Annual accounts for 2025 Statement at the press conference presenting the Deutsche Bundesbank’s Annual Report for 2025

Check against delivery.

1 Introduction

Ladies and gentlemen,

A warm welcome to today’s annual accounts press conference from me as well.

Before I delve into the 2025 annual accounts in detail, I would like to convey three important messages:

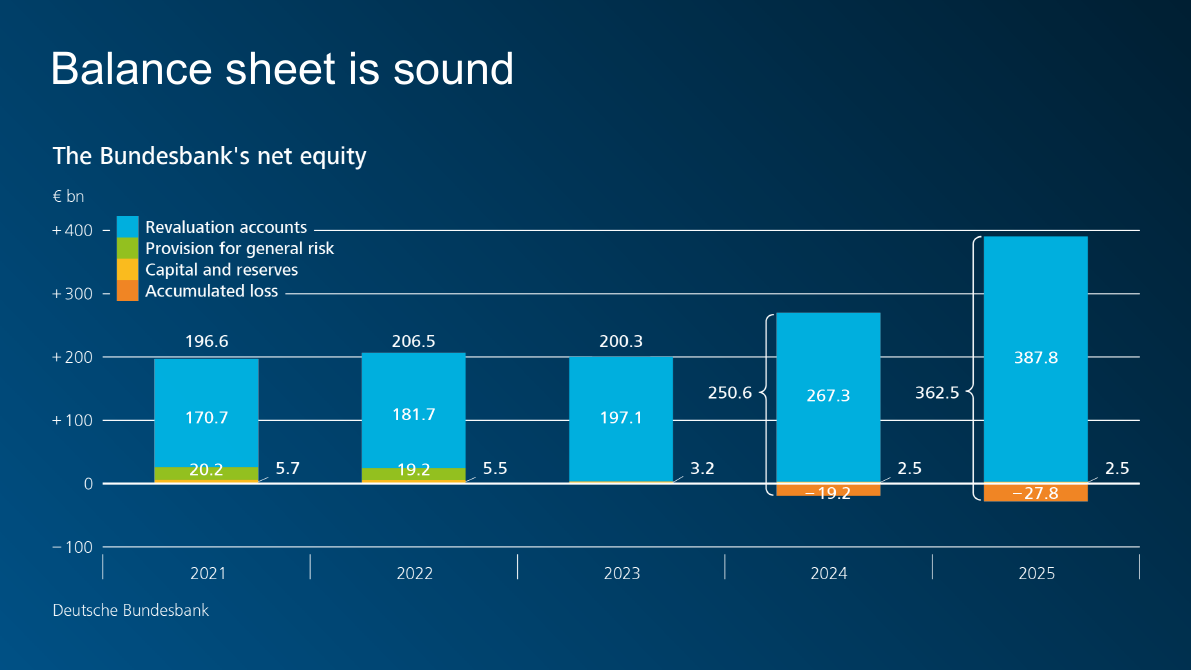

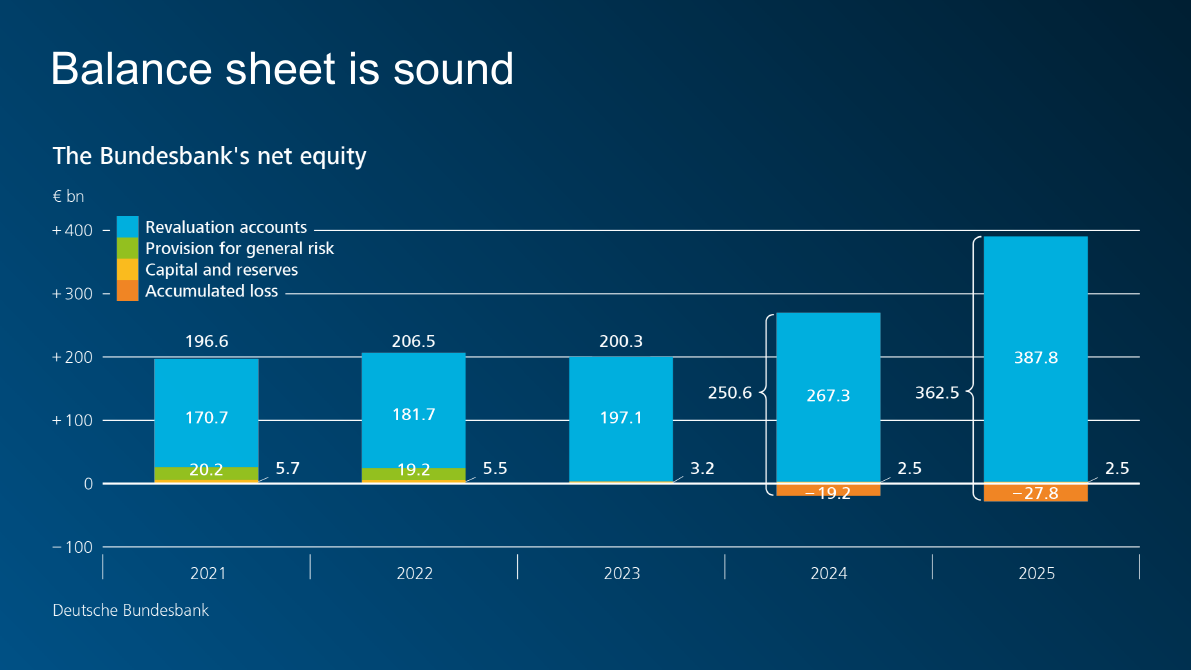

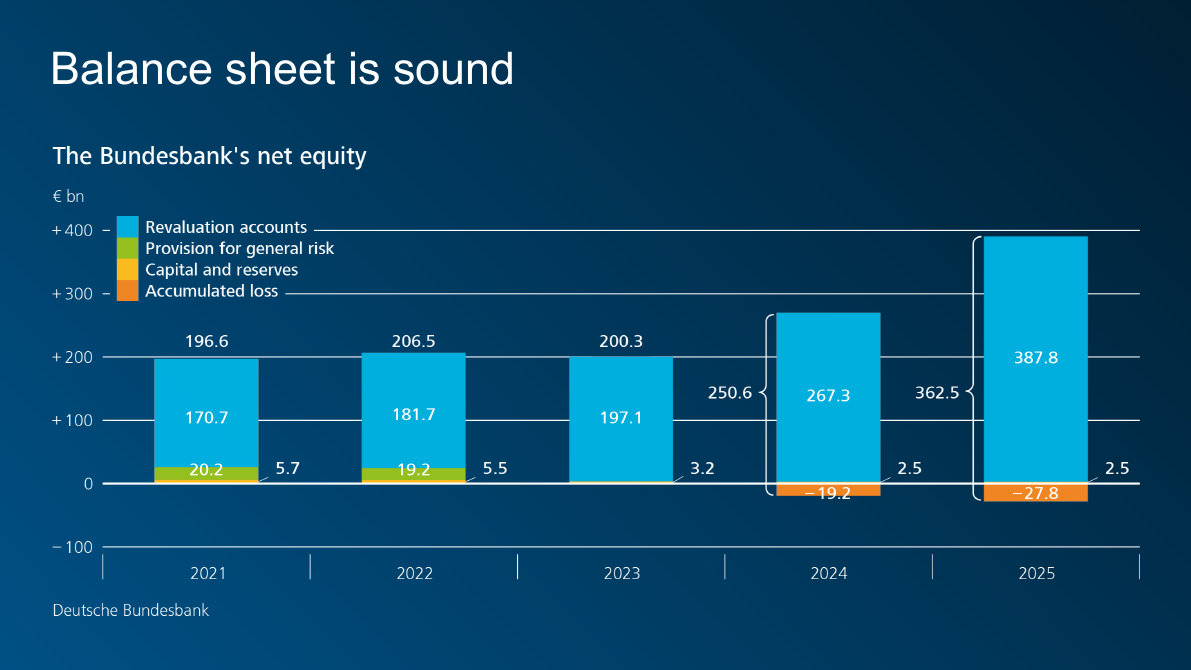

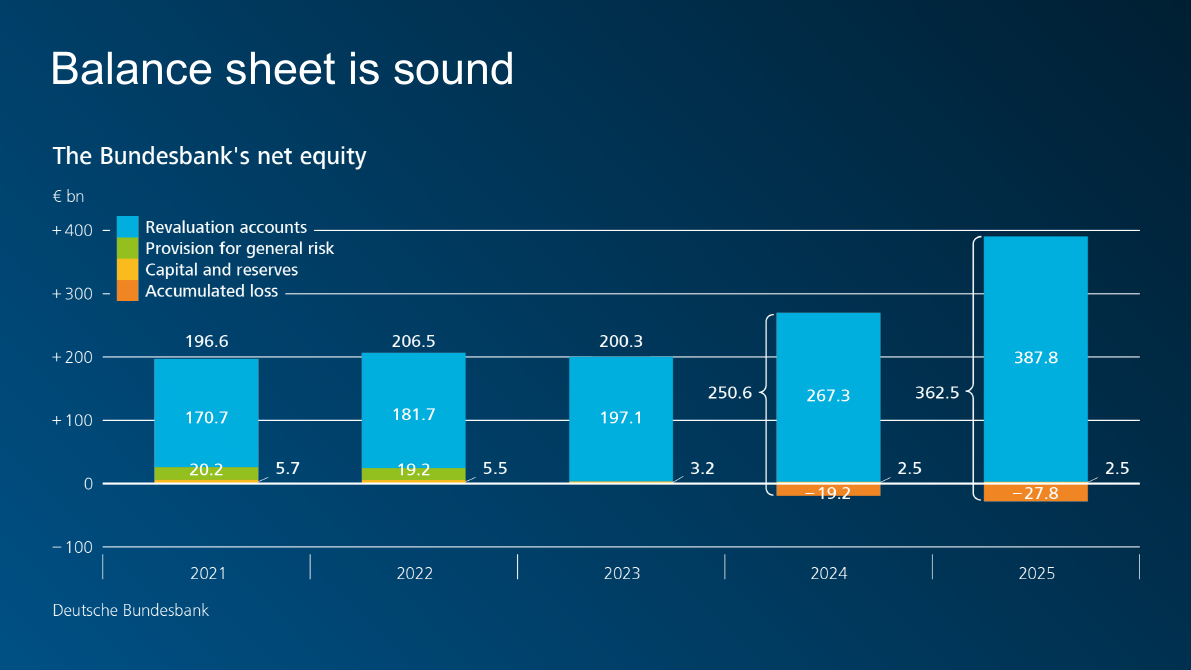

- Net equity has climbed to €363 billion.

- There is a revaluation reserve of €387 billion for the gold.

- The loss for the year has more than halved, and it is likely to decline further in the years to come.

This all means that the Bundesbank is in sound financial shape and remains able to fully discharge its tasks even with an accumulated loss.

Now let’s take a closer look at developments in the annual accounts for 2025.

The financial burdens stemming from the monetary policy measures of the past years made themselves felt again in 2025.

