Purchase programmes affect Germany’s TARGET balance

Bundesbank economists have studied the factors that have influenced Germany’s TARGET balances over the past 20 years. The results show that the growth of the balances can be divided into four periods. The decline in German TARGET claims in 2018 and 2019 was due in large part to lower and, for a time, discontinued net asset purchases of the Eurosystem, write the Bundesbank’s experts in the current edition of the Bundesbank’s Monthly Report.

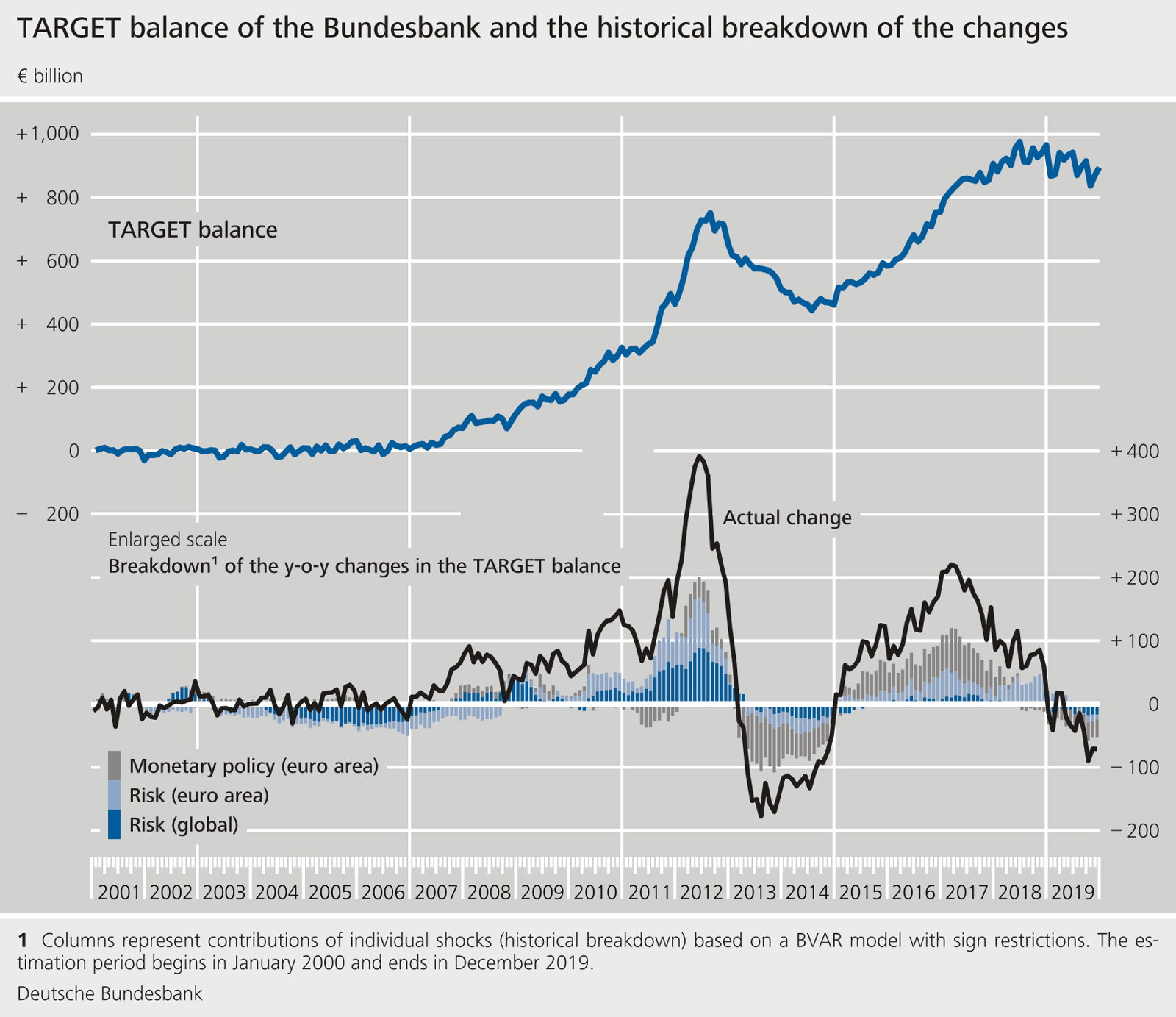

TARGET balances are a national central bank’s claims on (positive TARGET balance) or liabilities towards (negative TARGET balance) the European Central Bank. They occur mainly when commercial banks or central banks settle cross-border transactions in central bank money using the TARGET2 payment system. If the sums of such claims and liabilities between central banks do not balance out over the course of a day, they are netted out at the end of the business day to form a single claim on, or liability towards, the ECB for each national central bank. Thus, each national central bank has just one TARGET2 claim on, or liability towards, the ECB. The Bundesbank’s TARGET balance is positive, which means that the Bundesbank possesses claims on the ECB.

Rising TARGET balance during the financial and sovereign debt crisis

According to the Bundesbank’s experts, during the first period following the launch of the euro, the national balances of the Eurosystem moved at a low level with frequently changing signs. “The cross-border redistribution of liquidity in the euro area took place overwhelmingly through the private interbank market,”

write the economists.

The second period began with the outbreak of the financial crisis in 2007-08 and led to an expansion of the German balance. As private commercial banks became increasingly mistrustful of each other during the financial crisis, the interbank market largely collapsed. The Governing Council of the ECB then adopted a series of non-standard monetary policy measures for the first time in order to continue supplying commercial banks with central bank money. This accommodative monetary policy and the increasing global risks do not entirely explain the moderate rise in the German balance, according to the Monthly Report. In the second quarter of 2010, the TARGET balances expanded again, and this process strengthened in the following year. The economists write that this was due to increasing uncertainty in the euro area caused by the European sovereign debt crisis. An additional factor was that a generous amount of central bank money had been made available, which was utilised to varying degrees by the commercial banks in different European countries.

Purchase programmes affect the TARGET balances

The announcement by Mario Draghi, who was ECB President at the time, that the ECB was ready to do whatever it took to preserve the euro was followed by a resurgence in the financial markets’ confidence in the continued existence of the euro, and the German TARGET balance went down. The fourth period began in 2014 with a renewed rise. According to the Monthly Report, German TARGET claims reached an all-time high of almost €1 trillion in mid-2018. “However, this increase was not linked to a European or global financial crisis,”

write the experts; instead, it reflected the impact of the Eurosystem’s asset purchases.

“The estimation results confirm the suspicion that the renewed positive TARGET flows between 2015 and 2017 were chiefly attributable to European monetary policy (i.e. the Eurosystem’s asset purchase programme) and only to a lesser extent to the risk assessment within the euro area,”

write the authors of the Monthly Report article. Moreover, the results suggest that a large part of the decline in German TARGET claims recorded in 2018 and 2019 can likewise be ascribed to European monetary policy – but now to tapering and, ultimately, discontinuing the net asset purchases.