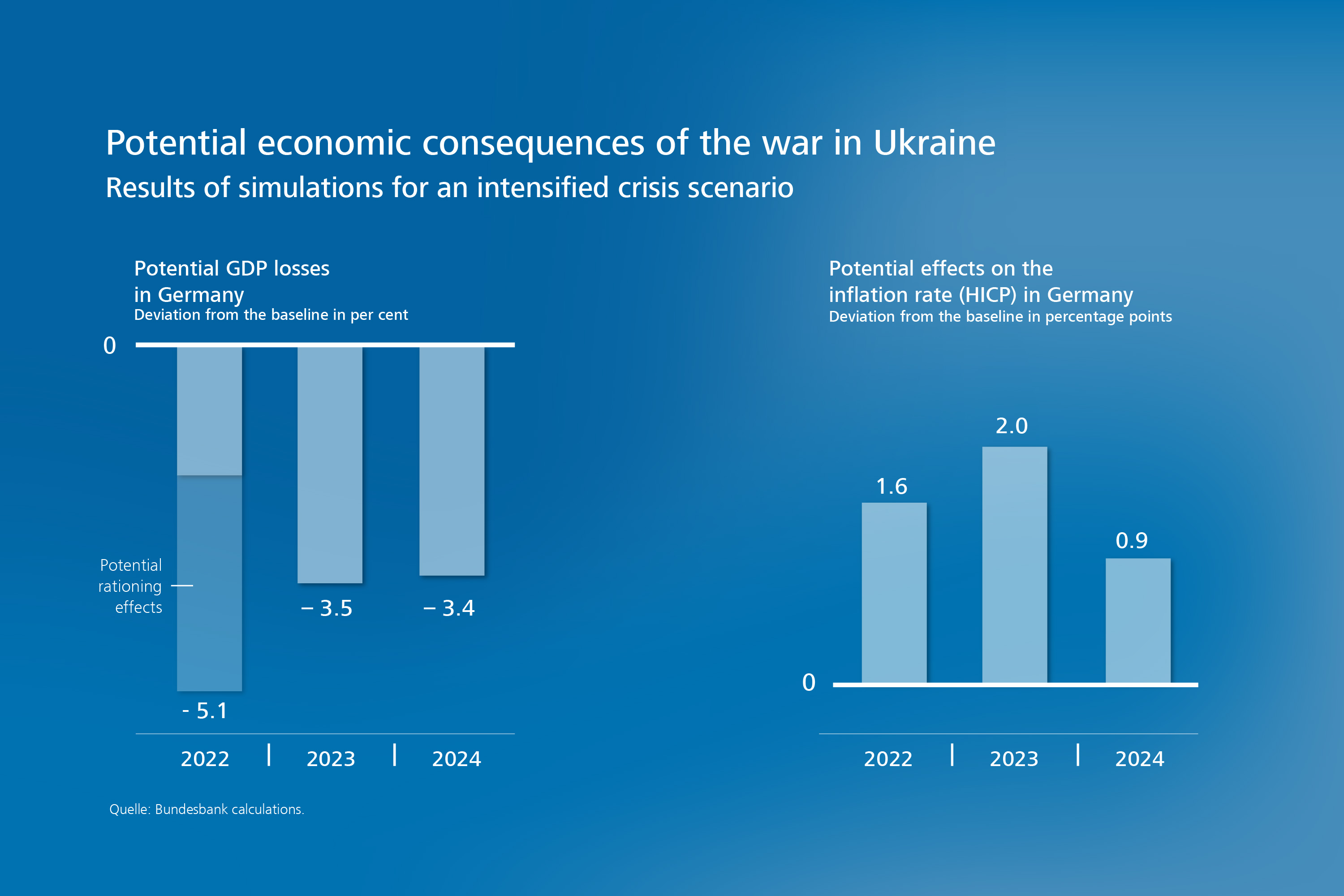

War against Ukraine: energy embargo could significantly weaken German economy

In the current issue of its Monthly Report, the Bundesbank uses scenario calculations to analyse the potential macroeconomic impacts of a further escalation of the war against Ukraine. The experts specifically assume that trade with Russia, including energy imports, will be subject to an embargo until further notice and that this could lead not only to price effects but also to a rationing of energy use. In this case, real gross domestic product (GDP) in Germany could, over the short term, be up to 5% lower than expected in the March projection issued by the European Central Bank (ECB). Real GDP would fall by just under 2% compared with the previous year.

{kind=link}

Inflation could be higher for longer

According to the Bundesbank’s experts, inflation would also once again surge considerably. In the observed scenario, the inflation rate in Germany could exceed the ECB’s projections by 1½ percentage points in 2022 and by 2 percentage points in 2023. The experts cite a significant rise in energy prices given a further escalation of the situation as the main reason. The inflation rate is expected to remain elevated in 2024 as well, albeit no longer as strongly. According to the Bundesbank, the risks for inflation are, on the whole, tilted to the upside, since price increases at downstream production stages or wage increases could potentially be stronger.

The experts stress, however, that, owing to the complexity of the problem, all results are fraught with considerable uncertainty. They warn that the identified developments, especially with regard to GDP, could be either overstated or understated.

Strongest rises expected for natural gas prices

The experts used several macroeconomic models for their simulations in order to address the various aspects and transmission channels of the observed scenario. They used these models to analyse the impact of a hypothetical further escalation of the conflict on the economies of Germany and the euro area. In the event that key buyer countries impose an energy embargo against Russia, it stands to reason that prices for crude oil, natural gas and coal will rise considerably. The price per barrel of Brent crude oil could go up to more than US$170. “Natural gas prices in Europe are expected to see the strongest rises since Russian deliveries will be very difficult to replace in the short term,

” the Bundesbank writes. For other commodities, the expected price mark-ups are expected to be more moderate overall.

The report’s authors list several factors which could lead to GDP losses in Germany on the heels of the war. To wit, an increase in commodity prices, which would indirectly erode household incomes, would weaken growth considerably. Moreover, foreign demand, and thus German exports, would decline significantly. The third factor they list is heightened uncertainty, which would be a drag on business investment and private consumption. According to the experts, the incorporated fiscal measures would only offset a small portion of these losses. “However, it may be expected that, in such a scenario, fiscal support measures above and beyond the incorporated and, in the meantime, additionally planned government measures are likely to be taken in order to absorb to a greater extent the negative impact on GDP,

” according to the report.

Energy rationing under a full embargo

In addition, an abrupt halt to Russian energy deliveries would probably considerably constrain domestic production. In their analysis, the experts assume that the use of natural gas, hard coal and petroleum will be reduced by 40% in the affected sectors between the second quarter of 2022 and the end of the year. One factor contributing to the severity of the situation is that, under the assumption in the analysis, there are no options for substituting fossil fuels in the current year.

According to these additional model calculations for energy supply shortfalls, if only energy production and supply sectors were to be cut off from Russian energy deliveries, this could lead to an additional short-term real GDP loss of 1% for the current year. Should the shock in addition directly hit energy-intensive industries which use fossil energy sources to power their production plants or which process fuels as raw materials, the loss could climb to 3¼%. These calculations, too, are subject to a high degree of uncertainty, according to the experts; amongst other things, they depend heavily on the availability of possible substitutes.