary policy

In its March Monthly Report, the Bundesbank states that the publication of ANFA by the ECB at the beginning of February 2016 was to be welcomed. "Transparency promotes central banks' credibility and, by extension, trust in their ability to fulfil their monetary policy tasks in a sustainable manner."

ANFA explained

ANFA is designed to safeguard monetary policy. Since early 2003, ANFA has regulated to which extent the national central banks (NCBs) are allowed to conduct operations on their own responsibility and liability as part of their national tasks. Such operations include the accumulation of reserve assets or pension provisions for employees, but also the creation of own funds portfolios for general investment purposes or the acceptance of government deposits or deposits from other central banks and international institutions. In this context, the NCBs are authorised to make purchases of government and collateralised bonds, for example. In contrast to the monetary policy operations the NCBs conduct as a result of their membership in the Eurosystem, these operations carried out on their own responsibility and liability are referred to as non-monetary policy operations.

Up until now, the agreement was treated confidentially. In public discussions, the ECB and the Eurosystem as a whole were therefore lambasted for lack of transparency. In its Monthly Report, the Bundesbank describes the situation as follows: "For instance, non-monetary policy securities purchases (particularly of domestic government bonds) made by the individual NCBs were linked to monetary financing, which is prohibited by the European Treaties – with emphasis on the extent to which such portfolios grew as the European sovereign debt crisis unfolded."

The ECB has responded to these allegations by making the agreement public.

The Bundesbank Monthly report goes on to outline the ways in which ANFA regulates the non-monetary policy operations of the NCBs within the Eurosystem. One is by imposing ceilings on such operations. Another is by determining the maximum overall volume of what are known as net financial assets (NFA) in the Eurosystem; in the context of ANFA, the generic technical term NFA is used for all non-monetary policy operations on the assets and liabilities side of the balance sheet. Put simply, ANFA allocates all non-monetary policy operations among the NCBs in proportion to their shares in the ECB's capital key.

Necessary agreement

In addition, the Monthly Report explains why this agreement between the Eurosystem central banks became necessary 13 years ago. One of the main reasons was the realisation that, taken together, all non-monetary policy operations could potentially impact on the single monetary policy of the Eurosystem by affecting what is referred to as the banking sector's liquidity position vis-à-vis the Eurosystem. The NCBs' balance sheets play a key role in this context.

When a central bank conducts operations which are reflected in its balance sheet, this creates central bank money (ie cash and sight deposits) which, for example, commercial banks hold with the central bank. By providing more or less of this money, central banks are able to control the total amount of money available on the market. When experts use the term "liquidity" provided or taken away from commercial banks by the central bank, they mean central bank money.

As a rule, a central bank ought to be keen to maintain a structural liquidity deficit in the banking sector as commercial banks may be expected to demand liquidity from the central bank. If this is the case, it is easier for a central bank to implement its monetary policy measures more effectively. This includes setting the interest rate level at which central banks grant commercial banks credit (ie liquidity). In this context, the Bundesbank Monthly Report states that "a structural liquidity deficit makes it easier to steer short-term interest rates in monetary policy terms as it forces banks to turn to central bank funding"

.

The Eurosystem, which is responsible for the monetary policy of the European monetary union, likewise generally aims to maintain a structural liquidity deficit vis-à-vis the banking sector. Against this backdrop, the NCBs and the ECB signed the ANFA at the beginning of 2003. The objective of the agreement is to ensure that the liquidity effects from the operations carried out by the NCBs as part of their national functions are consistent with the monetary policy aims of the Eurosystem.