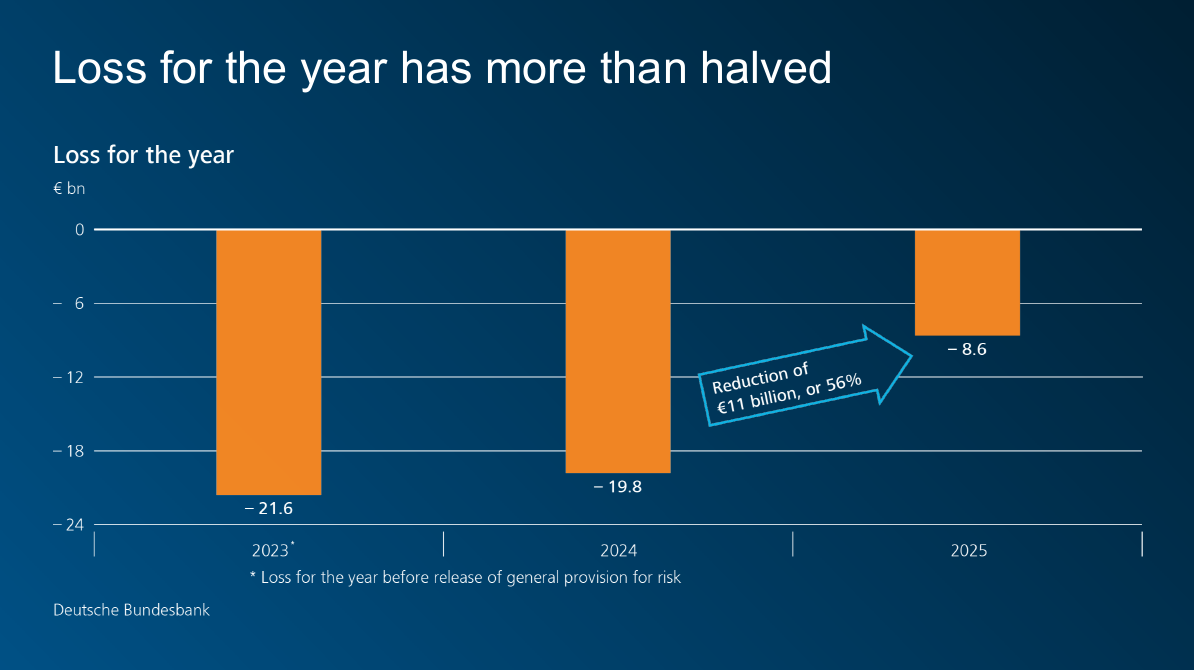

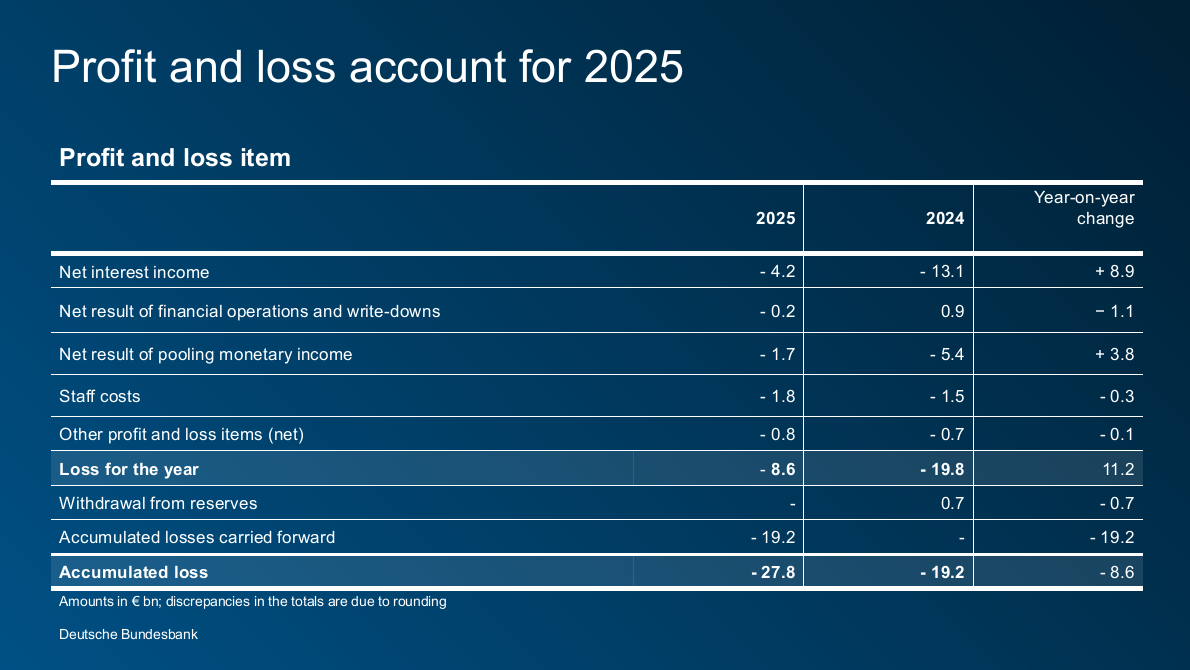

The Bank is ultimately reporting a loss for the year of €8.6 billion for 2025. As mentioned earlier, the loss for the year has thus more than halved compared to the previous year.

The loss for the year of €8.6 billion pushes our accumulated loss up to €27.8 billion.