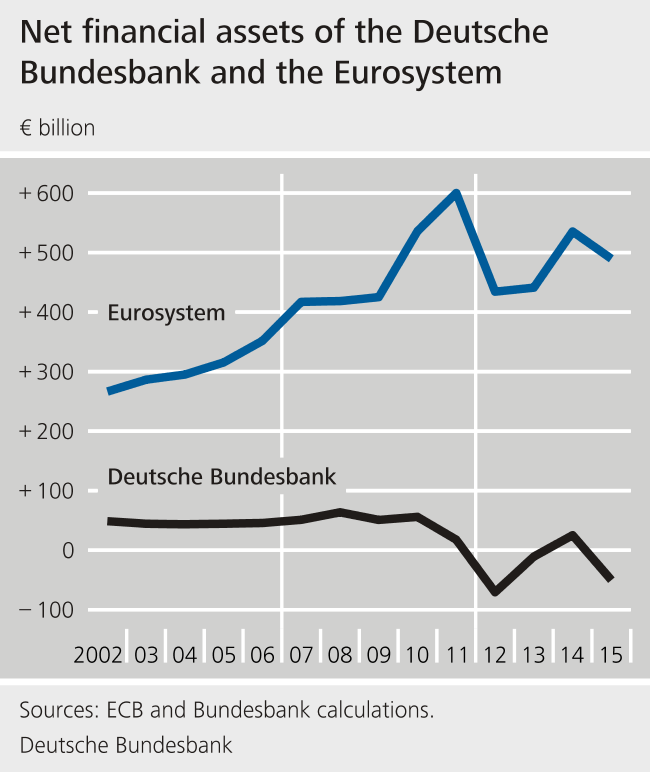

Volume of Bundesbank's ANFA assets relatively low

"Comparatively speaking, the non-monetary policy securities portfolios of other Eurosystem NCBs tend to be larger in scope and therefore also have a greater impact on changes in these central banks' NFA,"

wrote the Bundesbank's economists in the latest issue of the Monthly Report. Indeed, the Eurosystem's total NFA holdings rose continuously between 2002 and 2011 from €267 billion to €600 billion. These holdings subsequently slumped once again but still amounted to €490 billion at the end of 2015. As at the end of March 2016, they stood at €347 billion.

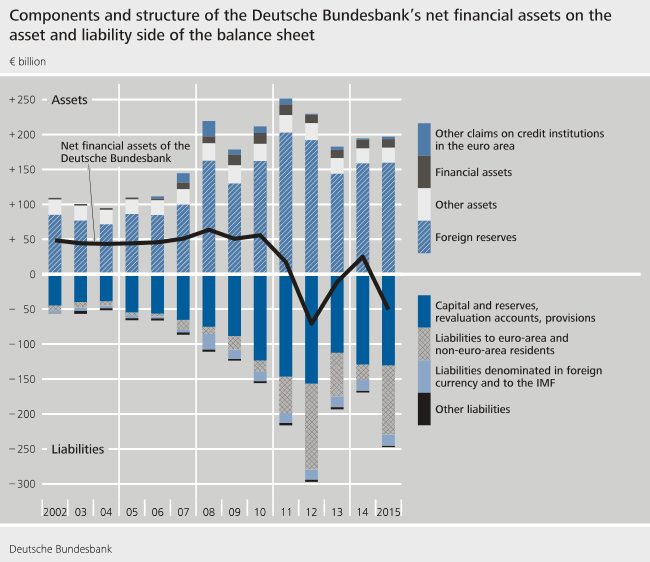

The fact that the NCBs conduct operations for their own account and purposes even after their entry into the euro area can be traced back to the unique legal environment in which they are operating. On the one hand, European Union law governs all matters pertaining to the goal of achieving a single monetary policy for the euro area as a whole, as these tasks were transferred to the Community level when monetary union was founded. Open market operations conducted by the NCBs on the Eurosystem's behalf are one example of operations that take place in this framework. On the other hand, however, the NCBs are allowed to perform tasks arising from national legislation in their respective home countries - provided such tasks do not interfere with monetary policy.

Although the NCBs therefore make a major contribution to monetary union, they have no autonomy when it comes to performing tasks outside the realm of monetary policy. Consequently, it could be said that the Bundesbank serves as the Federal Government's fiscal agent, which is why inflows and outflows of government deposits also have an impact on its balance sheet. It also manages the national reserve assets, consisting of gold, foreign exchange reserves and claims on the International Monetary Fund.

You can find out more about ANFA, also in the light of the Eurosystem's currently expansionary monetary policy, in the article entitled "The role and effects of the Agreement on Net Financial Assets in the context of implementing monetary policy" in the Bundesbank's March 2016 Monthly Report (pages 83 to 93).