But as already mentioned: the Bundesbank is on a very strong financial footing.

2 Balance sheet

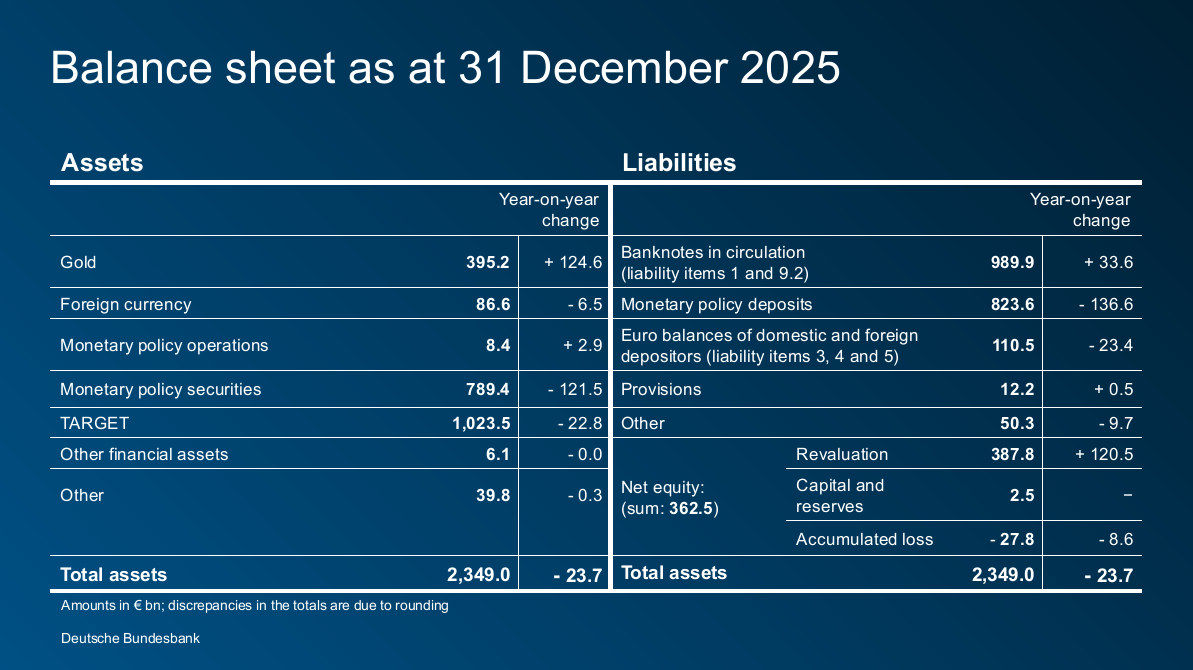

We’ll begin with the assets side of our balance sheet.

Total assets fell only slightly, by around €24 billion. While monetary policy bond holdings declined, the gold position climbed to a historical high.

Three aspects stand out as shaping the assets side of the balance sheet:

Securities holdings from the monetary policy purchase programmes – APP and PEPP – are gradually decreasing as securities reach maturity. Monetary policy securities holdings declined by €122 billion in 2025.

Liquidity outflows meant that the TARGET claim on the ECB saw a slight reduction of €23 billion.

The gold position rose by €125 billion compared with the previous year-end figure on account of valuation effects, reaching a new historical high of €395 billion. This almost offsets the monetary policy-induced decline in total assets.

Looking at the liabilities side of the balance sheet, I again have three points that I would like to highlight:

With monetary policy securities holdings declining on the assets side, the liabilities side saw a further reduction in deposits: liabilities related to monetary policy operations fell by €137 billion on the year.

In addition, other euro balances went down by €23 billion over the past year, mainly owing to smaller balances of non-euro area central banks.Another key item on the liabilities side is banknotes in circulation: when the negative interest rate policy period ended in 2022, growth in the volume of banknotes in circulation within the Eurosystem effectively came to a standstill. Since mid-2024, banknote circulation has picked up momentum again at some national central banks, especially the Bundesbank.

The volume of banknotes issued by the Bundesbank has risen to €990 billion. However, according to the banknote allocation key, the Bundesbank’s share of total euro banknotes issued by the Eurosystem amounts to just €397 billion. The difference of €593 billion can be seen in liabilities sub-item 9.2 “Net liabilities related to the allocation of euro banknotes within the Eurosystem”.The third aspect I would like to address is the revaluation accounts item: this item increased on the year, climbing by €121 billion to €388 billion.

The current slide shows a breakdown of the revaluation accounts item across gold, foreign currencies and securities.

The revaluation reserve for gold contained within that item has risen by €125 billion to €387 billion based on the market value of gold as at the reporting date.

The revaluation reserve for gold has exhibited strong growth, especially when viewed over the long term. This revaluation reserve is currently almost nineteen times as high as its level when monetary union was launched at the start of 1999.

The revaluation reserve for foreign currency has fallen significantly by €4 billion. This is due, in particular, to the US dollar’s weakening against the euro.

The revaluations of gold and foreign currencies have an impact on the Bundesbank’s net equity.

Let’s take a look at what net equity comprises:

- capital and reserves;

- the provision for general risk;

- the revaluation accounts item; and

- as of the 2024 annual accounts, the accumulated loss.

As you can see on the chart, net equity developed positively over a period of several years.

Looking back over the past few years, net equity has risen despite the accumulated loss. In each case, this was due to the revaluation of gold.

The same applies to 2025: net equity has gone up by €112 billion to €363 billion, even though the accumulated loss in 2025 has increased by €8.6 billion to €27.8 billion. As in the previous year, the increase in net equity is due to the revaluation reserve for gold having reached a new high.

Its net equity of €363 billion shows that the Bank can absorb the existing and prospective losses. It is fully able to fulfil its mandate. Our balance sheet is very sound.

3 Profit and loss account

Let’s now turn our attention to the profit and loss account.

The Bundesbank’s earnings situation has improved considerably on the year. Having said that, the key interest rate hikes in 2022 and 2023 continue to have a marked impact on the annual result.

On the assets side, we hold long-term monetary policy securities generating comparatively low levels of remuneration, whilst on the liabilities side there are short-term deposits of banks that are remunerated at higher rates.

Now on to the main items of our current profit and loss account.

The most important component of the profit and loss account is net interest income. While this stood at minus €13.1 billion in 2024, it amounts to minus €4.2 billion in 2025. Net interest income is therefore moving in the right direction.

How has this development come about?

As already explained, the monetary policy asset purchases have given rise to longer-term fixed interest positions generating a low level of remuneration. Turning to the liabilities side of the balance sheet, we find counterparts primarily in the form of short-term, higher-interest-bearing deposits by commercial banks.

The mismatch in maturities creates an open euro interest rate position on the balance sheet. The significant increase in the deposit facility rate in 2022 and 2023 has caused the interest rate risk contained in the open euro interest rate position to materialise, placing net interest income under strain.

How does that look in practice in 2025? Monetary policy securities were remunerated at an average rate of 0.58 % in the reporting year, while credit institutions’ monetary policy deposits gave rise to an average interest expense of 2.31 %.

This gives us a negative interest margin of 1.73 %. That is significantly smaller than the previous year’s figure of 3.28 %, owing to movements in key interest rates. In addition, maturing securities held for monetary policy purposes have brought the open euro interest rate position down by around 24 % on average for 2025.

This places a markedly lower burden on net interest income overall.

Let us now turn to the second bar: the net result of financial operations and write-downs related to foreign exchange and securities. At minus €226 million on balance, this is €1.1 billion lower than in the previous year. This is largely due to exchange rate losses.

Let’s move on to monetary income.

This comprises interest income from monetary policy assets, less interest paid on their counterpart liability items. The resulting net interest income is shared across the Eurosystem according to the capital key.

The third bar shows us the burden from the net result of pooling monetary income. At €1.7 billion, 2025’s figure is significantly lower than the previous year’s.

The €3.8 billion reduction here is mainly due to interest rate cuts and the change in the reference interest rate. Since the beginning of 2025, the lower deposit facility rate has been used instead of the main refinancing rate. As a result, the negative interest margin between the actual remuneration and the reference interest rate has narrowed. This is particularly relevant where monetary policy supranational securities are concerned.

These are securities issued by supranational institutions and purchased by other national central banks as part of PSPP and PEPP purchases. The Bundesbank itself has no holdings. The redistribution effects affecting monetary income are almost exclusively attributable to these monetary policy supranational securities. The Eurosystem’s holdings came to an annual average of €368 billion. The income and risks stemming from those holdings are shared within the Eurosystem.

The supranational securities holdings generate only a low level of remuneration. Calculating the difference compared with the deposit facility rate gives us a negative interest margin of around 1.6 % on an annual average for 2025. In the previous year, the interest margin – calculated by comparison with the main refinancing rate – was still 3.6 %. The resulting lower income for the national central banks concerned is balanced out among the Eurosystem national central banks via the common pool of monetary income. Based on its capital share of 26.6 %, the charge for the Bundesbank came to around €1.6 billion, compared with a charge of €3.8 billion in 2024.

The fourth bar shows staff costs, which came to €1.8 billion in 2025, up €322 million. This was due to higher transfers to staff provisions necessitated by the general pay rise for salaried staff and civil servants.

The upshot overall is a loss for the year of €8.6 billion for 2025. In 2024, the loss for the year amounted to €19.8 billion, but reserves totalling €0.7 billion were still available to offset some of that.

Combined with the accumulated loss carried forward from 2024 of €19.2 billion, carried forward from 2024, the 2025 accumulated loss comes to €27.8 billion. This will be carried forward to 2026.

4 Conclusion

Let me now summarise the key takeaways.

The positive news is that the Bundesbank’s assets considerably outweigh its obligations. Net equity stands at €363 billion and has thus risen by 44.7 %!

The loss for the year in 2025 has more than halved compared to the previous year but is still considerable at €8.6 billion. We expect the burdens to carry on subsiding in 2026. Nevertheless, they will remain sizeable.

The open euro interest rate position will shrink further in size, with monetary policy securities holdings getting progressively smaller as they mature.

Overall, we expect to report accumulated losses for an extended period of time, meaning that we will be unable to distribute any profit.

I would like to wrap up my remarks by stressing again that the Bundesbank is capable of shouldering both its current and foreseeable financial burdens. We are fully able to discharge our tasks. The Bundesbank’s balance sheet remains sound.

My thanks for your attention. President Nagel and I would now be happy to take any questions you may have.

Thank you very much.